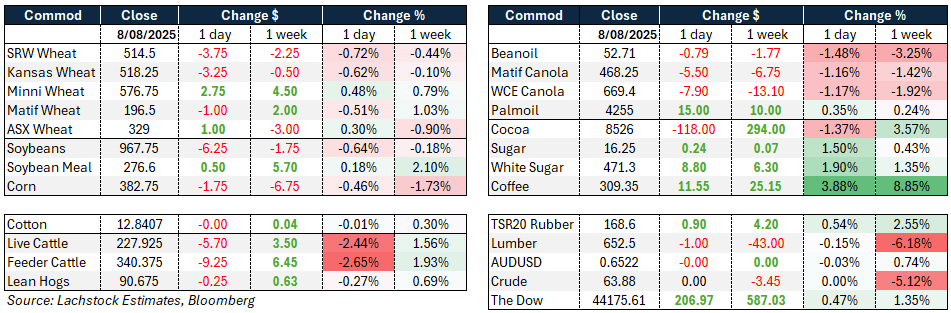

Weather: Black Sea winter wheat harvest is aided by hot, dry weather, while central Russia’s spring wheat benefits from timely rains, though some areas need more sun. Europe’s dry conditions support winter wheat harvest. Canadian Prairie showers are too late to help yields, with earlier heavy rain raising quality concerns. Argentina and southern Brazil saw frosts last week, with more possible, but little impact expected on vegetative wheat; northern areas are heading..

Markets: Busy week for data, particularly in the US with CPI through to the Aug WASDE. Global exporters are desperately trying to push out as much wheat as possible before Russia sorts out its supply chain.

Australian Day Ahead: Turning the corner – days are getting longer and temps are sneaking up which should see some decent growth. So far, Aussie current crop values haven’t really responded to the spike in Asian demand but it will be interesting to see if we have another week of enquiry. Aside from that, the market lacks drive.

.

Offshore

Wheat

US wheat futures softened despite an early rally, with Chicago and Kansas down while Minneapolis held gains on storm damage in the northern plains.

The market is increasingly convinced the US spring wheat crop will be 30–40 million bushels smaller than USDA’s estimate, with potential carryout near 800 million bushels if exports stay strong.

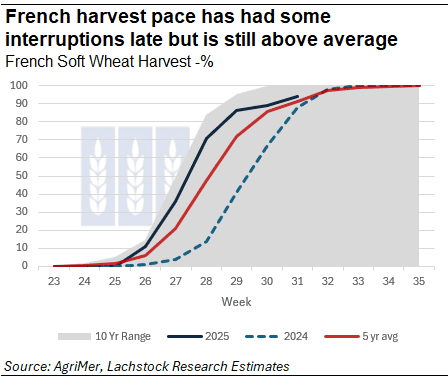

Export demand remains firm as EU, Black Sea and Baltic supply challenges divert business to the US, while French growers have been slow sellers.

Russian FOB values remain elevated despite IKAR raising its crop forecast to 84.5 million tonnes (Mt) and exports to 41.5Mt, amid ongoing logistical and quality issues.

Tunisia purchased 75,000t soft wheat from optional origins, and France’s crop estimate was lifted to 33.07Mt, up 29pc y/y and 4pc above the five-year average.

Ukraine’s wheat exports are down 49pc y/y, and quality concerns are growing, with feed wheat potentially reaching 50pc of production. Harvest estimates for Ukraine range from 19–21Mt, with private analysis leaning toward the lower end based on seasonal conditions.

US feed wheat has found recent demand from Asia, with South Korea booking multiple cargoes.

Other grains and oilseeds

Corn markets eased as attention returned to yields ahead of WASDE, with Farmer Business Network’s 186.4bpa reinforcing expectations for a large US crop.

US export competitiveness is improving, particularly from the PNW, as the US-Brazil price spread widens.

Brazilian safrinha corn farmers remain reluctant sellers, keeping FOB values high and deterring some buyers.

France’s corn harvest is forecast down 5.5pc y/y to 13.7Mt on lower yields from heat and water stress, and crop ratings have fallen sharply from last year.

Ukraine’s corn exports are down 62pc y/y, with 706,000t shipped since July 1.

Soybeans weakened as bean oil losses outweighed modest meal gains, with US crush margins slightly lower.

China continues to avoid US origin, purchasing heavily from South America and pushing Brazilian basis higher; rumours of Brazil importing US beans lack confirmation.

Palm oil prices rose on expectations of stronger Indian buying ahead of festival season, with Malaysian exports up over 5% in early August.

Global vegetable oil prices rose 7.1pc m/m in July to a three-year high, supported by robust demand and tighter Black Sea sunflower oil supplies.

Macro

The RBA is expected to cut rates 25bps to 3.6pc this week, its third cut this year, as inflation nears target and growth shows signs of picking up.

Governor Bullock is likely to maintain a cautious, data-dependent stance, with markets pricing one more cut in 2025.

Labour market softness, global uncertainty, and weaker Chinese demand are influencing the outlook.

In the US, President Trump appointed Stephen Miran to the Fed board in a move favouring lower rates.

Gold markets saw temporary disruption after tariff confusion on bullion imports.

US-China’s trade deal expiry looms on August 12 without an extension announced.

This week’s US data includes July CPI (core expected +0.3pc m/m, headline +0.2pc), retail sales, and consumer sentiment, with tariffs beginning to impact goods prices modestly.

Australia

New crop canola bids were steady to slightly firmer through the west of the country at A$836 and GM $757 FIS, with wheat $354 and barley $333.

Through the eastern states, canola was $816 and GM $760 track, wheat $352 and barley $315.

Rainfall and falling global values during the northern hemisphere harvest have seen delivered bids ease over the past month, with Geelong/Melbourne delivered APW1 down $15, ASW down $10, Griffith MZ down $9, and SFW Darling Downs down $10.

This week will see some southern crops experience their first couple of days in the low 20s, which will spur growth but also shift growers’ attention to the forecast—nothing significant for the next 10 days, with enough subsoil moisture for now, though it won’t last long once crops get cracking.

HAVE YOUR SAY