Weather: Same same, hot in France, wet in SRW. Indian monsoon caught up a bit but forecasts have turned dry for the next 2 weeks.

Weather: Same same, hot in France, wet in SRW. Indian monsoon caught up a bit but forecasts have turned dry for the next 2 weeks.

Local patterns have been mixed – rain sliding south and the weirdest pattern through SA yesterday that went almost perfectly north to south.

Markets

Dead cat or markets too cheap – US futures are pricing the “what if” domestically – what if it keeps raining and you take SRW production under 300mbu AND China buys a boat or two?

You can’t tell me that it’s just a coincidence that China goes shopping the day after Trump signs the cease fire – remember China gets a chunk of its crude from that region.

Day Ahead – Australia

Rain in parts, not enough in others – that kind of year – as long as the Super El Niño is in play, every single forecast will be traded, regardless of your stored moisture.

US futures up, AUD in check, Trump telling everyone he is the boss. Not sure what to do with all that.

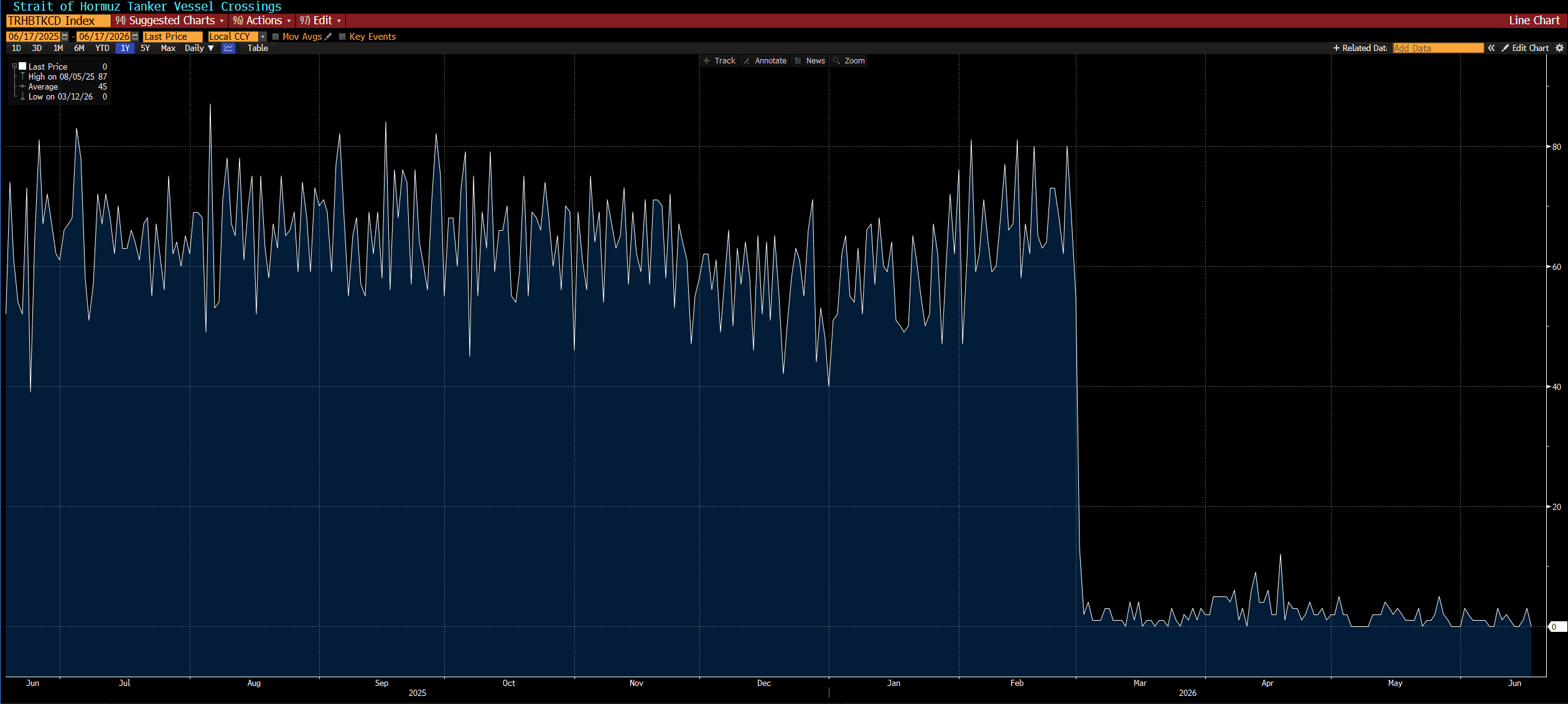

Source: Bloomberg – Strait of Hormuz Tanker Crossings

Wheat: The dominant narrative was Chinese demand inquiry, layered on top of existing weather concerns. All wheat classes were said to have been inquired upon, with widespread speculation pointing to a COFCO-style play — get long futures, seek FOB prices, sell futures — though no confirmed trades surfaced.

The daily soybean flash sale of 372k tonnes to unknown destinations added credibility to the China narrative and kept the buying mood alive.

On the weather front, rain across the US Midwest continues to slow SRW harvest progress, which stood at roughly 25pc as of last Sunday. With ten more days of wet weather forecast and new crop carryout sitting at only 102mb, the market can ill-afford quality downgrades on top of any potential Chinese purchases.

