Weather:

Weather:

Rains forecast for the corn belt add to the weight in the market, even with some predicted heat.

Indian monsoon lags, markets starting to react.

Good falls for Aussie.

Still warm in EU but the peak heat has past.

Markets

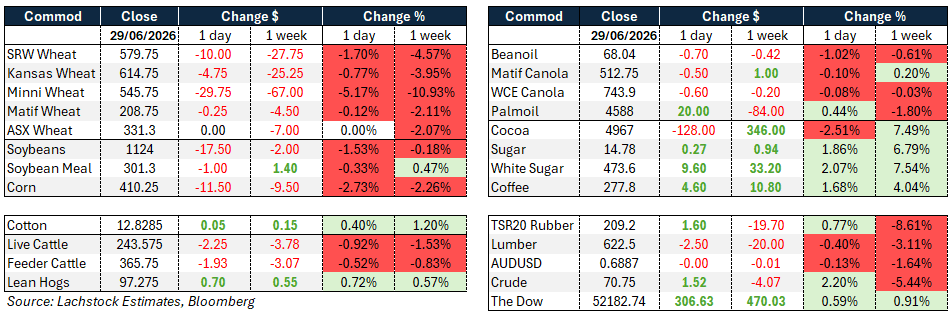

Wheat is unilaterally testing April lows. The all important June stocks in all positions and planted are report will be published tonight – historically a market mover. Seems the consensus is for higher wheat acres, another tick in the sell-the-living-suitcase out of a relatively tight balance sheet.

Energy markets have called an end to the conflict. Despite 80 mines bobbing around in the strait, Russia putting their hand up saying that they need some buffer refined product inventory and the fact that the guys running these conflicts are Donald and Vlad….but yeah, everything is fine.

I get it, inventory flows and we find new bottlenecks which essentially means that spot crude eventually doesn’t have a bid, additionally, as per the terms of Don’s agreement, Iran get sell crude. But, that’s assuming that nothing goes wrong from here.

Day Ahead – Australia

With central Vic getting well over an inch and the outlook calling for more widespread rainfall its hard to see what rallies commodities for the moment – I’m becoming more convinced that the AUD has some serious headwinds which will help values stabilise.

