Weather: Today is the really hot day through Europe – it will be interesting to see if there is follow through strength in Matif tonight.

Weather: Today is the really hot day through Europe – it will be interesting to see if there is follow through strength in Matif tonight.

Markets

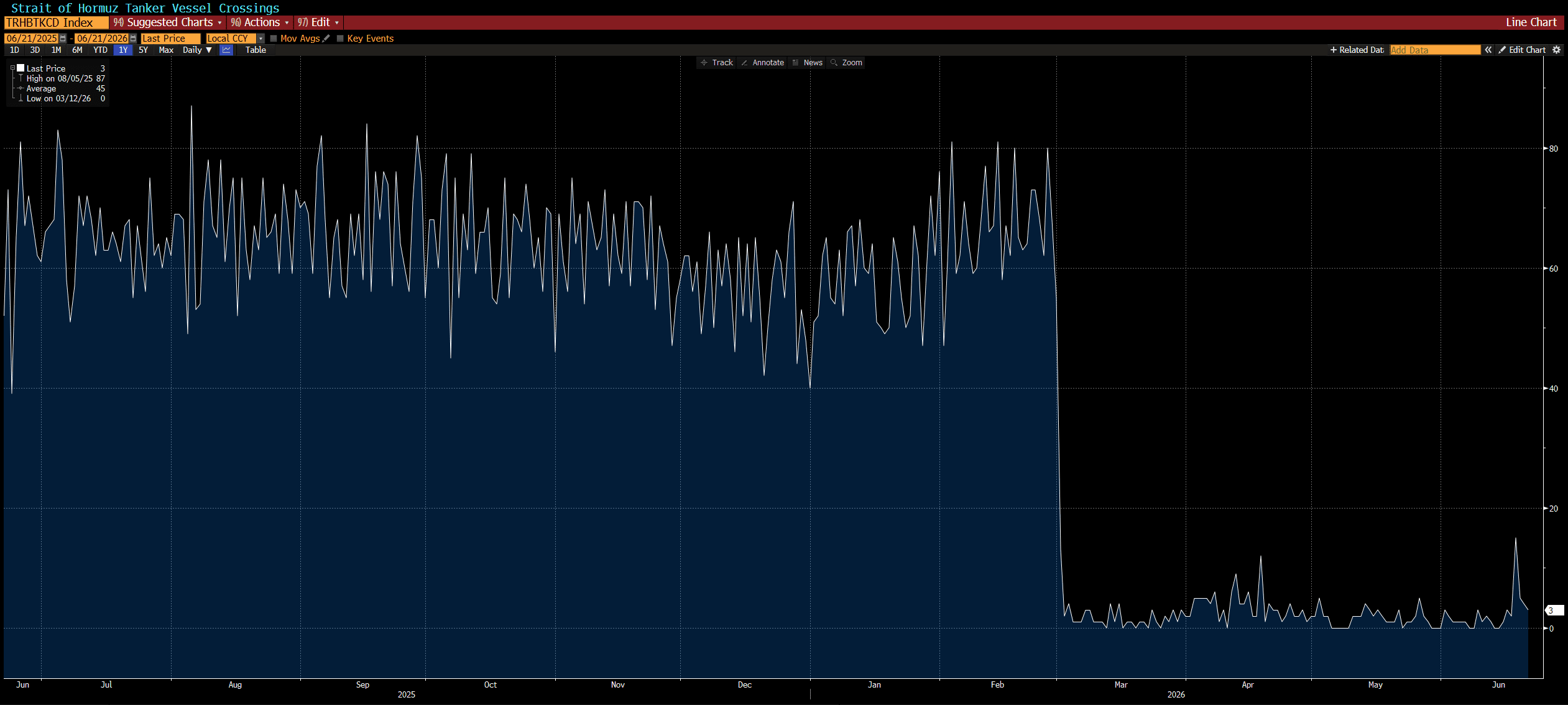

I feel like this was always going to happen – Back to tough talk in the Gulf with Iran basically saying Donald is full of it. What next? It seems as long as Israel are in the background the path forward is complicated.

Long weekend in the US.

Day Ahead – Australia

Amazing rainfall throughout the EP in SA, through to the WD in Vic. Next 8 days a little light on for rainfall but WA still looking good. Markets slow to start the week.

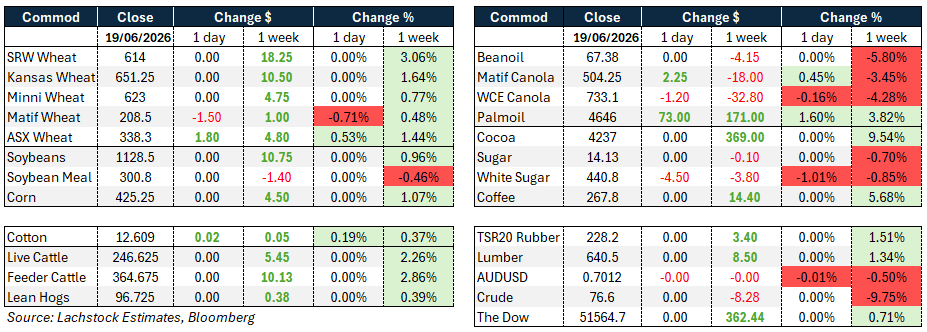

Wheat: US futures markets were closed Friday for the Juneteenth public holiday, leaving Matif as the only active market. The French benchmark slipped € 1.50/t on the day but holds a small weekly gain.

Wheat: US futures markets were closed Friday for the Juneteenth public holiday, leaving Matif as the only active market. The French benchmark slipped € 1.50/t on the day but holds a small weekly gain.

Other grains and oilseeds: As with wheat, US grain and oilseed markets were closed for Juneteenth. Matif canola edged higher on the day but remains under pressure on the week, weighed by the broader pullback in crude oil prices seen over recent sessions.

Macro: Oil prices surged at the open with Brent climbing more than 2 percent after President Trump renewed threats to strike Iran if its Lebanese proxies continued attacking Israel, clouding US-Iran talks underway in Switzerland. Delegations including Vice President Vance and Iranian Foreign Minister Araghchi met to negotiate Iran’s nuclear program and the future of the Strait of Hormuz, with talks running into Monday morning. Vance declared “great progress” though significant hurdles remain, particularly around Lebanon where Iran is demanding an Israeli withdrawal that Israel has flatly rejected.

The AUD was little changed near 0.7009 though is down 0.50pc on the week. US equity futures slipped 0.3pc in early Asia trade.

On the Fed, new Chair Warsh’s first press conference struck a hawkish tone, with the FOMC described as “unambiguous and unanimous” in its commitment to the 2pc inflation target.

ANZ now expects the Fed on hold until Q2 2026 before two 25bp cuts bring the target range to 3.00-3.25pc, noting the FOMC is evenly split on whether rates should move higher this year.

Domestically, Australian markets turn attention to this week’s May CPI, labour force survey and household spending data, with ANZ forecasting trimmed mean inflation up 0.3pc month on month and unemployment edging down to 4.4pc.

HAVE YOUR SAY