Weather:

Weather:

Nothing to see here – US corn conditions are near perfect with any heat concerns pretty much evaporating. The all crucial late July, early Aug pollination window looks like it will be benign from a heat perspective.

My favourite Indian monsoon pace website is down but things look like they are set to catch up – rainfall forecasts through the monsoon are notoriously bad but there is some convergence on the forecast.

Still pretty wet in Canada – much of the canola belt is running over 100mm ahead of long term averages.

Markets

Wheat is awkwardly trying to work out if it’s too cheap or too expensive. The spec suggests that it’s too expensive, Matif premium to Chicago is at decile 4 so not convincing but wheat/corn is at decile 7 (more a corn story than a wheat story). There is a level of risk premium just in case Xi comes shopping and the fact the US balance sheet is relatively tight – however global stocks are, today at least, comfortable.

Day Ahead – Australia

Wet – really wet in parts of Australia. It’s all about spring but we are building a decent buffer that arguably takes a sub 20 million tonnes (Mt) crop off the cards. Maybe that fella can call a low crop again – its pretty much rained since he made the 21.4Mt wheat crop call.

More of the same today – barley is sniffing around export parity in some markets – reports that Downs new crop cereal hay could be close to A$500/t feel expensive but probably carry some decent freight protection.

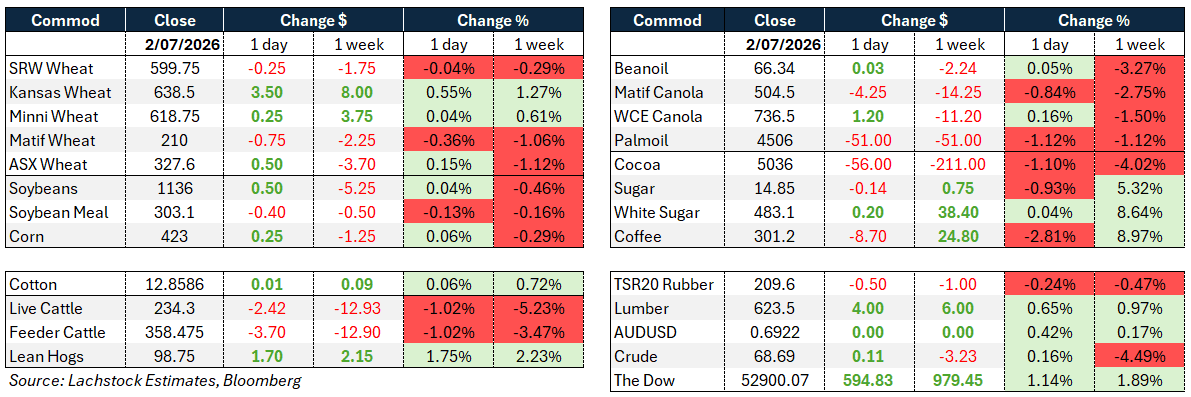

Wheat: SRW closed US599.75c/bu, off a touch on the day and 1.75c lower for the week. Kansas kept outperforming, up 3.50c to 638.50c, up 8.00c on the week. Minneapolis added a similar amount to 618.75. Matif eased to €210/t, down 2.25/t on the week, and ASX firmed slightly on the day to A$327.6/t but remains 3.70/t lower for the week.

Wheat: SRW closed US599.75c/bu, off a touch on the day and 1.75c lower for the week. Kansas kept outperforming, up 3.50c to 638.50c, up 8.00c on the week. Minneapolis added a similar amount to 618.75. Matif eased to €210/t, down 2.25/t on the week, and ASX firmed slightly on the day to A$327.6/t but remains 3.70/t lower for the week.

Wheat continues to trade as the strongest of the three majors, and the logic behind that is straightforward: US winter wheat output is tracking near historic lows, Canadian production is down roughly 6 percent year-on-year, Russian planting is being constrained by input costs, and European crops are still carrying the potential for heatwave damage.

With the US balance sheet tighter than trade assumptions and wheat holding the largest net short of the row crops, the setup favours further short-covering rather than a fresh bearish catalyst. Kansas’ relative strength reflects where the production risk is concentrated.

Other grains and oilseeds: Soybeans closed 1136, roughly flat on the day, down 5.25 on the week. Meal eased to 303.1, corn firmed slightly to 423 — both little changed week-on-week.

