Weather: Really wet in the US on the day El Niño became official.

Weather: Really wet in the US on the day El Niño became official.

Good falls in Geraldton, okay through southern NSW – forecast for SA/Vic through Monday/Tuesday looks super wet.

WASDE confirmed Turkey production at a record – weather has been amazing – odd that they only reduced imports 500kt – this will be adjusted lower imo.

Markets

WASDE was largely in line – well, if you look at the market reaction it seems pretty inline.

This time for sure…. Donald continues to throw out deadlines – this weekend the strait could be open etc. Energy markets seem to believe him… consistently. Once again – I simply don’t understand the fundamental story vs the market. I’m not saying I am right – I’m saying I don’t get it. We have cut out 20% of global supply yet WTI is sub USD$90/bbl and Gasoil is at USD$134/bbl.

Day Ahead – Australia

WASDE is behind us – weather is in front of us

War risk premium is lower today – but interesting to see how agnostic the AUD was overnight to all the noise. It might be my feed but I feel like the 60 mins report on Sunday night will actually start to shape the polls and wider confidence in the Govt. Im fascinated to see if the AUD reacts to an increased or decreased chance of Labor being reelected. Im going out on a limb here, but the teasers suggest that Chalmers may have an image problem.

.

WASDE

WASDE

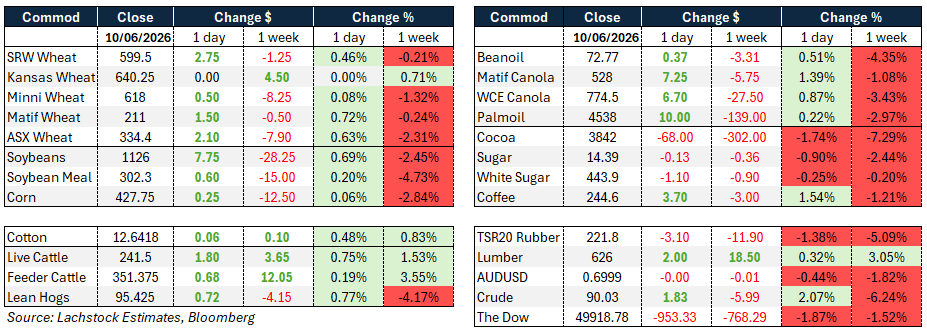

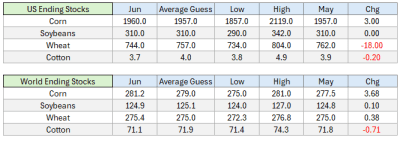

WASDE wheat: The June WASDE delivered a modest bullish surprise in wheat against a heavier backdrop elsewhere.

US all wheat production was cut 18 million bushels to 1,543 million, driven almost entirely by HRW, which fell 18 million to 497 million — roughly 10 million below trade expectations.

The all wheat yield dropped 0.5 bpa to 47.0, with the damage concentrated in Montana (down 6 bpa to 41) and Kansas (down 2 bpa to 35), partially offset by Texas up 2 bpa.

Harvested area was untouched, with revisions to come in later reports — and given the state of this crop, further cuts remain live. With exports steady at 775 million bushels, the production cut flowed straight to the balance sheet, leaving ending stocks at 744 million against trade ideas of 764 and 20 percent below the prior year.

Globally, wheat was less friendly: supplies rose 1.7 million tonnes to 1,100 million, with Russia up 2.0 million to 88.0 million, Turkey up 1.5 million to a record 22.5 million and Ukraine up 0.5 million, against Australia cut 2.0 million to 28.0 million on lower harvested area per ABARES. Global ending stocks were raised 0.4 million tonnes to 275.4 million.

WASDE corn: The US corn balance was effectively a wash — lower ethanol offset by higher exports — leaving ending stocks at 1,960 million bushels versus 1,957 in May, essentially in line with the average trade guess of 1,957.

The world numbers carried the weight: global coarse grain production was lifted 5.8 million tonnes to 1.594 billion, with old crop corn raised for Brazil (up 3 million), Argentina (up 2 million), India and Paraguay. Global corn ending stocks came in at 281.2 million tonnes, up 3.68 million and above the average guess of 279.0 — at the very top of the range of expectations. Chinese imports were unchanged.

WASDE soybean: US 2026/27 soybean projections were left entirely unchanged, with the price held at $11.40, meal at $310 and oil at 70 cents.

