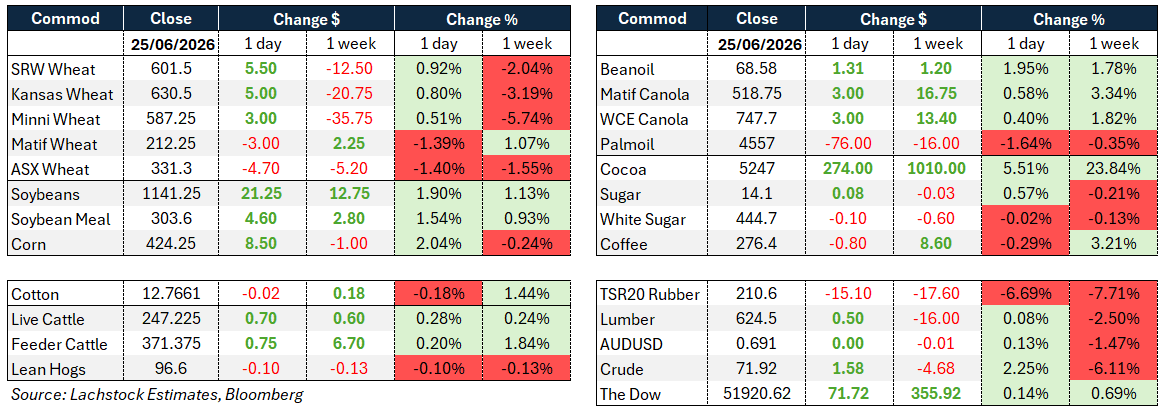

Weather:

Weather:

France is still being belted with more heat coming in the back of the forecast. Debate remains over the impact on winter crop but corn will definitely suffer – some saying the French wheat crop could fall below 10 million tonnes (Mt).

Indian monsoon is front of mind – not unusual for the monsoon to have a slow start so way too early to call a problem.

NSW looking good for the next 8 days.

Markets

More of the same – wheat showed some strength but it certainly isn’t concerned about much. Huge Russian crop on the way and the EU heat shouldn’t do excessive damage (aside from Englishman sunburn).

RBA minutes are due out on the 30th – super interesting – energy lead inflation is abating, housing is slowing and clearance rates are falling yet employment is outperforming. what to do?

