Weather: If anything, recent rainfall throughout the northern part of the HRW belt should be adding back some mts. The market clearly thinks the risk is behind us and there is genuine risk that the USDA production estimates maybe understated.

Weather: If anything, recent rainfall throughout the northern part of the HRW belt should be adding back some mts. The market clearly thinks the risk is behind us and there is genuine risk that the USDA production estimates maybe understated.

Russian weather has been pretty amazing – with production estimates heading north it is amazing that Russian FOB is holding above US$240/t.

Locally, the recent rains in the north have been too much of a good thing in some areas with the ground still too wet to get back on. Those that made the call to dry sow are in good shape.

Canada is still battling areas that are too wet to plant. Historically, a rally based on too much rain has an uncanny record of hurting the long.

Markets

So, Don reckons he is close, like really really close, to an agreement that would see the Strait open. Meanwhile it feels like it is game on again with Kuwait getting hit. The disconnect between the sound bites and the missiles makes me wonder how this ends. Clearly, Iran isn’t going to budge on its nuclear program which creates an impasse. How can Don get out of this and save face? The House in the US voted to limit Don’s powers with 4 Republicans crossing the floor. One thing we have learnt through this however, Don finds a way to do what Don wants.

Day Ahead – Australia

Canola up, cereals down.

It’s odd seeing articles in Bloomberg indicating that canola is rallying due to dryness in Australia. not sure I would put my name to that. In much of the canola growing belt establishment would be near record. It proves this rally has people scratching their heads – not sure it’s that complicated – energy goes up, vegoil and bio-fuel feedstocks catch a bid, crush margins look solid, seed goes up. Add in a Canadian planting delay and away we go.

Anyone else find it strange that we have cut off 20 percent of the global energy supply, yet I filled up with diesel at A$2.15/l vs pre war at $1.95/l. Yes there has been an exercise cut but this doesn’t add up to me. One logical conclusion is the $1.95/l pre war was fully juiced.