Old crop crush was raised 20 million bushels on stronger meal demand, offset by an equal export cut, leaving stocks flat.

Globally, beginning stocks rose on a 2 million tonne lift to Argentina’s prior-year crop, and 2026/27 ending stocks edged up to 124.9 million. Chinese imports unchanged.

WASDE wheat: Wheat closed mostly higher in a session dominated by the WASDE, with the HRW cut providing the support. WN slipped fractions while KWN gained 4.25 cents and MWN advanced 1.5 cents, spreads had a bid, and implied vol in WN eased to 24.72% from 26%.

Matif September was off €0.25 and Russian cash sits just above $240. Export sales were strong at 462.6k tonnes, split 95k old and 367.6k new, with the weekly total exceeding analyst expectations.

The HRW crop carryout now looks like landing near 300 million bushels against the 450 the market had been carrying — not tight, but a meaningful reduction, and harvested area cuts could extend it.

The nearer concern is SRW, where saturated corn belt conditions right at harvest put quality issues squarely in play.

Tightening stocks and too much moisture though the SRW belt arguably tightens things more.

Market commentary

Wheat: Wheat closed mostly higher in a session dominated by the WASDE, with the HRW cut providing the support. WN slipped fractions while KWN gained 4.25 cents and MWN advanced 1.5 cents, spreads had a bid, and implied vol in WN eased to 24.72% from 26%.

Matif September was off €0.25 and Russian cash sits just above $240. Export sales were strong at 462.6k tonnes, split 95k old and 367.6k new, with the weekly total exceeding analyst expectations.

The HRW crop carryout now looks like landing near 300 million bushels against the 450 the market had been carrying — not tight, but a meaningful reduction, and harvested area cuts could extend it.

The nearer concern is SRW, where saturated corn belt conditions right at harvest put quality issues squarely in play.

Tightening stocks and too much moisture though the SRW belt arguably tightens things more.

Other grains and oilseeds: Corn was the anchor, with July falling 1.9% to $4.11 as the WASDE’s larger

South American numbers landed on a market already weighed down by near-ideal US weather. CN and CZ each lost 7.25 cents.

The Climate Prediction Center officially declared an El Niño, bringing drought relief to the southern Plains, and with the Midwest a swamp, yield ideas are heading higher into pollination unless conditions change.

Corn export sales of 1.93 million tonnes beat the top end of estimates, but with weather non-threatening there is little to turn the trend.

Soybeans fell 0.7% to $11.15 3/4, leaning heavy alongside corn, though the China import threat and crush margins argue against being too short to flip.

Canola settled with small losses after early gains, July down C$1.70 to C$764.70, as the late turn lower in Chicago soyoil spilled over; the WASDE itself did little for Winnipeg.

Heavy rain across Western Canada continues to delay seeding, with overland flooding in some areas.

Macro: The Middle East drove the session. President Trump pulled back threatened strikes against Iran hours after vowing to hit it “very hard” and threatening to seize Kharg Island, announcing instead that a deal was close — a conceptual memorandum of understanding that would restart Hormuz shipping and include commitments from Tehran not to pursue a nuclear weapon, with a signing possible this weekend in Europe.

Iran’s Fars news agency said officials had not approved any text, and the war — now in its fourth month — has seen dozens of similar deal claims come and go, including a ceasefire that collapsed days ago.

The naval blockade remains in force until any deal is finalised. Markets took the de-escalation at face value: WTI fell almost 3% toward $85, Brent settled near $90, and equities rallied hard with the Dow up 929 points.

Separately, offshore urea has weakened notably over the past fortnight, with Middle East FOB as of 10 June up only 10% from the start of the conflict, on China returning to the export market, seasonal demand declines, substitution and demand destruction.

Local markets: WA bids were firmer yesterday with canola $815 and new crop $861, wheat $348 and $358, while barley was $330 and $328 FIS Albany.

In the east canola was $10 stronger at $780 with new crop $822, wheat was $330 and $342, and barley $313 and $320 track Geelong.

Lentil bids remain doughy with heavy supply weighing on the market, a situation unlikely to improve over the next 12 months with another large Australian crop and a solid Canadian crop on the way. Current bids sit around $650 delivered southern ports.

Forecast rainfall totals continue to escalate across SA and Victoria, with 50–100mm now expected across most cropping regions. If the models are right, it may be time to swap the ute for a boat.

HAVE YOUR SAY