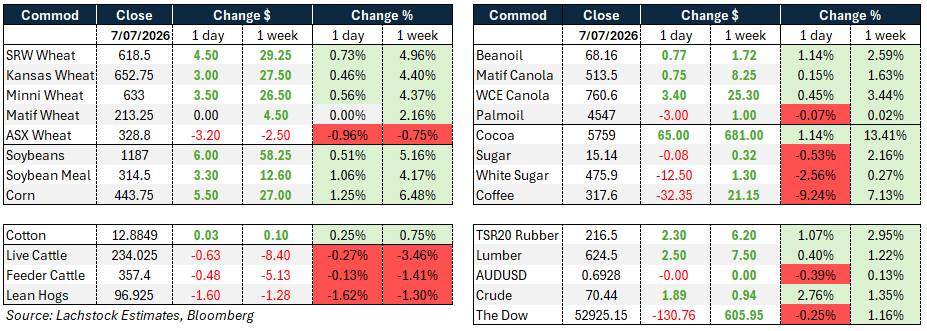

Weather:

Weather:

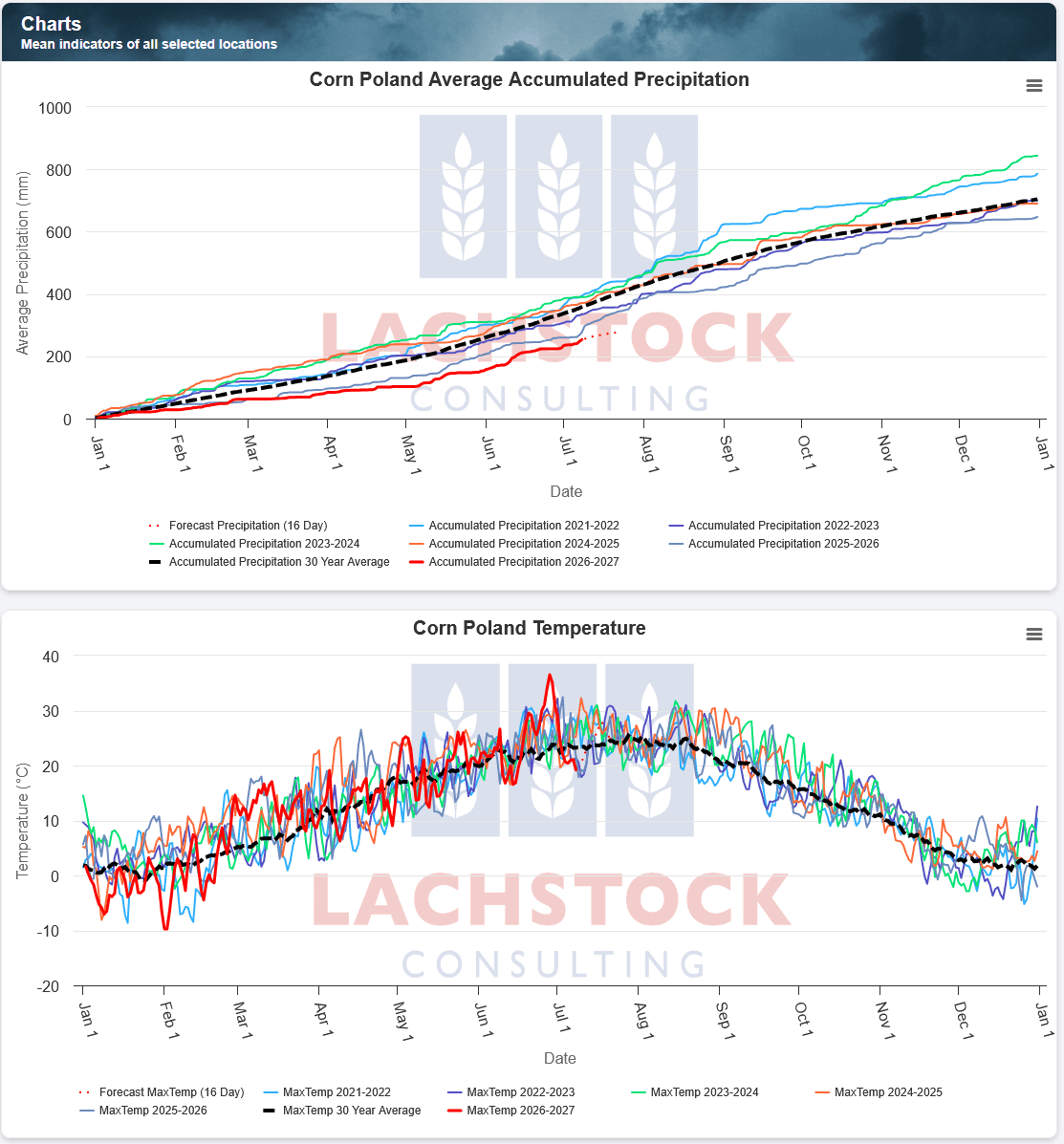

The heat is persisting in the EU with more damage to the corn crop expected. To this point, it has largely been a French story but, increasingly, this is an EU and Black Sea region story.

Countries like Poland are running over 100mm behind normal with temps over 11°C above normal.

Indian Monsoon is predicted to catch up a little this week.

Markets

Donald has his finger over the button and Russia/Ukraine is kicking off again – yes, energy markets have moved but, really, grains almost completely ignore war.

The clear strategy by Ukraine to hit Russian energy infrastructure, and the fact Russia has been potting Ukrainian rail isn’t overly bullish their supply chain.

The recent CFTC shows a bunch of new shorts into the corn market. Given the weather in the US/EU and the chance China comes shopping, the short would be a little nervous.

Day Ahead – Australia

Canola should have another up day – cereals should be largely flat, although, ocean freight spreads are certainly helping our competitiveness.

Wheat: Modest gains Tuesday capped a second straight double-digit weekly advance. Chicago spreads were soft, KC calendars flat to firm, Minneapolis a touch weaker. WU implied vol ticked up to 29.27 percent from 29.09pc.

Wheat: Modest gains Tuesday capped a second straight double-digit weekly advance. Chicago spreads were soft, KC calendars flat to firm, Minneapolis a touch weaker. WU implied vol ticked up to 29.27 percent from 29.09pc.

Matif Sep added €0.50/t with Russian cash near US$227.50/t fob.

