Weather: Matif wheat firmed against CME, reflecting the record heat wave through Europe. Rhine water levels are choking fuel shipments to parts of western Europe with levels predicted to fall further.

Weather: Matif wheat firmed against CME, reflecting the record heat wave through Europe. Rhine water levels are choking fuel shipments to parts of western Europe with levels predicted to fall further.

More press about the Indian monsoon – currently running up to 40 percent behind in some areas but it’s only 3 weeks in.

Markets

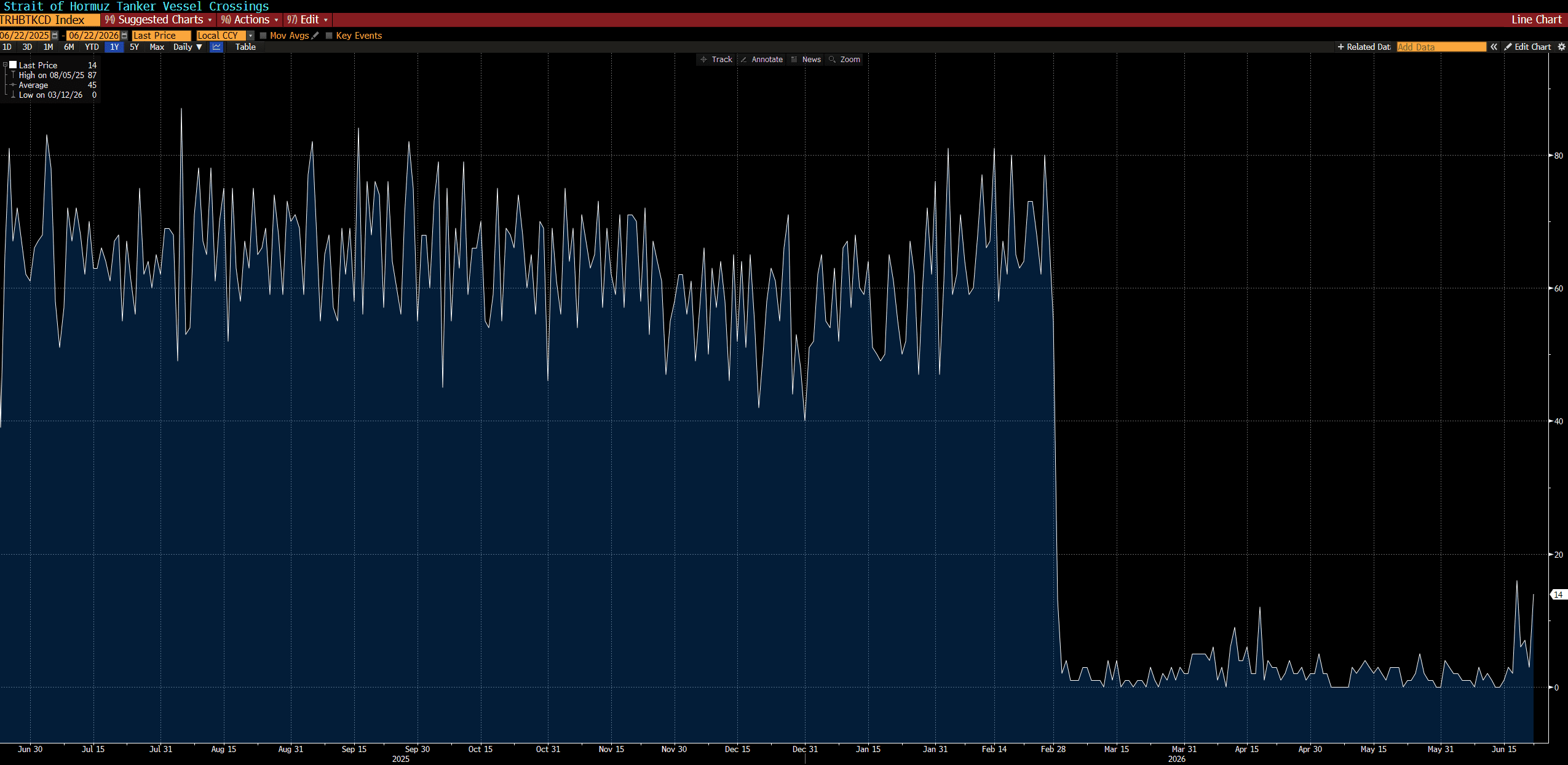

This time for sure… have said that a few times. Markets are really comfortable with the progression despite spot fires still burning. 14 vessels got through the strait yesterday, energy markets pulled back and the world seems to believe this will be the one that works.

