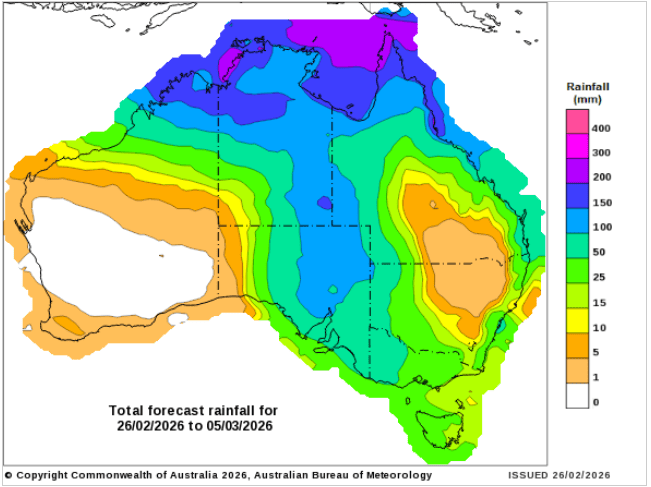

Weather: Same same – Europe has had a bunch of rain but is very warm compared to normal.

Aussie rain amounts have probably dropped off a little for Southern NSW and Vic but SA still looks solid.

Markets

Wheat is in the corner, getting pounded but remains on its feet. The fact it’s still holding above the 200-day moving average is significant.

AUD reacted to the inflation data which has firmed ideas of a May rate increase.

Day Ahead – Australia

Old crop markets are increasingly a function of grower liquidity rather than export parity relative value. Wheat export path needs to turn on or, eventually, export estimates have to be reduced, adding to the carry over.

There is a push pull between the weather outlook and global values.

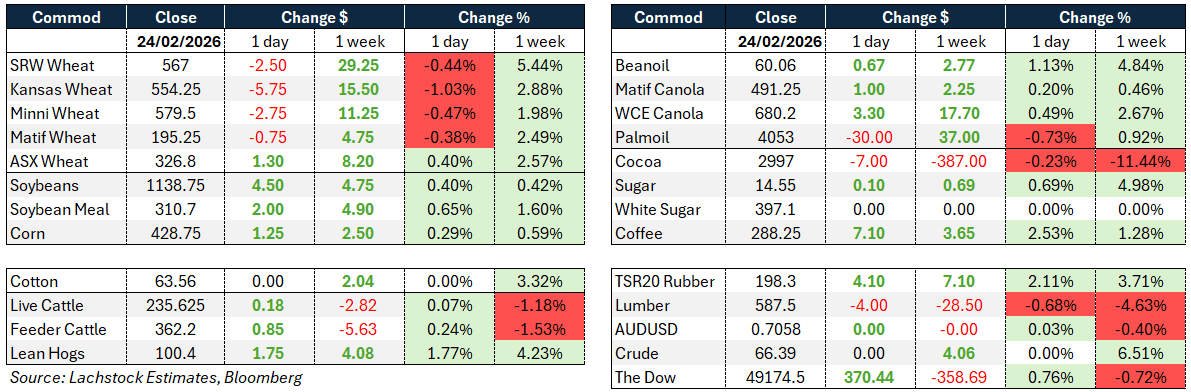

Global wheat: Chicago 565.75 -1.75 (-0.31%) Kansas 552.50 -1.75 (-0.32%) Matif 193 -2.25 (-1.15%)

Wheat proved resilient despite a run of negative influences. US futures were lower on the day while Matif also slipped and Russian cash remains near $234.50.

Forecast rains are still heading to the southern Plains beginning Sunday, improving winter wheat prospects, while reports circulated that 1–2 vessels of Argentine 11.5% protein wheat moved into the southeastern US.

The import arbitrage reportedly closed quickly and the US structurally remains a difficult destination for sustained imports, but the headline was noted.

Despite these pressures, Chicago and Kansas contracts remain above their 200-day moving averages.

The market absorbed improving crop conditions, import talk, and expectations of a large managed money short position likely to be revealed in upcoming COT data.

Sales expectations sit near 325k versus 288k last week, with only 123k required to stay aligned with the USDA target. US exports are already at 92% of the USDA projection.

