Weather:

Weather:

Initially the heat in Europe was going to be for a few days – now it looks like it will be ongoing for at least another 5-7 days. Much of Europe is not built for this kind of heat and, while the majority of the winter crop will get through unscathed there will be second order impacts that may change demand.

Heat has finally found the corn belt but, right now, its welcomed.

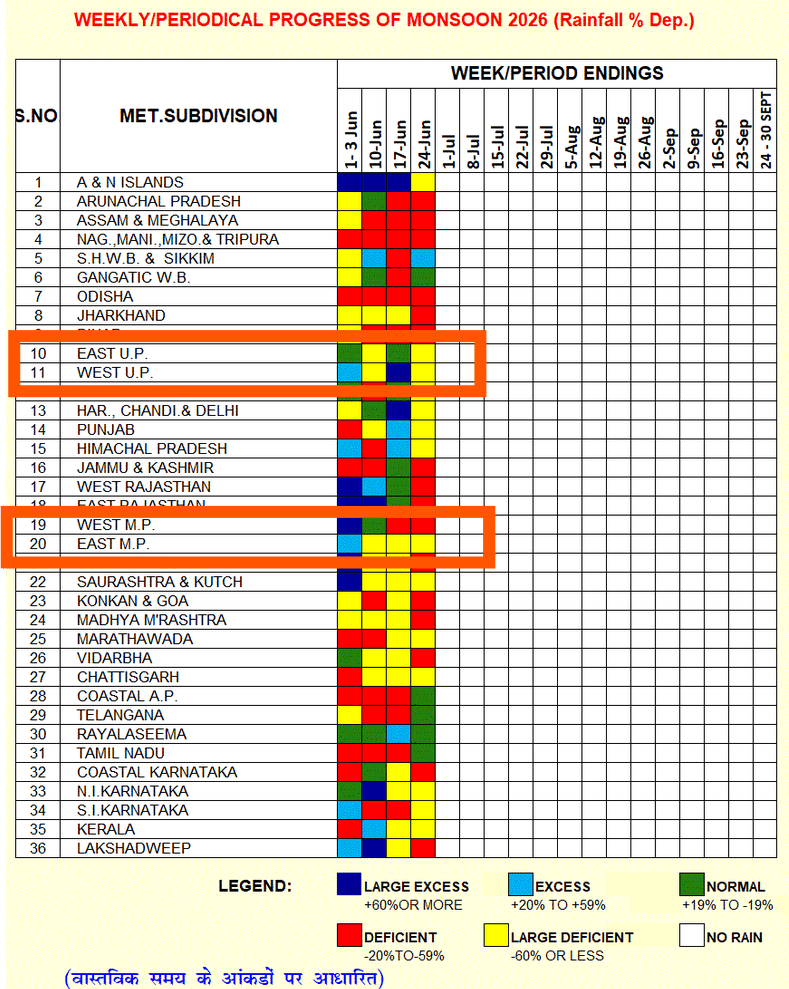

Indian monsoon is lagging – it can certainly catch up but, given the super El Nino talk, this is one to watch.

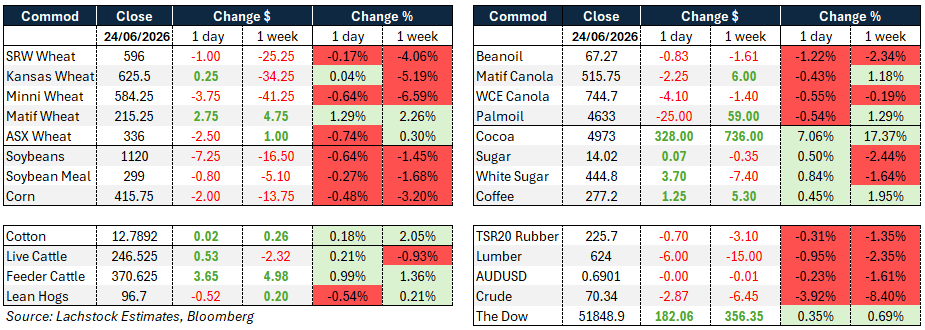

Markets

Oil is tanking (get it… see what i did there) but I’m still scratching my head a little.The deal between Iran and the US seems a little tenuous – Isreal still wants troops in southern Lebanon, Iran wants to charge a toll to use the Strait, i cant see how they have really solved the nuclear issue and the gulf states are unhappy with the generous package Iran has been gifted.Yes, oil is flowing – 19 tankers yesterday but we are still miles behind where we would normally be.

Wheat has no mates – Russia is the millstone around the global market so it was a little interesting to see Sovecon actually reduce their estimates, albeit slightly.