Day Ahead – Australia

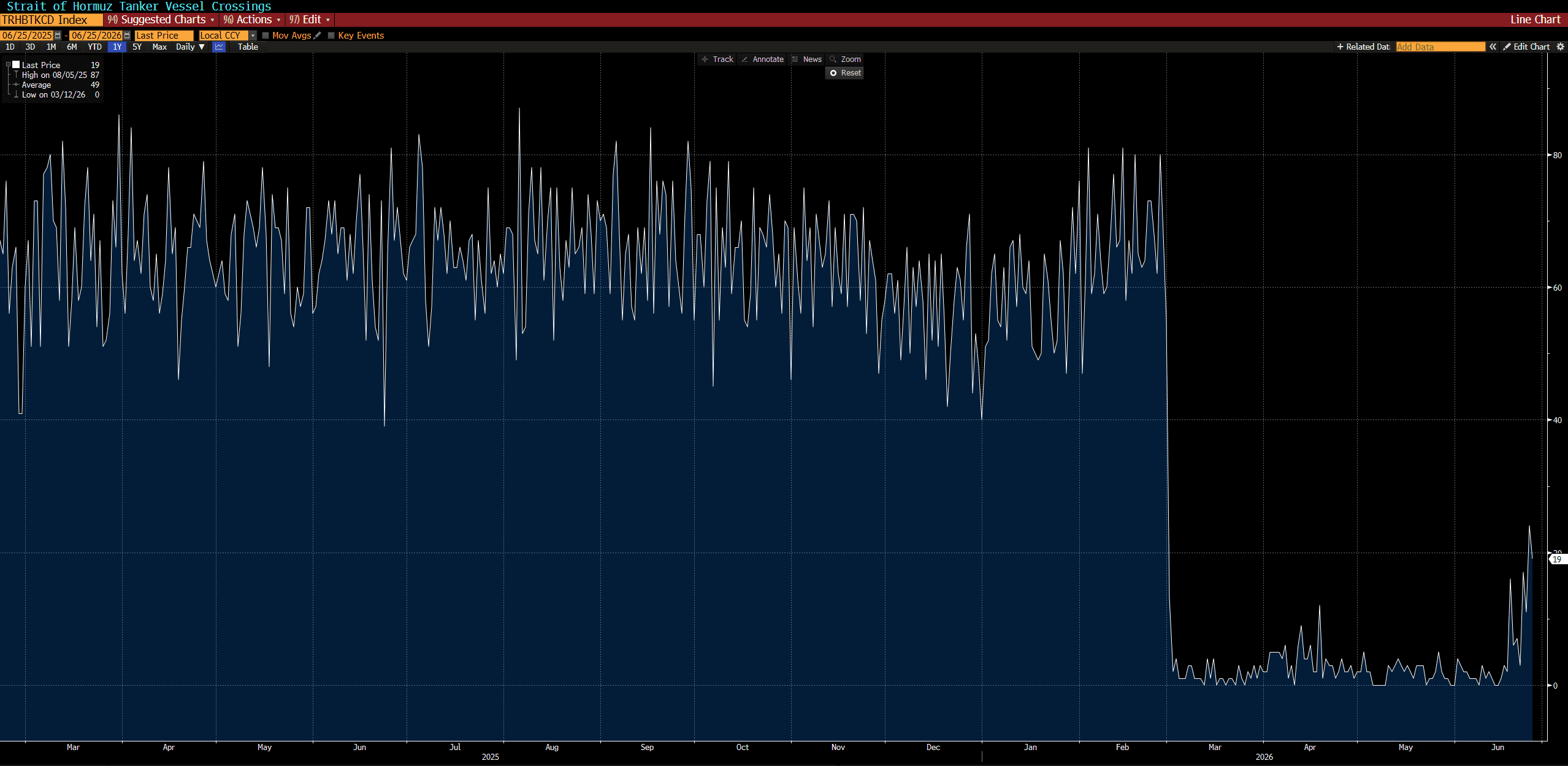

AUD lower, canola higher, rain on the way, tankers getting shot by something or someone, mmm, financial year end also at play

flat for me.

Strait of Hormuz tanker crossings – source: Bloomberg

Wheat: Wheat held its gains into the close, a change of pace that became apparent as lunchtime approached with the rally still intact. WU added 5.5c, KWU 5c, and MWU eased 1.75c, with only Minneapolis lagging. Spreads in Chicago were narrowly mixed to firm, the KC curve weak in KWN then flat to firm further down, and Minneapolis calendars firm in front before turning lower to mixed U forward.

Implied vol in WU went out at 26.95pc against 25.91pc Wednesday. Matif Sep lost €3.50 and Russian cash sits near $232.

It helped that corn never wavered and that the macro backdrop was constructive with crude finally turning around.

Matif was the one market with rumoured Chinese interest and took a breather after its recent run — nothing was heard traded but China was said to be taking a look.

Weekly sales came in at 504.5k against ideas of 425k, well clear of the 315k needed to match the USDA, split 139k HRW, 117.2k WW, 116.5k HRS, 106.6k SRW, and 25.2k DUR, with Mexico and Japan the top buyers.

On the supply side, Rusagrotrans pegs Russia’s June exports at 2.26Mt, up 66pc year-on-year, with the season potentially reaching 47.7Mt versus 42.2Mt last year, and the IGC lifted global wheat production 1Mt to 821Mt on a larger Russian crop.

The pull of the oncoming Russian harvest is the weight here, though the cries for diesel in the BSEA are getting louder.