Internationally, SovEcon trimmed Russia’s 2025–26 wheat export forecast slightly to 45.4mmt on weaker competitiveness versus the EU, while lifting its 2026–27 outlook.

Indonesia pledged to increase US wheat purchases under a revised trade deal, though traders question whether the targeted volumes can be fully achieved.

Geopolitical developments around Ukraine, Russia, and US policy continue to provide an underlying risk premium, limiting downside even as crop conditions improve.

Other grains and oilseeds: Corn 430.5 +2.75 (0.64%) Soybeans 1148.25 +8.75 (0.77%) Matif Canola 483 -8.25 (-1.68%)

Corn firmed, gaining ground on wheat and tracking beans higher. Safrinha planting in Brazil risks falling further behind given renewed rainfall in the northern regions, potentially tightening second-crop prospects.

Weekly US export sales are expected around 1.35mmt versus 754k needed to maintain the USDA pace, with exports consistently overshooting benchmarks. Taiwan’s MFIG group purchased 65kt of US corn.

Ethanol production slipped slightly to 1.113m b/d but remains ahead of last year’s pace, while stocks rose modestly to 25.646m barrels.

Soybeans rallied on strength in meal and hopes of renewed Chinese demand. While rumors of Pacific Northwest purchases were not confirmed, expectations of stable US tariff policy toward China provided support.

The key question remains whether China will step in for an additional 8mmt of US old crop beans.

Brazilian soybeans remain roughly $40/mt cheaper than US origin, the widest discount in over a year, threatening export momentum.

Meal strength drove crush margins higher, with strong domestic and export demand continuing to clear supply despite elevated crush rates.

In oils, focus remains on US Renewable Volume Obligations, with EPA proposals reportedly moving closer to finalization.

India canceled 65–75kt of previously booked South American soybean oil cargoes, capturing profits during the rally. Nepal’s soybean oil exports to India surged on duty-free access, while EU soybean imports are running 11% below last year.

Malaysian palm oil declined for a fourth consecutive session.

Ukrainian 2026 rapeseed export prices have risen to $530–540/t CPT on weather concerns.

Canola remains underpinned by higher crude and soyoil prices, renewed Canadian exports to China, and strong domestic demand.

Funds have flipped from a net short to net long position amid biofuel mandate speculation for 2026.

Although prices have consolidated after a C$80 per ton rally since the beginning of the year, underlying momentum remains constructive. Large recent elevator sales highlight robust buying interest. Attention turns to Statistics Canada’s upcoming acreage report, though survey timing may underestimate canola area following China’s tariff reduction.

Macro: AUD0.7123 +0.01 (0.92%) Dow 49482.15 +307.65 (0.63%) Crude 66.39

Euro area January headline and core inflation were confirmed at 1.7% and 2.2% y/y respectively, both below ECB projections. The undershoot strengthens the case for potential easing should disinflation persist, with February data and ECB minutes closely watched.

In Australia, January headline CPI held at 3.8% y/y while the trimmed mean accelerated to 3.4% y/y. The result raises the risk of an RBA hike in May, with signs of demand-led pressure in discretionary categories. Monthly dynamics still imply around 0.8% q/q trimmed mean for Q1, albeit with upside risk. Australia’s major projects pipeline reached AUD71bn in 2024–25 and is now expected to peak at AUD105bn in 2027–28, reflecting a broader, more policy-sensitive investment cycle.

Broader macro tone remains shaped by US trade rhetoric, biofuel policy developments, and geopolitical tensions involving Ukraine, Russia, Iran and China. Markets are also watching upcoming USDA export sales data, the Agricultural Prices report, and CFTC positioning for further direction.

Local: Canola bids in the west were softer $762; wheat was steady $320 and barley stronger again $326 FIS Albany.

Through the east canola was back $740, wheat $320 and barley $308 track Geelong.

Barley unlike wheat has underlying export demand out of Victoria which sees prices slowly grind higher. As we move out of Chinese New Year we expect more business to get done.

Rain on the forecast — yes it’s still there — looking promising for SA and Vic. Will this improve liquidity? It may loosen up some grain, but growers still dislike the price and cashflow isn’t a real concern yet, so we’re unlikely to be knocked over by a wave of selling.

HAVE YOUR SAY