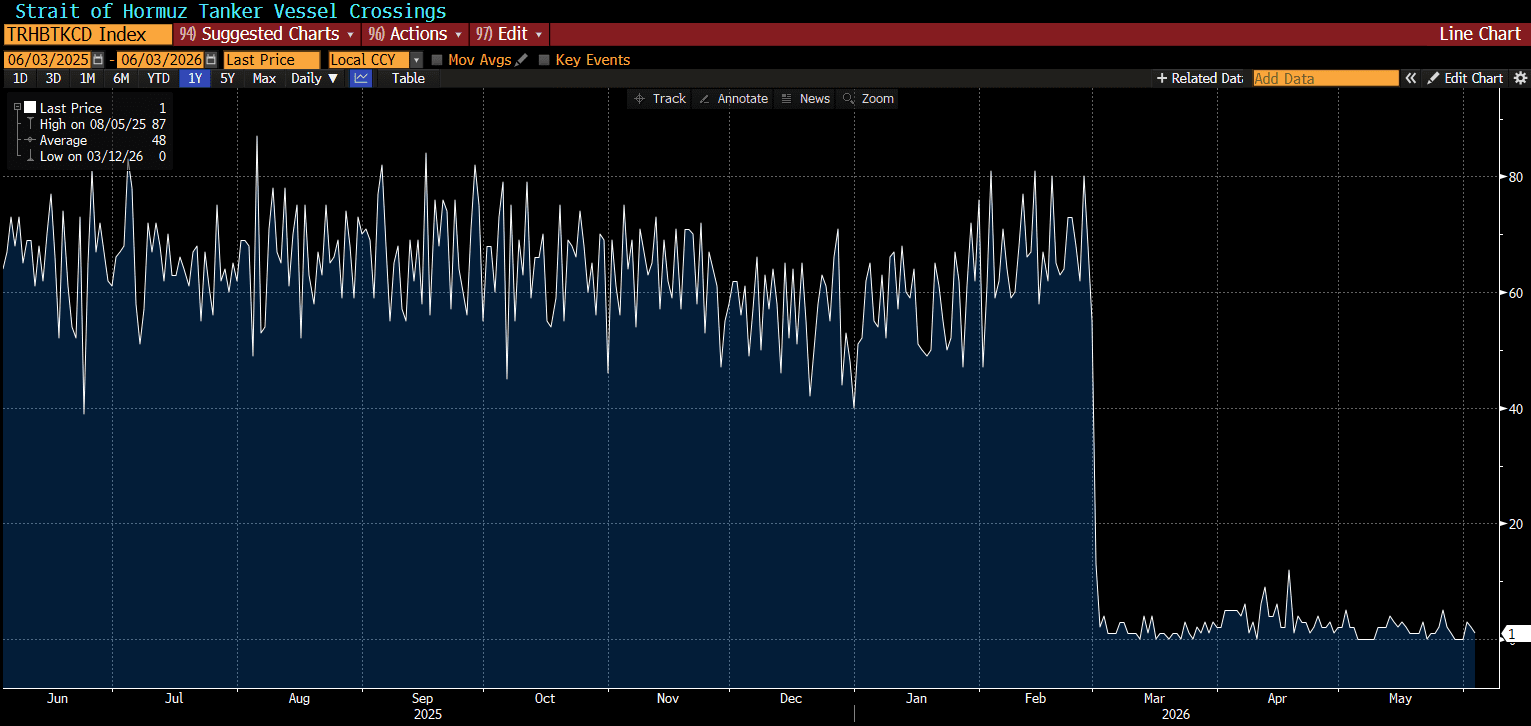

Source: Bloomberg – Strait of Hormuz Vessel Crossings

Global wheat: Wheat markets endured another brutal session with no meaningful relief in sight. Chicago has now finished lower in nine of the last ten sessions, with the 100-day moving average offering zero resistance as sell orders cut straight through it.

Kansas City has posted ten consecutive down days, a stretch not seen since a twenty-session losing run in mid-2009. The algo-driven selling has been relentless, compounded by the Deutsche Bank roll of July/July 2027 contracts through the 6th business day and the index roll beginning Friday.

Seasonal headwinds, harvest pressure and the parade of fund liquidation of stale longs are all conspiring against any recovery attempt.

Russian cash eased another US$0.50/t to $244/t and Russian export duties on wheat, barley and corn remain at zero through June 9, keeping that origin competitive. Russia’s Institute for Agricultural Market Studies raised its 2026 wheat harvest forecast by 1.5 million tonnes (Mt) to 91.5Mt, adding further weight to the bearish supply picture.

The US winter wheat harvest is underway in five states with 5% of the crop cut as of May 31, ahead of the five-year average.

Ukraine’s winter wheat, rye and barley crops are mostly in good and satisfactory condition.

EU soft wheat exports reached 21.5 million tons as of May 31, up 6% from the same period last year.

On the demand side, Jordan issued a new tender for up to 120,000 tonnes of optional-origin milling wheat with a June 9 deadline, following a recent purchase of 60,000 tonnes at $276/tonne for August shipping. Egypt has now procured 4.38 million tonnes of local wheat this season, a record pace running 15% ahead of 2025 and 37% above 2024, against a full-season target of 5 million tonnes.

Morocco plans to suspend its 135% import duty on soft wheat from August 1 to allow resumed imports ahead of the next season, having introduced the duty from June 1 through July 31 to protect its anticipated bumper harvest.

Morocco imported 6.36 million tonnes of wheat in the twelve months to end-May, up from 6.02 million tonnes a year earlier.

At this stage the market is deeply oversold but momentum is entirely in the bears’ hands and there is little appetite to catch a falling knife.

Other grains and oilseeds: Corn is in the same quicksand as wheat. July corn is hovering only a few cents above its contract low, a staggering reversal from when CN was threatening 490.

The China short-covering rally that temporarily lifted prices has now unwound entirely, taking new longs down with it.

Benign US weather, weak cash, poor seasonals and cheaper Argentine values are all pressing.

Argentina’s corn harvest is not yet 50% complete and remains the cheapest FOB origin and best value landed, having narrowed the US premium to near par into Asia.

US corn sales tomorrow are expected at 1.2 million tonnes old crop plus 350k new crop.

The USDA confirmed a sale of 136,000 tonnes of US corn to South Korea but the market shrugged.

In soybeans the divergence between products continues: beans and meal are heading lower while bean oil and crush are forging ahead.

