Weather: Pattern drifted through SA but slide south for the most part

Weather: Pattern drifted through SA but slide south for the most part

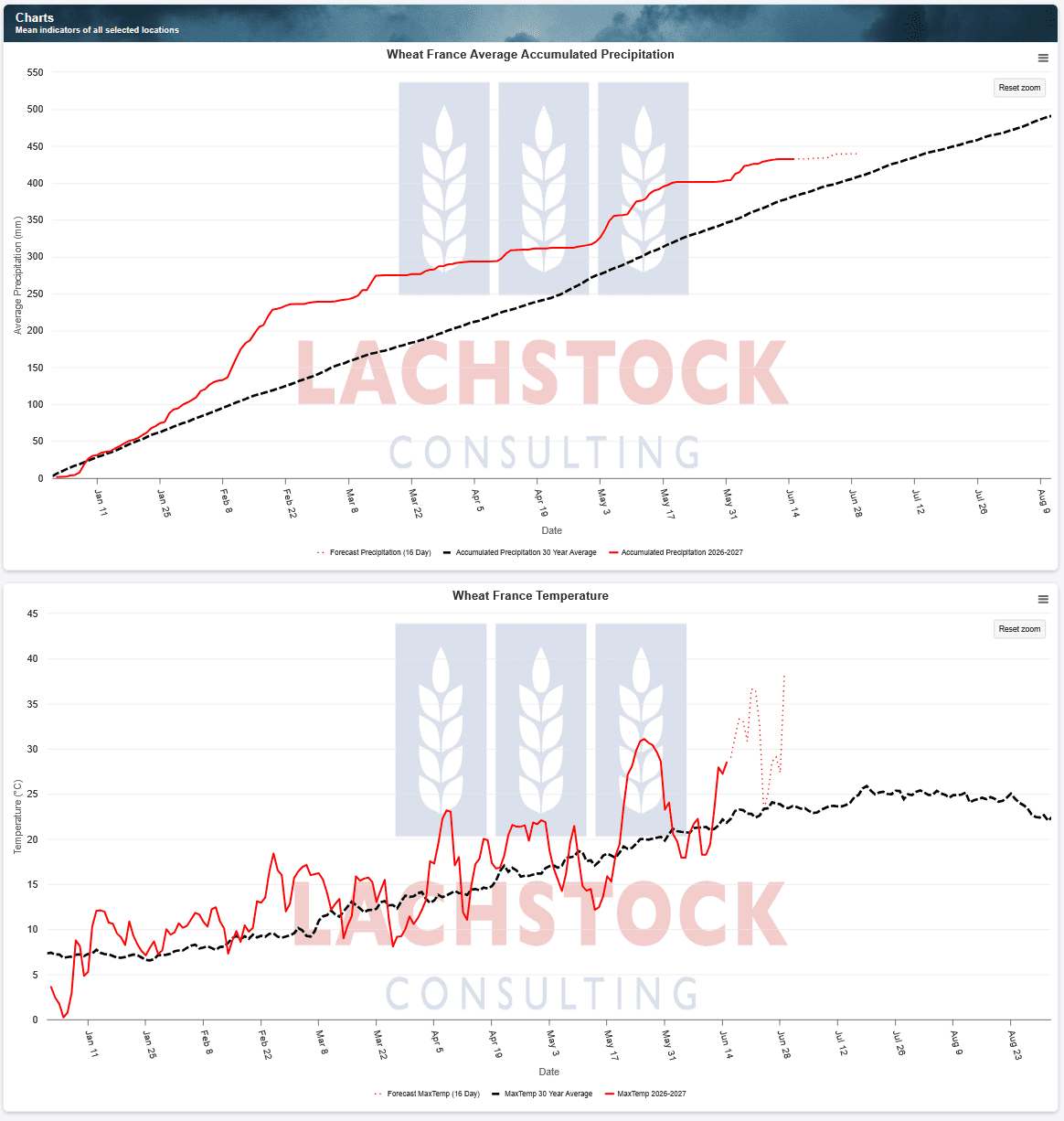

The predicted heat through France has taken a kick higher with temps now set to push close to 40°C – Il fait trop chaud pour mon béret!

It will be interesting to see if we are close enough to harvest to avoid damage to the winter crop.

Markets

The progress made in the ceasefire needs context. Even if this agreement sticks, the market spent some time pondering over the actual timeline, which, given the need to sweep the strait for mines, sort out the orderly exit of over 300 vessels and avoid a relapse (remember, Israel isn’t part of this agreement), will take time. The timing is important (obviously) with the strategic reserve in the US getting painfully low.

The NOPA crush data sent another rocket through veg oil markets – we simply are not producing enough domestic feedstock for the RFS – the function of the market is to encourage imports while it can happen – clean reflection is local tallow prices pushing higher.

Day Ahead – Australia

Getting closer to the next financial year – will we see a flush? Hard to see it given the pull back in values but, for markets like Darling Downs, even with the pull back, values are well above harvest.

Wheat: A rare day-session bid flipped the script. After a week of overnight strength selling off during the day, the pattern reversed Monday — overnight weakness met an aggressive day-session bid that had Chicago and KC each finishing nearly 20c off their lows with highs made late.

