Weather: The challenges in the US have been well documented and are ongoing – there is some rain in the backend but, we have seen this movie before, getting it through to the front end has been difficult.

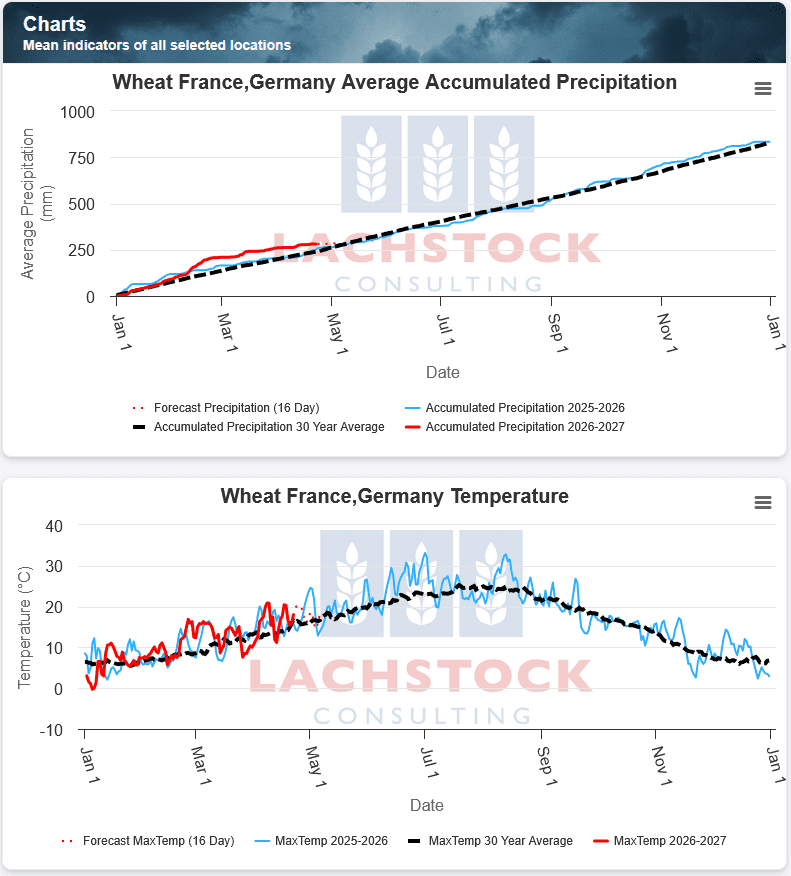

The EU is starting to get some attention with a lack of rainfall over the past month – after a decent start, rainfall totals are gravitating back to longer term averages but forecasts will be traded (see chart below).

The conjecture around the “Super El Nino” and what is an analogue year is pretty interesting – 2023 is getting thrown around.

Markets

Don, at the request of Pakistan has extended the cease fire but is keeping the Strait closed. From a market perspective, this is a push. Clearly, there is a level of market fatigue, most clearly reflected in Singapore Gasoil – the proxy for diesel. The spot contract is 34 percent off the highs posted on the 30th of March.

Day Ahead – Australia

The rumours about a vessel of wheat moving from Pt Lincoln to Brisbane grow. The numbers work on paper but the trade needs some incentive and the discharge port logistics are crucial to making this work.

The search continues for forecasts that have rainfall built in – some showing southern NSW gets a drink early May… lets go with that one.

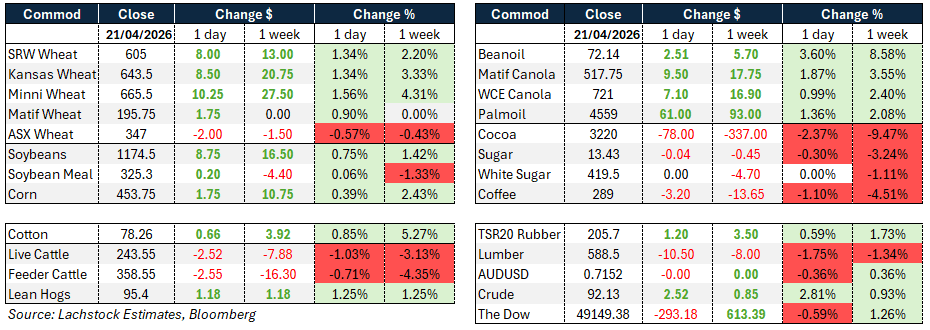

Global wheat: Chicago +8c, Kansas +8.5c, Matif +€1.75

Global wheat: Chicago +8c, Kansas +8.5c, Matif +€1.75

Wheat was the most talked about market today with the tone underpinned by a combination of geopolitical risk premium and genuine crop concern.

