Weather: Global grain weather remains mostly constructive overall, particularly across the Black Sea region and Europe, where recent rainfall has supported crop conditions. Central China’s winter wheat is filling in generally fair condition, although heavy rain hit some western areas over the weekend.

There are still several problem areas emerging: east-central Russia remains cold and wet, delaying planting progress; the US Plains continue to face stress from recent frosts and drought impacting winter wheat, although this week’s showers have offered some relief. North-western frosts are creating mixed outcomes; the Canadian Prairies have been too cold and wet for timely planting, with showers adding further delays; eastern Australia has received recent showers that are helping newly emerged wheat and buying crops some short-term time relief.

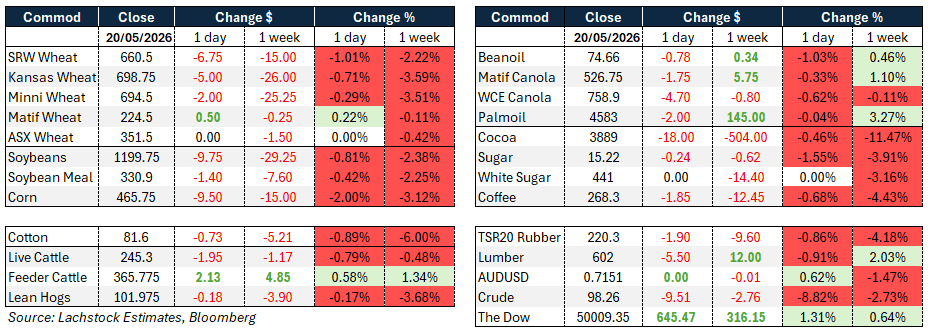

Markets: If we are just focused on the soundbites overnight you would be excused for thinking things have taken a dramatic turn. China hosed down the recent trade deal saying it was more a “vibe”. Donald said that Iran better agree to its terms “or else”, while Iran said forcing their surrender was not going to happen; now look at the market – not a reaction that matches the rhetoric. Keep an eye on US SRW – wet, and warm in a bunch of the belt – say vomitoxin without saying vomitoxin.

Day ahead – Australia: Above export parity, basis generally firm, super El Nino, slow export demand, record cattle on feed, record carry-over in areas, government inventing new ways to tax.

Question: Has the Australian consumer seen the highs in diesel? Before the Iran conflict, we averaged 60 tankers a day through the Strait of Hormuz; since the beginning of March we are averaging three. Meanwhile, the Brisbane terminal gate diesel price has fallen 35 percent from the mid-April highs.

Global wheat: Chicago -6.75c/bu, or 1pc; Kansas -5c, or 0.7pc; MATIF +0.50, or 22pc. Wheat markets opened with a bid on lingering production concerns before being dragged lower by the macro selloff in crude. Minneapolis wheat fell 2c/bu. Early strength in the US was underpinned by genuine supply worries on both coasts — HRW conditions in Kansas remain dire, with 58pc of the crop rated poor or very poor as of May 17, and the USDA forecasting national wheat production down 21pc from 2025 to what would be the smallest crop since 1972. Drought, extreme temperatures and the spread of wheat streak mosaic virus have compounded input cost pressures from higher fertiliser and diesel prices, with some Kansas farmers reporting urea costs up to $600-700/t. On the SRW side, heavy rains are forecast to hit the south-central US over the next two weeks, which is unwelcome news heading into harvest.

Russian FOBs meanwhile rose $3/t to $244, an unusual move given Russia’s comfortable export pace. May shipments are tracking toward 2.9 million tonnes, 38pc above the same period last year. Algeria was reported to have bought around 200,000t of milling wheat at roughly $284-285/t C&F, and Jordan issued a fresh tender for up to 120,000t after making no purchase in its previous round. US export sales tomorrow are expected around 100,000t of current crop and 225,000t of new crop.

Other grains and oilseeds:Corn -9.50c/bu, or 2pc; soybeans -9.75, or 0.81pc; MATIF canola -€1.75, or -0.3pc. Corn never traded higher during the session, with the crude collapse the dominant driver. September corn fell 1.9pc to $4.725, with nearby CN down 9.5c and December off 8.5c.

Weather is non-threatening, with above-normal rainfall forecast for previously dry growing areas, and there was nothing concrete on China, which has not sought offers on US products beyond routine sorghum. The market remains long and is acutely aware that China can read the COT, with the longer they wait potentially meaning cheaper corn. For context, last year at this point corn was short 190,000 contracts and trading at $4.565 with a 1.5-billion bushel old-crop carryout versus the current 2B.

US export sales tomorrow are expected around 1.2Mt current crop and 225,000t new.

Beans followed the macro lower, with SN off 9.75c, SX down 9.5c, meal down $1.40 and oil off 78 points, leaving July crush 2 cents softer at $3.495.

China’s confirmation of the $17B annual ag purchase commitment from the Trump-Xi summit remained vague, with Beijing’s commerce ministry acknowledging only a “guiding target” to expand two-way agricultural trade without referencing the headline figure. China’s April soybean imports from the US more than doubled year on year as cargoes from late 2025 bookings arrived, but further purchases remain contingent on tariff resolution.

Brazil’s Abiove lifted its 2026 soy crush forecast to a record 62.5Mt, up from 62.2Mt previously. Canola fell across the board, with ICE July settling at C$749.80, down $7.90, finding support at its 20-day moving average as farmer selling remained light during active spring seeding.

MATIF rapeseed and Malaysian palm oil were also lower, though palm found some support after Indonesia announced plans to centralise commodity exports through a state-run enterprise, raising supply concerns.

Macro: AUD flat at 0.7151 US cents; Dow up 1.31pc to 645.47; Crude down 8.8pc to US$9.51. The session was dominated by President Trump’s comments that the US is in the “final stages” of an Iran peace deal, which sent crude tumbling more than 5pc with spot WTI settling near $98. The prospect of the Strait of Hormuz reopening drove a swift removal of risk premium across energy and commodity markets, though scepticism remains well-founded; Iran’s president publicly rejected the notion of surrender, the IRGC threatened retaliation beyond the region if hostilities resume, and the core demands of both sides remain far apart. The US insists on full nuclear disarmament and a reopened strait; Iran wants the port blockade lifted first.

The EU struck a provisional agreement to remove import duties on US goods as part of the July trade deal reached as part of the Turnberry Agreement, with preferential access granted to US farm and sea produce in exchange for 15pc tariffs on most EU goods.

US Treasury Secretary Bessent said the administration is not in a rush to extend the China tariff truce beyond its November expiry.

John Deere reports Thursday, with investors watching for signals on farm equipment demand — fuel and fertiliser cost pressures from the Iran conflict are seen as a constraint on farmer spending.

Local markets: Through the east of the country canola bids were steady bid A$785/t for current season and $820 for new, wheat was $340 and $367, barley $318 and $330 track Geelong. In the west, canola was firmer with current season bid $815 and new $855, wheat was $360 and $375, barley $342 and $341 FIS Albany.

Some chickpea interest from Bangladesh has emerged over the past few days, the first meaningful inquiry seen for a few months. Traders don’t expect huge depth to demand, but it is certainly welcome.

Despite improving eastern Australian cattle markets, analysts are warning of growing export headwinds into H2 2026 with China’s safeguard quota nearly full, renewed access for US beef into China and potentially 400-600kmt of displaced Brazilian beef expected to compete more aggressively into global markets later this year.

HAVE YOUR SAY