SRW is no longer outrageously priced and HRW is working with 150m bu less supply this season. 600 WU could act as a magnet until the report early next week.

Other grains and oilseeds: Beans were the drivers. SN gained 18.75c, SMN rallied $4.60, and BON added 135 pts to leave July crush up 6.25c at 329.50. The push came from weekly sales confirming Chinese purchases plus rumours they were after more US for Sep/Oct, with both products finishing higher.

Bean sales were 455k old against ideas of 300k and 902k new against 725k estimates — China took 202k and the unknown 792k.

A looming Argentine processor strike, centred on a pay dispute, added risk premium to the complex, while bean oil may finally be past its recent liquidation.

Old crop product sales were 153k meal against 250k expected and just 0.9k bean oil against 5k.

Corn was firm throughout, CN up 7.75c and CZ 8.25c higher, helped by higher crude and a longer stretch of heat heading to the US from late this weekend into July — welcome warmth for now, but the market won’t hesitate to rebuild production risk premium if it overstays.

Corn sales were 743k old against 950k expected and 736k new against 650k ideas, Mexico and Japan the largest buyers.

Across the trade this was read as short-covering ahead of month and quarter end, with the CFTC showing growing grain shorts, particularly in corn.

France remains the epicentre of the European heat wave, with a record 30C daily average Wednesday and Expana warning French corn output could fall below 10m tons, the lowest in decades.

The IGC sees 2026-27 global total grains at 2.426 billion tonnes, down from 2.488billion tonnes, with stocks tightening to 618Mt.

On oilseeds, Chinese crushers have made inquiries for fresh Australian canola in anticipation of a trade pact, with private processors looking at Q4 delivery; Zhengzhou rapeseed meal fell as much as 2.8pc.

Palm posted its biggest drop in over a month on weaker crude, soft soy oil and a stronger ringgit, the Sep contract down 1.96pc at 4,542 ringgit. Corn weather season is officially here — beneficial to uh oh can happen in no time.

Macro: A ship was struck by an unknown projectile in the Strait of Hormuz, damaging the bridge, with the WSJ reporting an Iranian IRGC attack on a Singapore-flagged vessel, though a White House official said it was too soon to assign blame and noted no deaths or environmental damage. The incident undermined what had been a rapid reopening of the chokepoint, with Brent touching session highs above $75 after at least three vessels — including two supertankers — turned back earlier in the day following Iranian Navy warnings.

The IMO paused its evacuation operations in response. Crude turning around gave grains a constructive backdrop into the close.

On US inflation, both the PCE deflator and the core measure remain too high relative to target, underpinning expectations the Fed holds steady into mid-2027.

The breakdown was more encouraging: services rose 0.5pc m/m but the gain was concentrated in finance and insurance (+1.2pc) and transportation (+0.8pc), with imputed portfolio fees doing much of the work. Market-based PCE, about 85pc of the index, rose 0.24pc m/m, down from 0.28pc in April and 0.42pc in February, suggesting no broadening of pressures outside energy. Durable goods slipped 0.02pc m/m, though it’s too early to call that an easing of tariff pressure without a run of soft prints. Weather, politics, and a COT to consider tomorrow takes us into the weekend.

Local: In the west of the country bids were steady yesterday with current season canola A$800/t and new crop $842, wheat was softer at $338 and $356, while barley was $315 and $331 FIS Albany.

Through the east markets were largely unchanged with canola $752 and new crop $792, wheat $326 and $345, and barley $312 and $310 track Geelong.

The barley balance sheet continues to tighten, with freight enquiries indicating another export cargo is likely to load out of Geelong later this year.

Northern live export feeder steers continue to hold around A$4/kg ex Darwin despite increasing mustering activity, as strong domestic restocker and feedlot demand limits supply to exporters. However, a weaker rupiah and Indonesian government beef price caps continue to squeeze feedlot margins and create mounting headwinds for demand.

HAVE YOUR SAY