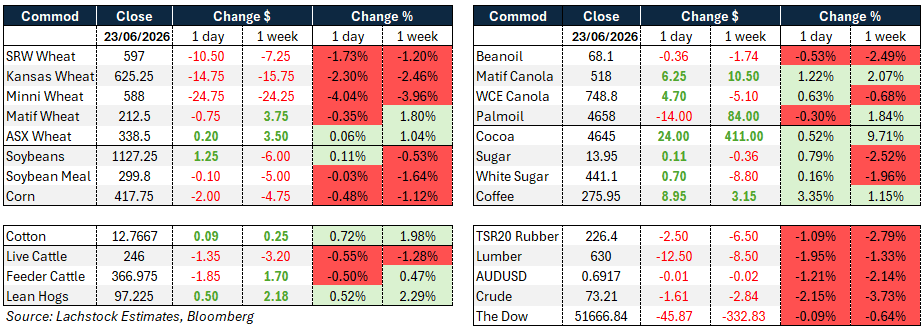

Weather: The heat is on. Europe is sweltering with heat warnings common and records being set. Conjecture around the extent of crop damage will continue = the issue is France. For the most part, Germany and the UK have more moisture under the crop whereas France didnt have this luxury. However, the winter crop should be mature enough that it will avoid complete sizeable revisions in yield and quality

Weather: The heat is on. Europe is sweltering with heat warnings common and records being set. Conjecture around the extent of crop damage will continue = the issue is France. For the most part, Germany and the UK have more moisture under the crop whereas France didnt have this luxury. However, the winter crop should be mature enough that it will avoid complete sizeable revisions in yield and quality

Markets

The heat through France has not been enough to rally futures which maybe tells you what the local market thinks about the impact.

Early doors but EU canola yields have started on the low side – will see how this develops – once again, look the market to gauge the real story. Independent canola strength against energy and a RIN market that just wont break.

AUD key support 0.6913 has been tested, a close below eyeballs 0.6833. This is as much about USD dollar strength as it is question marks over RBA’s next move. FEDWATCH in the US has a staggering 87% chance of a Dec rate hike in the US.

Day Ahead – Australia

The GIAV Golf Day has much of the market seeking a double cheese burger for breakfast.

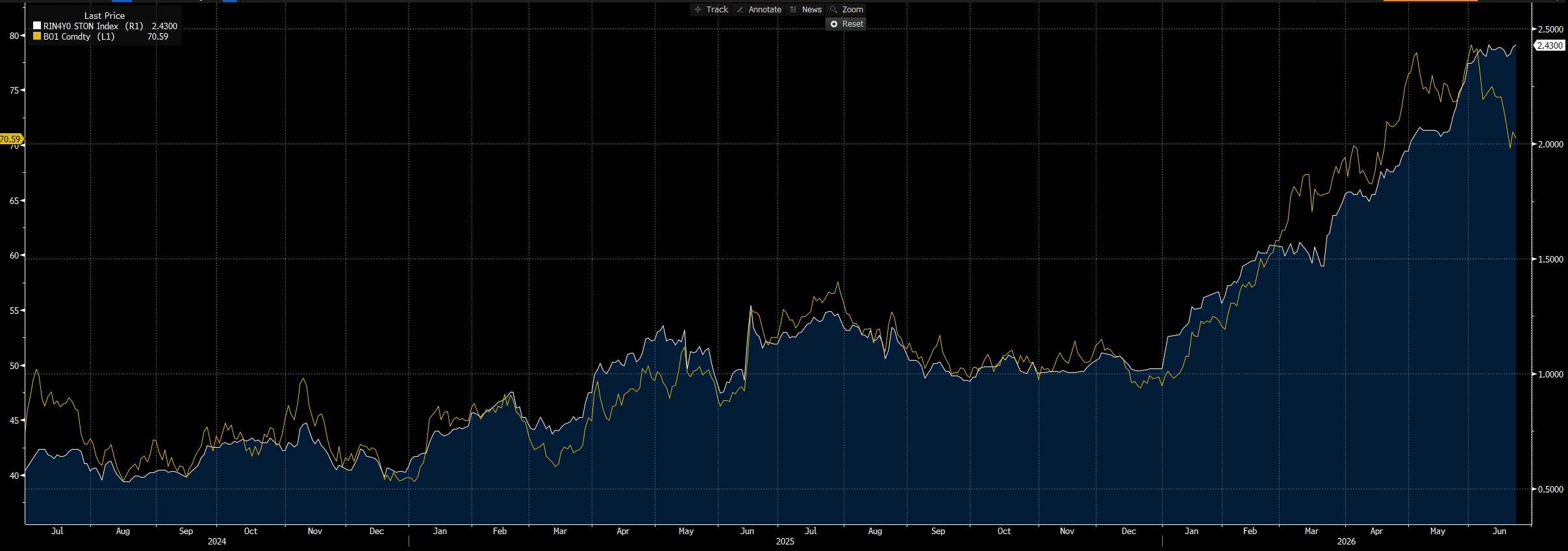

The clean out in wheat has been impressive but, equally so has been the independent strength in canola. In part, this is consistent with the increasing dislocation between the requirements of the Renewable Fuel Standards in the US and available feed stocks. Beanoil has been hit in recent weeks but, given the strength in the D4 RIN market (and assuming refining capacity) any further weakness should find support.