Day Ahead – Australia

Basis is generally pretty firm across the country – as it should be given SEN (Super El Niño) risk. However, we are lagging exports so we are adding back mts to the equation. But, its all a side show with Spring being the main game and, according to Dale Gray (the Vic weather guy) we havent even started talking about the frost risk.

INDIAN GOVT MONSOON PROGRESS

Wheat: Wheat finished mixed after an early rally faded, with Chicago slipping 1c, Kansas ending fractionally higher and Minneapolis off 2.75c. Spreads were weak to flat and WU implied vol eased slightly to 25.91%.

WU was up 10c in the first hour, driven by oppressive EU heat that pushed Aug Maize up €6.50, but a negative US macro backdrop selling off metals, energies and other commodities offset the European pull.

The EU heat is unrelenting and looks set to last another 5-6 days, while a light Indian monsoon so far added to the conversation.

The broader issue remains a sizeable Russian harvest on the way against stoic world demand, with SovEcon trimming its 2026-27 Russian crop forecast to 88.9m tons and Russian cash down $2 to $232.25.

Developing US and Canadian spring wheat crops also offer strong potential, and the super El Nino has yet to stir up trouble in Australia.

Wheat can rally when prompted by macros or heat but struggles to hold overnight gains. Tomorrow’s US wheat sales are expected at 425k.

Other grains and oilseeds: Corn fell to new contract lows after early gains failed to stick, with the market convinced that heavy Midwest rain will lift yields despite complaints of shallow roots and yellow bottoms.

Heat is finally coming to the corn belt late this weekend, welcome at first but a risk if the ridge camps over the central US. Above-average temperatures are expected across the entire eastern half of the US over the next 6-10 days, concentrated in Illinois, Indiana and Ohio, while precipitation stays near normal centrally and above-average further north.

Demand chatter continues around China and now potentially Iran, with Trump claiming Iran will buy upwards of $500 mil in US goods, though traders are sceptical and view any Iranian purchases as too small to move the market.

A BBG survey put corn acres at 95.1m (vs 95.3m March intentions) with stocks 17% higher at 5.4b.

The June 30 acreage report is the next major catalyst, with fund selling showing no sign of letting up.

US corn sales are expected at 950k old + 650k new. Beans have no immediate weather to follow, with China uncertainty lingering and Iran potential now added.

A BBG survey put bean acres at 85.2m (vs 84.7m March intentions) with stocks up 4% yoy at 1.05 bil. RINS suggest trouble meeting the mandate, with D6 RINs at new all-time highs of $2.393/gallon, up nearly 12% yoy, while bean oil remains in a prolonged liquidation phase expected to subside around options expiration.

Analysts forecast soybean export sales of 700k-1.4m tons, with traders watching for signs China is buying US beans again.

Bean sales tomorrow are expected at 300k old + 725k new, meal 225k old + 125k new, and bean oil 4k old + 2.5k new.

Canola eased as focus shifted to the November contract, dipping C$1.80 to C$744.30 and remaining below its 20- and 50-day moving averages.

Lower crude has pulled the oilseed down lately, with WTI off around US$6/bbl on the week and July soyoil down 2.08c/lb as more tankers transited the Strait of Hormuz.

Macro: Oil prices have fallen sharply in June and are nearly back to pre-conflict levels, with the focus now on whether higher March-May oil will drive broader inflation and unanchor expectations.

Market-based measures argue against this: the 5y5y inflation swap is around 2.34%, down from 2.48% in mid-May, and the 10-yr breakeven has fallen more sharply, with both moves starting before last week’s FOMC.

May PCE is due tonight (10:30pm AEST), with the headline deflator forecast +0.4% m/m and core +0.3% m/m, though the sharp oil fall has taken some punch out of the headline.

More focus falls on core and how inflation is performing outside energy-sensitive sectors, with the market-based core PCE easing gradually over the first four months suggesting no pass-through so far.

Durable goods prices, up 0.6% m/m in April on tariff effects, are also worth watching, with the key question being whether tariff effects unwind soon or prove more persistent.

Local: Through the west of the country bids were slightly firmer yesterday with canola $802 and new crop $840, wheat $341 and $353, barley $328 for both current and new crop FIS Albany.

In the east canola lifted $10 to $755 current season and $795 new crop, wheat was $326 and $342, barley $310 and $315 track Geelong.

While most climate models are now pointing towards an El Niño, there is still uncertainty around what it means for rainfall. Most agree warmer temperatures are likely, with many Victorian growers reporting crops are already 2–4 weeks ahead of normal. If that continues, it could increase frost risk later in the season, particularly if cloud cover is reduced.

A softer AUD has provided a little support to lentil values, but bids remain around $650 delivered port. There are still significant grower stocks to be marketed across the east, which will keep a lid on things for quite some time.

HAVE YOUR SAY