Weather: More attention on what the HRW crop can look like – with ideas dropping by the day. This raises two questions – what does this mean for global balances? and what does this mean for US futures?

In the current environment, I feel like a US problem doesn’t move the needle on global FOB values.

However, I question the value of US futures – through the lens of a US blow up, futures look undervalued.

Markets

The soap opera continues – the blockade is more about the US/China relationship than it is about the conflict. China gets a chunk of their energy from Iran so this will be having an impact.

Ag markets have been amazingly resilient to this conflict. We have days like yesterday where it feels like some fear bleeding into our markets only to see it puke out the following day.

Australia is trying to solve some problems – moving grain from central west to the Downs while bringing urea back down due to the lack of planting.

Day Ahead – Australia

How do you trade this market fundamentally? serious question. It does feel like the conflict has lasted long enough that the market is now back to trading – there are opportunities evolving due to the dryness in the north but, from an export front, things are painful.I am guilty of waiting for the Asian consumer to step in – but there is zero panic today.

Global wheat: SRW Chicago +11.25c to 582.25c, Kansas City +12.50c to 603.25c, Matif +€1.00 to 195.75c

The dominant theme across wheat markets was the deteriorating condition of the Hard Red Winter crop across the southern Plains. Rainfall over the weekend fell well short of expectations, with the western half of Kansas, parts of western Nebraska and eastern Colorado receiving little to no meaningful precipitation.

Private estimates suggest around 50 percent of the HRW belt remains in drought and is likely to stay that way, with only the eastern 25pc of the belt and a few isolated pockets receiving adequate rain.

Nationally, winter wheat was rated 34pc good to excellent, down from 35pc the prior week, while HRW states specifically fell six points to 32pc, leaving those states at just 24pc good to excellent versus 26pc the week prior. Most HRW production estimates remain in the 630-650 million bushel range but are seen declining sharply if dry conditions persist, particularly in the west.

SRW conditions are holding up considerably better at 62pc good-to-excellent. Spring wheat planting came in at 6pc complete, matching estimates, and winter wheat was 11pc headed.

The geopolitical backdrop added further support, with US-Iran talks collapsing and the naval blockade of the Strait of Hormuz now in effect, providing a war and inflation bid across the complex.

Russian cash wheat is trading around US$237/t fob and Russia’s April grain exports are estimated at 4.2 million tonnes (Mt), down from 5.3Mt in February.

Ukraine’s 2026-27 wheat production estimate was trimmed to 23.5Mt on lower planted area, though output is still seen at its highest since 2021-22. Ukrainian grain exports for the current season were also cut to 38.2Mt from 40.2Mt, largely on a sharp reduction in the wheat export forecast.

Other grains and oilseeds: Corn-0.75c to 440.25c, Soybeans -13.50c to 1162.25c, Matif Canola +€2.75 to 502.50c

Corn traded higher early in the session, chasing wheat and crude, but faded before testing the 200-day moving average in the May contract at 446.50c, eventually settling down fractionally.

Managed money length in corn continues to be unwound and the session had a similar feel to the prior week’s COT data which showed funds growing tired of holding longs.

US corn remains competitively priced with PNW the cheapest destination to Asia and Argentine and Gulf FOBs roughly at par. Corn inspections of 1.783Mt came in on the high end of estimates with shipments running 34pc above last year, though planting progress at 5pc came in a touch below the 6pc trade estimate.

The blockade of the Strait of Hormuz is raising questions around fertiliser availability and cost, which is shifting some thinking on planted area, with ideas that reduced fertiliser access could trim corn acres while swing acres shift toward soybeans.

Beans were the weakest link in the complex with soyoil tumbling as energy prices came off mid-session, though meal held its ground, with soybean meal settling up $0.10 to 331.90 and May crush up 7.25c at 299.50c.

The prospect of a Trump-Xi meeting remains uncertain given the state of the Middle East, which is weighing on ideas that China will step up old crop bean purchases.

Meal continues to find support from European energy prices, a slow Argentine harvest, and upcoming downtime at several US crush plants.

Bean inspections of 815,000t matched estimates but remain 15pc below last year’s pace, though after the close beans were reported 6pc planted versus trade ideas of just 2pc.