Source: Bloomberg – White line is D4 RIN, yellow line is spot soybean oil futures

Wheat: Wheat was shellacked across the board, with Chicago September down 1.6% to $5.98, Kansas off 14.75c and Minneapolis hardest hit, roughed up for 21c as the liquidation bug caught the spring wheat crowd. Implied vol in WU eased to 25.97% from 27.94% Monday.

Spreads in Chicago were a shade weaker, KC calendars mostly flat, and the Minny curve sold off.

In Paris, Matif September slipped €1.25 and Russian cash fell $2 to $234.25. The pattern held once again, with wheat at its best overnight before unravelling during the day session.

The USDA pegged the winter wheat harvest at 40% complete as of June 21, well ahead of 18% last year and the five-year average of 24%, and that harvest hedge pressure weighed throughout the day.

The crowd north of the border described the Canadian crop as a potential bin buster, with both the northern plains and Canadian wheat areas set for above average precipitation over the next fortnight.

Russian crop optimism remains the answer to any wheat issue, though Sovecon trimmed its 2026 production estimate to 88.9mmt from 90.3mmt on lower area, and separately cut 2026/27 plantings to 25.8m hectares, down 600k from its prior forecast and the lowest since 2014.

Andrey Sizov noted the spring wheat acreage cut may not meaningfully lift prices, as improved early-season export availability could add pressure to the global market even with a smaller crop.

Diesel availability in Russia is also emerging as a concern with harvest approaching.

In Europe the heat is on, with one private suggesting Monday may have been the hottest day ever recorded in France and the heat dome forecast to persist all week, severely impacting crops.

Australian areas have yet to feel El Nino, with both east and west set to see rain this week.

There has been some mention of SRW frost damage discovered, and with all the moisture around at harvest, quality remains a live risk.

Other grains and oilseeds: Corn traded both sides but was ultimately defeated, with CN down 1.75c and CZ off 2.25c, settling at $4.18 for September.

EU corn offered little, with August maize unchanged.

US weather is weighing on any lift French conditions might provide, with some heat showing up for the Midwest next week into July; warmer temperatures would be welcome given how waterlogged the corn belt is today.

Crop progress showed corn good-or-excellent unchanged at 68%.

Demand provided a bright spot, with a daily sale to Mexico of 100k tonnes (30k old, 70k new).

The China $17B deal and the Iran funds story remain demand smoke bombs, with the market unwilling to price either until China lowers tariffs or Iranian assets are confirmed for US ag purchases.

Corn is short with July weather ahead, a stocks/acres risk point next week, and severe EU damage in play.

In the bean complex, SN ended up 1.25c, SMN gained $3.10, and BON lost 56pts, leaving July crush down fractions to 325.75; November beans were unchanged at $11.41½, soybeans good-or-excellent steady at 66%.

There were no new revelations, with the market waiting on China and acres next week. Bean oil still faces the challenge of enticing feedstock imports.

Brazil’s 2026 crush was lifted 0.8% to 63mmt by Abiove on strong harvest and derivative demand.

Funds grew short positions, adding new shorts in corn (now net short over 46,000 contracts) and soybeans (net long shrinking to just below 53,000).

On oilseeds, ICE canola finished higher, overcoming weakness in soyoil and palm, with November up 4.70 to 748.80 as the market “regained traction” after a previous selloff; Matif rapeseed was also higher.

Malaysian palm fell 33 ringgit to 4,639 on weaker soyoil, softer crude and a stronger ringgit.

China may buy a record 1.4mmt-plus of Russian rapeseed oil this season.

The grain and oilseed complex is now waiting on June 30, when StatsCan and the USDA release planted area reports.

Macro: Crude declined after the US rolled back sanctions on Iranian oil, with the temporary waiver unlikely to draw orders from well-stocked Asian refiners and independent Chinese refineries seen as the main buyer.

Iran said $12B of frozen funds were set to be released as talks signalled progress toward formally ending the war, though the US has yet to confirm the amount, with Treasury indicating released money goes into US-controlled escrow earmarked for US food and medical purchases including corn, wheat and soybeans.

Tehran’s version differs, with Foreign Ministry spokesman Baghaei saying the funds would be used freely rather than restricted to US purchases.

Four cargo ships carrying urea, DAP and sulphur crossed the Strait of Hormuz last week bound for Indian ports, supplementing fertiliser buffers, and easing nitrogen prices have offered some relief, though Jefferies noted margins remain negative across all crops into 2026 and 2027.

On the data front, the US S&P Global composite PMI rose 0.7pts to 52.2, with input prices easing to 62.1 and new orders up to 52.4.

The euro area composite rose 1pt to 49.5, still in contraction, with input prices down sharply to 64.7.

The UK composite slipped to 49.4, below consensus, with new orders at their lowest since April 2025, a result read as a strong argument against further tightening.

The AUD was steady at 0.6917, while the Dow eased 45.87 to 51,666.84.

HAVE YOUR SAY