Wheat: A rare day-session bid flipped the script. After a week of overnight strength selling off during the day, the pattern reversed Monday — overnight weakness met an aggressive day-session bid that had Chicago and KC each finishing nearly 20c off their lows with highs made late.

WN ended up 5.25c, KWN up 5.5c, and MWN the lone laggard down 2.25c. Spreads in Chicago and KC were firm as the US grower stays sidelined and elevators look to buy, while the Minneapolis curve was flat to mixed.

Implied vol in WN firmed to 24.83pc from 23.61pc. Matif Sep lost €1.00/t and Russian cash sat just under US$240/t fob.

The overnight weakness was easy to source — the US-Iran deal, expected to be signed Friday in Switzerland, sent crude spiralling and risk premium out of grains. But with the market as short as it is and prices opening double digits lower, profit-taking was always a risk.

Several stories chased price: too-wet US harvest conditions, hot and dry Europe, and chatter that China taking French wheat last week means they’re looking.

US inspections of 334k missed the 450k expected, leaving shipments down 6pc yoy.

After the close, winter wheat conditions rose 2pc to 27pc against ideas of unchanged, though with winter wheat already 25pc harvested versus 19pc expected, conditions matter little at this stage.

Spring wheat ratings improved 3pc to 55pc.

Romania is set for a record 13.86 million tonnes (Mt) crop on record yields and expanded area, and a high-pressure ridge will push above-normal temperatures across northwest and central Europe through end-June, keeping the heat-and-dryness story in focus.

Other grains and oilseeds: Corn also turned it around, with CN up 2.75c and CZ up 4.5c. The market is carrying some of wheat’s oversold condition after a one-week record build in the gross managed money short drove net selling of 120k — Friday’s COT showed funds flipping net short corn by 5,325 contracts after being net long since March.

Plenty of weather remains, with complaints of too much rain in the delta and mid-south, but unless it lands at planting or harvest, rain is rarely bearish, and the market is now on the verge of seeing into pollination weather that could flip sentiment quickly.

Corn inspections of 1.637mln bushels missed the 1.750mln expected, leaving shipments up 26pc yoy; conditions rose 1pc to 68pc, matching ideas.

Beans shook off a sluggish overnight to finish well off lows — SN up 5.75c, SMN up $0.70, BON up 9pts, leaving July crush down 3.25c to 363.25. SN tested and held 1100 early before recovering.

The standout was bean oil, which surged after a lower-than-expected NOPA crush of 208.8mln bushels (vs 216.4mln expected, and down from 211.9mln prior) revealed much tighter stocks — oil stocks of 1.735bln lbs sat well below the 1.868bln expected.

The average Apr-May oil draw is -27 versus -236 today; oil remains overused and needs to move higher to entice feedstock imports.

Funds also trimmed bean longs, though soybeans remain net long by nearly 91k. Bean inspections of 523k were in line but left the pace down 20pc yoy.

In canola, ICE settled well off session lows but lower on weaker crude, with Nov down C$5.50/t to 760.40; recent rains and a delayed seeding start mean some intended Prairie acres go unplanted, while Matif canola fell €9.00. Palm was little changed, holding near 4,438 ringgit as Malaysia kept the July CPO export tax at 10pc.

Macro: Risk-on dominated as the US-Iran MoU, to be formally signed June 19, sent oil tumbling to a three-month low and stocks racing higher. WTI sank almost 5pc Monday before steadying above US$81 per barrel in early Asia, while Brent ended near $83 — the retreat has erased the bulk of the conflict-era gains, leaving oil only $10-15/bbl above pre-war levels.

The reopening is unlikely to be immediate: nearly 300 loaded vessels wait to exit the Persian Gulf with roughly as many empties waiting to enter, and Raymond James sees prewar supply levels no earlier than end-July given the logistical hurdles.

The US emergency crude reserve has sunk to its lowest since 1983.

For central banks, the energy unwind eases inflationary pressure just as the Fed, BoE and BoJ meet this week — the FOMC and BoE are expected to hold, the BoJ to hike 25bp, with vigilance still warranted on energy pass-through.

The RBA was expected to hold at 4.35pc today, increasingly likely the peak given softening consumer demand.

US data was mixed: manufacturing output stalled in May for the first time this year as chemical and petroleum declines masked data-centre-linked strength, while oil and gas well drilling rose 5pc, the biggest monthly gain in over four years, as shale responded to higher prices.

On the livestock side, screwworm continues to spread in Texas — now at least a dozen infections, including eight head of cattle — adding urgency to containment, with the sterile-fly plant not operational until November 2027 and the herd already at a 75-year low, a risk that points record beef prices higher.

Local markets: The week started softer in the west of the country with canola back around A$15/t to $807 and new crop $847, wheat was $345 and $357, barley $326 and $324 FIS Albany.

Through the east a similar story with canola down $15 to $760 and new crop $800, wheat was $327 and $345, barley $308 and $315 track Geelong.

Northern feed markets remain around $380 for prompt wheat and $388 barley, while new crop is bid $392 for wheat and $390 for barley Jan+.

Victorian wheat values have steadily worked lower over the past six weeks and are now approaching export parity. However, every time domestic markets look close to finding support, further weakness in global wheat values shifts the goalposts lower, suggesting there may still be downside risk ahead.

HAVE YOUR SAY