Russian FOB is actually holding relatively firm despite amazing conditions.

Day Ahead – Australia

The GIAV Golf Day will keep southern markets quiet.

AUD offsetting the move largely but I don’t expect much to trade today.

Source: Bloomberg – Strait of Hormuz Tanker Crossings

Wheat: A brief overnight rally of 6c in Chicago, driven by escalating Iran/US tensions, quickly reversed when negotiators reported “encouraging progress” in Switzerland. The divergence between US and Paris markets reflects two offsetting forces: a severe European heat wave — Bordeaux forecast above 42°C with red alerts across France and Spain — supported MATIF, while an expected ~90 million tonnes Russian harvest provided a ceiling.

US inspections of 393kt missed the 450kt estimate though the pace remains 15pc above last year.

Crop progress showed winter wheat conditions fell 1pc to 26pc (vs 27pc expected) but harvest progress jumped to 40pc from 25pc, well ahead of the 35pc trade estimate.

Spring wheat fell 1pc to 54pc, below the 56pc estimate.

Ukraine’s 2026/27 crop is forecast at 24.1 million tonnes (Mt), up 3.4pc year on year. Egypt is on track for its 5Mt local procurement target with 4.7Mt purchased so far.

EU wheat faces structural headwinds with Morocco expected to import less following drought recovery and Black Sea competition remaining active.

Other grains and oilseeds: Corn fell alongside wheat and crude with a benign US weather picture dominating. CN lost 6c, CZ fell 4.5c. The Midwest remains wet with no threatening heat expected, and even the ridge forecast for next week is expected to be brief. Corn conditions were unchanged at 68pc, matching estimates, while inspections of 1.454Mt matched the low end but are running 25pc above last year.

Informa pegged corn acreage at 96 million acres (Mac) vs USDA’s 95.3Mac.

European imports may increase over time as heat impacts EU crops, but near term there is ample wheat available for feed at attractive prices.

In soybeans, beans struggled while the complex was driven by bean oil — SN lost 7c, SX fell 1.25c, SMN dropped $1.50, while BON rallied 146 points taking July crush up 19.75c to 326.50 as bean oil had become too cheap relative to competing feedstocks.

Bean inspections of 241k were well below the 375k expected, putting the pace down 19pc year on year. Bean conditions were unchanged at 66pc. Informa put bean acreage at 85.3Mac vs USDA’s 84.7Mac.

AgRural forecasts Brazilian soybean area at a record 49 million hectares (Mha) for 2026/27 but with growth of just 0.9pc — the smallest expansion in 20 consecutive years — citing tight margins, credit constraints and El Niño concerns.

Safras trimmed Brazilian corn output to 139.94Mt.

ICE canola reversed its recent slide with the November contract settling up C$11.00 to $744.10/t, supported by European heat and vegetable oil strength.

The market awaits Statistics Canada’s principal field crop area report on June 30.

Looking further ahead, the EPA’s revised Renewable Fuel Standards are expected to nearly double biomass-based diesel production from soybean oil from 1.3 billion gallons in 2025 to over 2.5 billion gallons by 2027, supportive of domestic crush demand.

Macro: The dominant theme was the US-Iran ceasefire talks in Switzerland, where negotiators reported “encouraging progress” overnight — unwinding the geopolitical risk premium that had briefly lifted commodities.

Crude fell over US$2/barrel as Strait of Hormuz closure risks receded. Trump and VP Vance both floated the idea of unfrozen Iranian assets being directed toward US agricultural purchases.

Fertilizer supply disruption from the strait is beginning to ease with Middle Eastern imports resuming, though US crop nutrient imports fell 44pc year on year in May.

UK PM Starmer announced his resignation with Andy Burnham the frontrunner to succeed him; markets were largely unmoved given the widely anticipated nature of the news, though attention will turn to UK fiscal policy and gilt market stability.

US economic focus this week is on May PCE inflation, expected at 4.1pc y/y, alongside income and spending data to gauge consumer demand.

HAVE YOUR SAY