July beans fell 11.25c, soymeal dropped $5.40, and bean oil gained 30 points, leaving July crush up 2.5c at $4.1750.

The market wants confirmation of easier trade with China and the “board of trade” concept floated by USTR Greer would be a start.

USDA Deputy Secretary Vaden said at the WSJ Global Food Forum that China has met an initial commitment to buy 12 million tonnes of US soybeans and is standing by an agreement to purchase 25 million tonnes annually, with new purchases underway.

The market however will not be convinced until weekly export sales reports confirm sizable Chinese purchases.

EU soybean imports for 2025/26 reached 12.4 million tonnes by May 31, down 7% year on year.

The standout performer across the complex was canola. ICE Canada July canola gained C$41.30 to C$798/tonne and November rose C$34.30 to C$802, hitting multi-year highs and briefly touching C$800. The rally is underpinned by crush margins exceeding C$400/tonne, reduced farmer selling during seeding and spraying, a weaker Canadian dollar, a recent European heatwave threatening the rapeseed crop, and ongoing Middle East uncertainty.

Matif canola gained €6.25. Klassen of Resilient Capital noted that commercials and end users are stepping in alongside speculative buying, and that production uncertainty in both Canada and Europe is keeping farmer new crop selling subdued.

Palm oil climbed more than 1% on the resumption of Malaysian trade after a long weekend, supported by Chicago soyoil. Malaysian palm oil inventories are expected to rise for a second straight month in May as sluggish exports outweigh lower output.

Macro: The macro backdrop offered a confusing mix of signals for agricultural markets. Crude WTI gained around 2.5% on the day, touching back towards the $100 mark, as Gulf hostilities intensified with an Iranian missile damaging Kuwait’s airport and US military strikes near the Strait of Hormuz.

Despite crude’s strength, agricultural markets have entirely decoupled from the energy complex this week, with the correlation that previously lifted grains on higher oil now effectively broken.

A late-session development of significance was the announcement of a conditional Israel-Lebanon ceasefire agreement, with the deal contingent on Hezbollah ceasing hostilities and withdrawing south of the Litani River.

Trump also indicated Iran is getting close to signing an agreement that would see the Strait of Hormuz reopen immediately.

The OECD warned that the global economic outlook hinges heavily on the duration of the Middle East conflict, flagging recession risk and sharply higher inflation if hostilities persist into next year.

The Trump administration proposed new tariffs of 10-12.5% on imports from 60 economies citing forced labour concerns, drawing pushback from China and the EU.

A separate proposal to impose a 25% tariff on Brazilian products is expected to impact ethanol, sugar and seafood sectors.

Trump also cut tariffs on agricultural equipment to 15% from 25%. Farm diesel in Illinois averaged a record $5.41 per gallon at the start of May, nearly double year-earlier levels, catching producers off guard after expectations of lower energy costs.

US ethanol production for the week ended May 29 rose to 1.108 million barrels per day, near the top of analyst estimates, while stocks fell 362,000 barrels to 24.61 million barrels.

On the corporate front, Altora Ag announced a merger with Australian Food & Fibre, bringing together Altora’s roughly 180,000 hectares of arable land across NSW, WA, Victoria and Queensland with one of Australia’s major cotton and irrigated farming groups, creating a significantly larger diversified broadacre and irrigated agriculture platform under PSP’s ownership.

Local markets: Western Australian bids were mixed yesterday with canola A$815/t and new crop bid $847, GM was firmer at $755 and $792. Wheat was $346 and $358, barley $328 and $326 FIS Albany.

In the east canola was back $4 to $771 and new crop $805, wheat was $337 and new crop $350, barley was $309 and $318 track Geelong.

It’s becoming increasingly difficult to build a bullish wheat narrative from current levels, with global production prospects remaining strong, Russian wheat production expected north of 90mmt, Australian exports sluggish and domestic consumers becoming increasingly well covered.

Australian beef exports surged to a record 152,438t in May, eclipsing the previous monthly high as strong global protein demand, tight US cattle supplies and importers racing to beat quota and tariff triggers in China and South Korea drove shipments higher. The US remained the largest destination at 47,033t, while South Korea and China both recorded exceptionally strong buying programs.

HAVE YOUR SAY