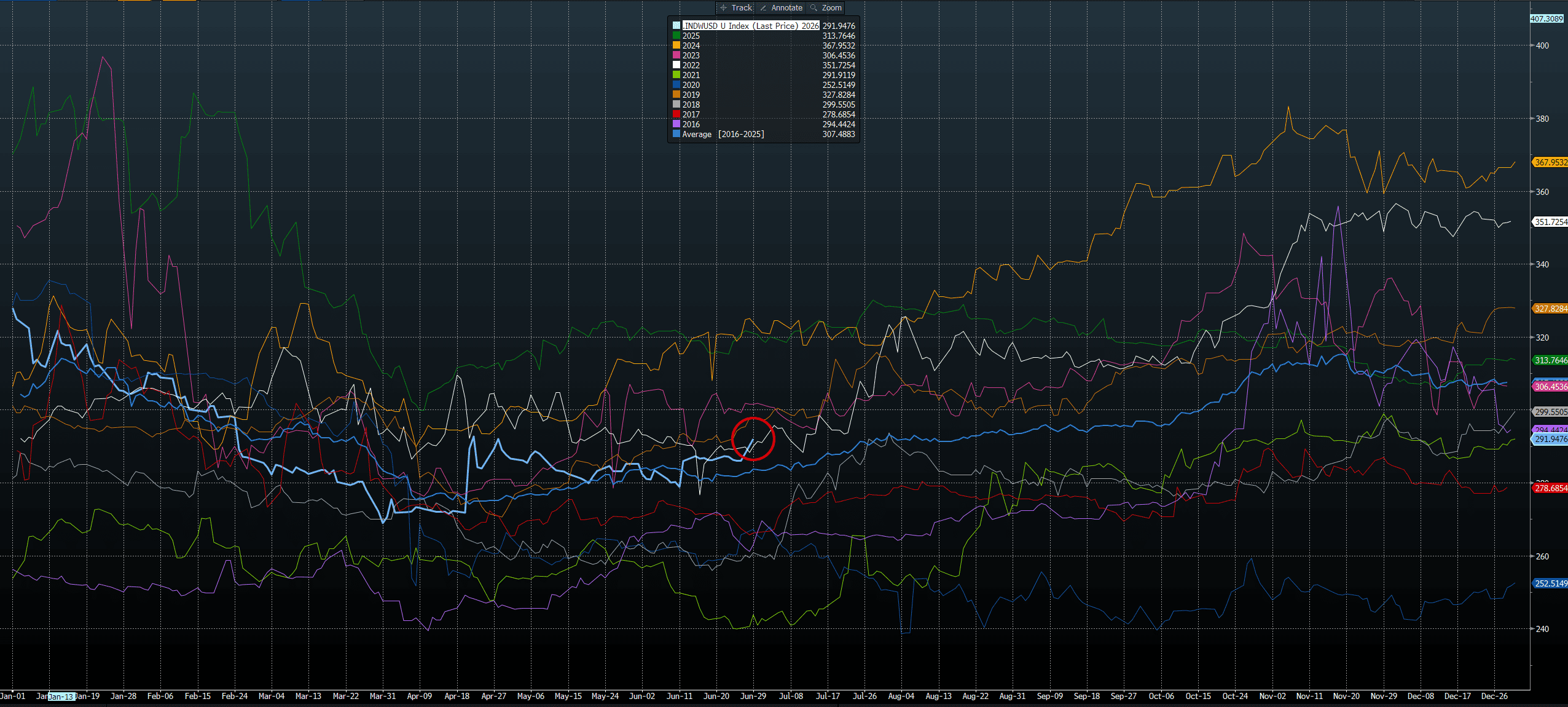

Source: Bloomberg. Indian Domestic Wheat in US$/t.

Wheat: Wheat unwound with the rest of the complex as funds flipped from buyers to sellers ahead of tonight’s USDA acreage and quarterly stocks reports and the June/quarter-end book-squaring.

WU led the Chicago board lower, settling at $5.78, with the easing Corn Belt weather outlook and the steady retracement of the Iran risk premium doing most of the damage.

Minneapolis was the standout loser, MWU shedding better than 5 percent as spring wheat got caught in the broader liquidation — the bullish reversals printed last week are now on the verge of being taken out, with prices grinding lower despite hot conditions, because the forecast keeps offering rain.

Hedgepoint pegs all-wheat acreage at 43.9m, up on the March intentions, which frames tonight’s print as a potential headwind if confirmed.

Offshore, the global balance sheet stays comfortable — Argus lifted its 2026-27 Russian crop to 91.2 million tonnes (Mt) and Egypt’s 2026 imports are running 5.3pc below last year.

KC held in best of the three US classes, the HRW discount story and a firmer protein bid cushioning the move, while Matif was nearly unchanged and ASX flat.

Other grains and oilseeds: Corn was the heaviest of the row crops, CU off 3.1pc at $4.08¾ as the same forces — fund liquidation, end-of-quarter positioning and a wetter, friendlier six-to-ten-day outlook — converged on the board.

The NWS six-to-ten-day shows above-average rain across much of the Belt even as the heat builds, with the eleven-to-fifteen-day turning drier; ample moisture into pollination is hard for the bulls to fight.

Hedgepoint looks for corn acreage to slip 300,000 to 95m, with few changes expected to the March figures given the clean planting window, though elevated input costs are a wildcard. SX followed at $11.37½, dragged by the broad risk-off and spillover into the crush — BON gave back ground despite firmer crude.

Matif canola was the quiet outperformer, November actually closing €1.00/t higher on the week even as ICE canola new-crop contracts reversed gains to finish lower; the old-crop July held up (up C$2.30/t) but November eased C$0.60, pressured by the sharp Chicago soy break and softer European rapeseed, with Malaysian palm steady.

StatsCan’s planted-area report tonight is the swing factor for canola — trade looks for 22.1–22.8m acres against 21.6m last year and a 21.9m five-year average.

Palm firmed modestly on the day but remains down on the week.

Macro: Crude was the mover, WTI up 2.2pc to $70.75 on a tightening physical picture even as the geopolitical premium bleeds out elsewhere.

Tankers keep transiting Hormuz despite a pair of weekend attacks — a laden VLCC on Saturday and a boxship before it — with roughly 80 mines reported in the main corridor and the JMIC lifting its threat level back to “substantial.”

The US-Iran standstill and the first Ras Tanura load since the ceasefire are easing flows, but the supply side found fresh support from Russia: Putin conceded a domestic fuel “deficit” for the first time after Ukrainian drones hit refineries in Krasnodar and Yaroslavl, with Novak reviewing fuel exports to protect domestic supply.

The Dow added 306 points to a fresh 52,182 on a tech-led bid.

AUDUSD was effectively unchanged at 0.6887, holding near the bottom of the analyst range — the firmer oil tape and risk-on equities not enough to lift the Aussie as quarter-end USD demand capped it into tonight’s US data.

Local: The week started steady in the west of the country with canola bid at A$805/t and new crop $840, wheat was $332 and $343, while barley was $328 and $330 FIS Albany.

In the east, canola eased slightly to $750 while new crop was $792, wheat was $326 and $343, and barley $310 and $312 track Geelong.

Delivered wheat markets in the south continue to soften, with Murray Bridge trading in the low $330s for Jan+, Bendigo bid at $335 and the Darling Downs at $383.

What a difference two months can make through northern Australia, with winter crop plantings moving from just 0–20pc complete to now nearing 100pc. Given where we are in the season, chickpeas and barley have increased their footprint at the expense of canola and wheat.

HAVE YOUR SAY