INGHAMS results out on Friday show a tough year to June for the poultry major, with revenue, profit, and core volume all down on the FY24 results.

Across its Australia and New Zealand operations, core poultry volume at 461,200 tonnes was down 1.4 percent from FY24, earnings before interest, taxation, depreciation and amortization at $392.2 million fell 15.3pc, and net profit after tax at $89.8M was down 10.2pc.

Across its Australia and New Zealand operations, core poultry volume at 461,200 tonnes was down 1.4 percent from FY24, earnings before interest, taxation, depreciation and amortization at $392.2 million fell 15.3pc, and net profit after tax at $89.8M was down 10.2pc.

“FY25 was a year of significant change, and I am proud of how the business responded, successfully completing the Woolworths contract renewal and onboarding of new customer volumes, despite challenging Australian market conditions,” Inghams’ chief executive officer and managing director Ed Alexander said.

“We remain confident in our long-term value proposition, underpinned by solid business and market fundamentals and a clear strategic agenda focused on outstanding customer service, cost optimisation, and margin enhancement.”

In Australia, core poultry volume fell 2.5pc over FY25 to 388,000t, reflecting the transition to the new Woolworths supply agreement and softer market conditions in key channels during the June quarter, but grew 5.2pc in New Zealand to hit 73,200t.

At a channel level, retail volumes declined 4000t, driven by the Woolworths transition, and partially offset by new business in QSR and other retail customers.

In the Australian wholesale market, volume fell 3.8pc, and includes transition of some third-party wholesale sales to in-house processing supported by Inghams’ recent investments in automation.

Across the group, the core poultry net selling price (NSP) was $6.31/kg, up 0.5pc from FY24, and despite the wholesale NSP/kg dropping 10pc.

Inghams said retail and out-of-home demand for its products was subdued in the second half, with cost-of-living pressures dampening retail category volume in the June quarter.

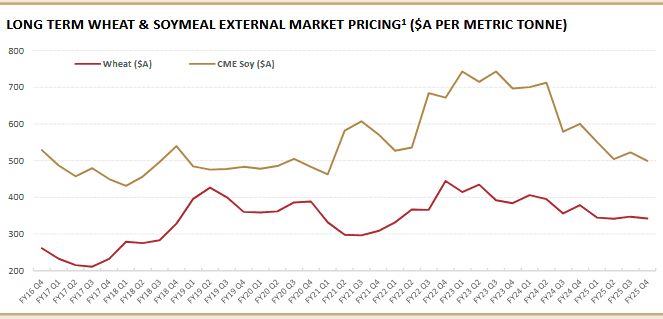

Buffering the impact of a tougher sales environment was wheat and soymeal prices being at their lowest in recent years, with the average soymeal price in Australian dollar terms declining 20pc during FY25.

Figure 1: Quarterly spot price data for wheat and based on an average of daily market observations. These do not reflect Inghams’ actual consumption prices due to the purchase of delivered grain/soymeal as well as a level of forward cover of 3-9 months. Source: Inghams

Feed costs declined $49.8 million in FY25 from FY24, reflecting the improvement in market pricing of key feed inputs over the past 12 months.

However, its external feed revenue fell due to a decline of 8.3pc in the NSP/kg to reflect the reduction in key feed input costs.

In regard to non-feed costs, moderate growth was seen over the year for utilities and cleaning, while growth in salaries and wages of 3.9pc broadly reflected annual increases across the company’s various enterprise agreements.

Inghams recorded higher operating costs due to the conversion of 121 contract growers to variable performance-based contracts over the past two years, including 55 in FY25.

Source: Inghams

HAVE YOUR SAY