Implied volatility in Chicago wheat jumped to 30.12pc from 25.78pc, and the market is also sitting near 50pc of its record short basis the last COT report, raising the prospect of a sharp short-covering rally.

In Europe, heat is building across northwest and central France with harvest still a few weeks away.

French wheat was excluded from the Algerian tender, which was reportedly awarded mostly to CVB, though a large speculative options trade caught attention — 20,000 lots of December Euronext €250/€260 call spreads traded at €0.80 in a new position (from experience this stinks of a weather fund – I’m sure someone will tell me I’m wrong)

Russian cash fell another US$0.50/t to $237.50, and June export volumes are tracking around 2Mt, up 47pc year-on-year.

EU soft wheat exports reached 22.38Mt by June 14, running 7pc above the same point last season.

On the demand side, Jordan issued a tender for up to 120kt optional-origin milling wheat with a June 23 deadline, and South Korea’s MFG bought 60kt feed wheat from EU/Black Sea origins in a private deal.

Other grains and oilseeds: Corn benefited from the same China demand chatter that drove wheat, with reports of Chinese interest in US corn and sorghum offers, though no confirmed sales emerged.

The underlying weather story remains bearish — abundant rain across the Cornbelt except the northwest and below-normal temperatures pointing to strong early crop development. In a normal year this would be enough to cap any rally, but the market’s sensitivity to all things China is making sellers hesitant to press.

Export expectations for Thursday’s report are 1.1Mt old crop and 800kt new crop.

French corn plantings are estimated at 1.31m hectares as of June 1, down 19pc year-on-year and 13pc below the five-year average. Taiwan’s MFIG bought 65kt feed corn sourced from Brazil.

In soybeans, the USDA flash sale of 372kt to unknown destinations — 60kt old crop, 312kt new — was the story of the day, with consensus leaning toward China as the buyer given the prior day’s reported inquiries.

November beans finished up 3.25c, meal was flat, and bean oil dropped 138 points, taking July crush down 17.25c to 325.50. Meal spreads remained constructive while bean oil continues to face structural headwinds despite the biofuel mandate backdrop, with longs continuing to liquidate.

Double crop bean acres are also at some risk as rain delays in the SRW belt push back planting windows.

EU soybean imports are running 6pc below last year at 13.21Mt by June 14. In canola, ICE futures fell for a fourth consecutive session with the November contract down C$7.80/t to $746.10, dragged lower by bean oil weakness despite some support from crude oil and firmer European rapeseed.

Prairie crop conditions remain favourable with below-normal temperatures and more rain in the forecast, and Manitoba spring planting is 96pc complete.

On the biofuels front, Indonesia’s B50 blending mandate begins July 1,

Cargill is assessing beef tallow biodiesel production in Brazil as US tariffs crimp tallow exports, and a new study flagged expanding biofuel demand as a key driver of US farm profitability.

EU lawmakers cleared the final legislative hurdle for gene-edited crop cultivation.

Macro: The Fed held rates unchanged in a unanimous decision but delivered a hawkish signal, with 80pc of officials now expecting at least one hike before the end of 2026 and inflation forecasts for the year revised sharply higher from 2.7pc to 3.6pc.

US May retail sales came in at +0.9pc month-on-month with broad-based gains across 11 of 13 categories, though in real terms the result was considerably softer once May’s 0.5pc CPI rise is accounted for.

At the G7 summit, Trump declared “I’m the boss” and joined other leaders in pledging fresh support and sanctions for Ukraine, while the group called for a Lebanon ceasefire and committed to diversifying energy supply routes away from the Strait of Hormuz.

Trump added uncertainty by stating that US bombing of Iran could resume if he is dissatisfied with the interim deal, and the emerging nuclear accord is being assessed as potentially weaker than the Obama-era agreement.

The European Council President made contact with the Kremlin in a bid to open Ukraine peace discussions.

Russian crude production fell around 5pc year-on-year to 8.7 million barrels per day in May following Ukrainian strikes on energy infrastructure, and Novorossiysk port came under drone attack. Separately, a corn ship bound for Iran crossed the US blockade line ahead of the interim deal, illustrating the complexity of the Hormuz situation.

In Brazil, President Lula extended his lead in polling ahead of October elections, holding 49.3pc in a hypothetical runoff versus 36.8pc for Flavio Bolsonaro.

Local markets: Through the west canola was softer yesterday, down A$5–6/t to $795 for current season and $830 for new crop, with GM canola around $60 under. Wheat was steady at $340 current season and $352 new crop, while barley was $326 and $323 FIS Albany.

In the east canola eased $5 to $750 with new crop at $785, wheat was $330 and $345, while barley was slightly firmer at $310 and $306 track Geelong.

Grower selling remains limited despite the recent rainfall, with increasing El Niño chatter seeing many producers view old crop grain as a drought hedge. Consumers are having to work harder than they should to source grain, although values remain well relatively low.

SA consumers can continue to rest easy after another 10–20mm fell across much of the Mallee overnight. The strong seasonal start has seen new crop wheat values at Murray Bridge fall from $370 five weeks ago to $335 today for Jan+, while current season wheat has eased from $355 to $340 over the same period.

HAVE YOUR SAY