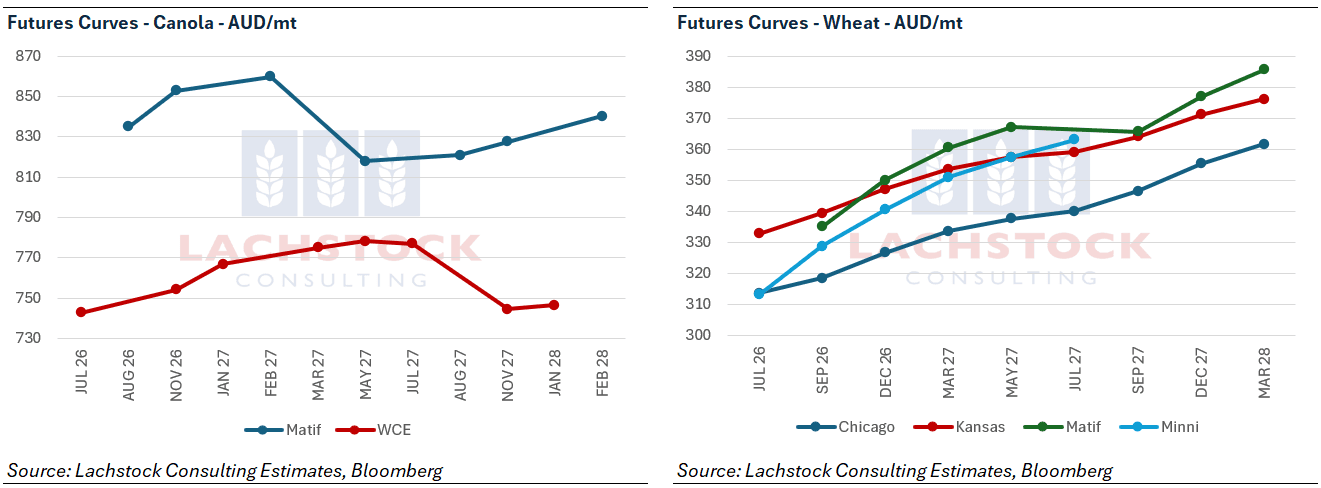

Canola diverged: Matif down €4.25/t to 504.5 (down 14.25 for the week), WCE up C$1.20/t to 736.5 but still 11.20 lower on the week.

Palm oil fell again to 4506.

Cocoa dropped sharply, down 56 on the day and over 200 on the week to 5036; sugar and coffee both firmed on the day despite recent volatility.

Corn and beans took their cue from weather rather than fundamentals — forecasts now show the Corn Belt heat breaking within 24-48 hours, with a return to near-normal temperatures through mid-July arriving right as pollination gets underway.

Beans also caught a bid on renewed talk of Chinese futures buying, though that optimism sits against soft data: old-crop export sales for the week ended June 25 hit a marketing-year low, well below trade expectations.

Canola’s move is a weather story, not a demand one. StatsCan’s June 30 report put 2026-27 seedings at a record 23.44 million acres, but sustained Prairie rain — with flooding already showing in Alberta, Saskatchewan and Manitoba — has traders questioning whether that acreage converts to a normal harvest.

RBC’s desk in Winnipeg still frames November canola inside C$730-750, with a drier turn opening room below C$720 and continued wet weather keeping it pinned near the top. Crush demand remains firm regardless, with Canadian plants near capacity and further Chinese interest reported.

Macro: The Dow hit a fresh high, up 594.83 on the day and 979.45 for the week to 52900.07. Crude firmed to 68.69 but is still down 3.23 on the week.

AUD/USD held flat at 0.6922.

Equities rallied after a soft June jobs print — 57,000 added versus roughly double that expected — which markets read as reducing near-term hike risk.

Capital Economics pushed back on that read, arguing the data doesn’t shift their view that the Fed is more likely to hike again this year than the market is pricing. FEDWATCH has reduced the chance of a Dec hike from 81pc to 77pc.

That debate now has a political overlay: the Supreme Court blocked the White House’s attempt to remove Governor Cook this week, though the administration has signalled it will pursue a procedurally cleaner path to the same end, and separately is working to install its preferred pick atop the Atlanta Fed.

None of it is moving markets yet, but it’s a growing source of Fed-independence risk worth watching into the second half.

Local: In the west of the country bids were steady yesterday with canola bid around A$800/t and new crop $835, wheat was $340 and $350, and barley $325 and $335 FIS Albany.

Through the east, canola was $752 and $795 for new crop, wheat was $325 and $345, and barley $308 and $310 track Geelong.

Growers will be looking for some dry weather through SA and Vic over the next few weeks, as waterlogging is now starting to have an adverse effect, particularly on lentil crops.

Old crop protein spreads remain wide, with H1 around $385–390 delivered Melbourne, roughly a $40 premium to APW. Given the season is shaping up, it feels increasingly likely that it will be another low-protein year.

Despite China’s beef imports collapsing to just 7.8kt in June following the 55pc tariff, Australia’s total beef exports still reached 147kt, with the US, Japan and Korea more than absorbing the lost demand – highlighting just how strong global appetite for Australian beef remains.

HAVE YOUR SAY