Kansas Hard Red Winter conditions remain poor with private forecasters very reluctant to offer any assurances on harvested acres given their track record in the region over the last two months. Rain is in the forecast but confidence is low. The chatter around poor Kansas conditions is getting louder and the market is not willing to be short until more is known.

A new weather concern also emerged today with Europe having been dry for the past four weeks and the two-week forecast also dry, potentially extending the dry stretch to six weeks if realised.

Early weakness in Chicago was erased through the session with all three markets closing firmly. Russian cash was assessed US$1.50/t higher to $241.

The geopolitical backdrop added further support with the Iran situation creating ongoing uncertainty around fertiliser supply chains, a concern flagged as a potential headwind for crop yields in corn and soybeans being planted this month and next.

Other grains and oilseeds: Corn +1.75c, Soybeans +8.75c, Matif Canola +€7.10

Corn had a firm session without being the lead driver, gaining modestly on the back of wheat and bean strength along with crude. A USDA attaché report out of Argentina pegged the 2025/26 corn harvest at 61 million tonnes (Mt), well above the USDA’s last official April WASDE estimate of 52Mt, with the attaché siding with local South American estimates.

Rosario remains the most bullish at 67Mt and Michael Cordonnier raised his Argentine estimate by 6Mt to 60Mt this week.

In Brazil, concern is growing that the dry season may have arrived prematurely which would be unhelpful for the safrinha crop.

French corn planted area is estimated to have slipped below the five-year average, down around 15pc from last year, as fuel and fertiliser costs have roughly doubled since the Iran war began.

On the demand side corn attracted 436,600t in daily sales split between Mexico across multiple marketing years and unknown buyers.

US corn planting is on pace with last year’s record crop at 11pc complete as of April 19. Soybeans were supported by bean oil strength with BOK surging 251 points, driven by biodiesel mandate dynamics.

Brazilian crop agency Conab raised its 2025/26 soybean estimate by 1.4Mt to 179.2Mt with harvest around 92pc complete.

Argentine crush for March came in better than expected.

US soybean planting is running ahead of last year at 12pc complete versus 7pc at the same time last year.

Canola had a positive session on both ICE and Matif, lifted by strength in crude oil and the broader vegetable oil complex.

Chicago soyoil rose above 71 cents per pound providing a key directional cue.

The July WCE contract settled at C$735.00 with analysts eyeing $740 as the next upside target, though the contract encountered resistance at that level.

Cargill announced its new crushing facility in Regina, Saskatchewan is now operational with capacity to process 1Mt of canola per year, producing canola oil for food and renewable fuels as well as protein meal for animal feed.

Palm oil continued to trade near its biggest discount to soybean oil in more than two years, a gap that may support demand in price-sensitive markets such as India.

Indonesian palm biodiesel consumption reached 3.9 million kilolitres year to date under its blending mandate with preparations underway to increase the blending rate further.

Macro: AUD 0.7152, Dow -0.59pc, Crude +2.81pc

The macro backdrop was a whipsaw session driven almost entirely by the Iran ceasefire situation.

As the ceasefire deadline approached markets moved aggressively on and off as headlines crossed regarding Vice President Vance’s trip to Pakistan and whether talks would proceed. Ten minutes after US equity markets closed, President Trump announced an extended ceasefire at Pakistan’s request, with Iran given more time to produce a unified proposal. Trump confirmed the naval blockade on Iran’s ports remains in place and the Strait of Hormuz stays effectively closed, keeping crude elevated.

On the Fed front, chair nominee Kevin Warsh pledged independence from political pressure, argued for a new inflation framework, removal of forward guidance as a policy tool and a gradual reduction in the Fed balance sheet.

US retail sales for March came in stronger than expected with headline sales up 1.7pc month on month, underpinned by a 15.5pc surge in gasoline station spending.

However University of Michigan consumer sentiment deteriorated sharply in April to a record low, keeping the consumption outlook skewed to the downside.

The AUD was steady on the day.

Local: WA bids were stronger yesterday, with canola at A$775/t current season and $810 new season, wheat at $335 and $358, and barley at $342 and $332 FIS Albany.

In the east, canola was $755 current season and $785 new, wheat was $339 and $369, and barley was $314 and $328 track Geelong.

Australian barley is no longer the cheapest origin into China, with French values working lower over the past month. Fresh business is expected to slow, although with most east coast export programs likely to be completed by May, it should not have a major bearing on prices.

Some models are trying to build in rainfall for most of SA, Vic and parts of southern NSW over the next 14 days. It still does not look like it will reach the areas that need it most, but hopefully it may help break down the current pattern.

HAVE YOUR SAY