ICE canola continued higher through the session supported by crude oil gains, MATIF rapeseed and Chicago soymeal, though weakness in Chicago soybeans and soyoil capped the upside.

Cumulative Canadian canola exports stand at 5.6Mt versus 7.2Mt the same time last year.

Brazil’s soybean harvest reached 87pc complete as of April 9, slightly behind last year’s 91pc pace, while production estimates for the 2025-26 crop are being revised up around 1.2Mt above the prior national forecast agency estimate.

Macro: AUD0.7095, Dow +301.68 to 48218.25, Crude +$2.51 to $99.08

Risk sentiment improved through the session and into Asian trade as Trump raised hopes of an Iran deal, allowing the S&P 500 to fully erase its 2026 losses.

Equity index futures for Japan, Hong Kong and Australia all gained on optimism that a resolution could ease oil prices and support growth.

WTI crude pulled back in Asian trade despite the naval blockade of the Strait of Hormuz formally taking effect, with at least two tankers abandoning planned transits after a military deadline passed. Oil has nonetheless held near $100 a barrel through the conflict’s seven weeks, supported by the closure of a chokepoint through which roughly a fifth of global oil and LNG flows.

The blockade is also seen as a mechanism to pressure Beijing, which buys Iranian oil, into playing a more active role in reopening the strait.

The recent spike in crude combined with a marked rise in March US consumer prices is shifting bond market focus back toward inflation, with money markets now pricing less than a one-in-five chance of a Fed rate cut by December.

Japan’s 10-year yield hit its highest level since 1997 before paring the move.

Goldman Sachs kicked off earnings season with a mixed result, with strong equity trading revenue offset by a miss in fixed income.

On the housing front, existing home sales fell 3.6pc month on month to 3.98 million annualised in March, a nine-month low, as higher mortgage rates weighed on activity. The median existing home price rose 1.4pc year on year, though price growth remains subdued relative to history, with structurally tight inventory from mortgage lock-in effects keeping upward pressure on prices despite soft demand.

Australia flagged concerns around urea supply disruptions linked to the Iran war, while Western Australia is considering a state-controlled strategic diesel reserve holding millions of litres to buffer shortages hitting farming and mining.

Local: Stronger to start the week in the west with canola A$770/t current season and $815 new, wheat $332 and $342, barley $338 and $333 FIS Albany – through the east canola $749 and $784 new season, wheat $332 and $365, barley $312 and $325 track Geelong.

Seeding now in full swing through SA, Vic and WA, well ahead of recent years pace — for the most part rotations unchanged despite higher inputs, with growers looking to capitalise on full moisture profiles.

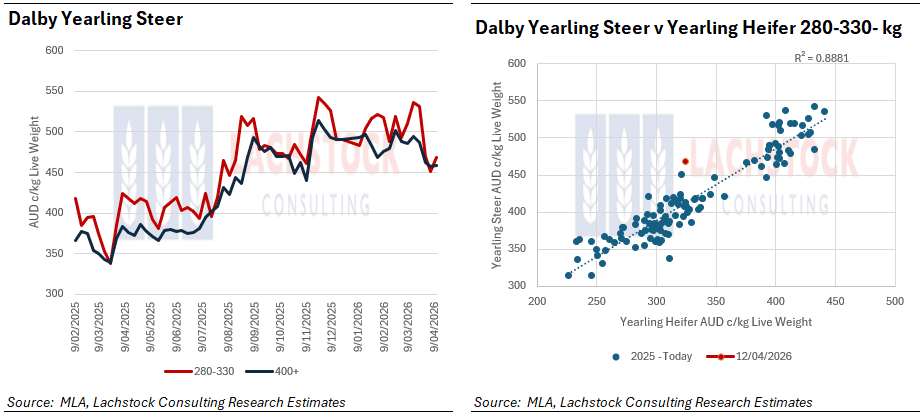

Flatback feeder steers have softened ~10c over the past fortnight (450–470c/kg Downs), widening the Angus spread as crossbreds come under pressure from rising numbers, full northern yards and a shift in weather (cyclone north, cold south), while heavy feeders remain relatively well supported.

HAVE YOUR SAY