China chatter, EU heat, higher crude and whippy midday model runs did the work.

BBG’s Friday all-wheat carryout survey sits at 718 mil bu, down from 744 in June, with the 26 mil bu cut expected out of winter wheat production; SRW carryout is a snug 91 mil.

The heavier the EU’s corn losses, the more wheat gets fed — and the heat driving those losses is expected to persist another 7-10 days with below-average rain.

Export data reinforced the tightening skew: EU soft wheat exports rose 8pc to 23.4 mil tons for the season just ended, led by Morocco, Nigeria and Saudi Arabia, while imports fell 46pc.

Ukraine’s early grain harvest is on schedule — 251,400 ha in, 1.02 mil tons threshed toward a targeted 60 mil ton crop — even as topsoil moisture has fallen sharply nationwide. The drought risk sits with the yet-to-be-sown late crop, corn and sunflower, 30-40pc of which is now affected, not the wheat and barley already off the field.

If China does come for US wheat, SRW is the contract that benefits — not an ideal year for Beijing to play games in Chicago against a 91 mil bu carryout.

Other grains and oilseeds: Corn opened weak but came to life mid-session when the 11-15 day flipped from temperate to hot — the GFS reversal that had been offsetting the hotter, drier EU model. Friday’s carryout is expected to tighten too: BBG sees 1.899 bil bu, down 61 mil from June, mostly on higher feed and residual use after last week’s lower-than-expected stocks.

The market is short and the grower isn’t selling, which makes getting positioned ahead of Friday harder than usual.

Argentina is the world’s cheapest FOB origin into Asia, though the US remains competitive. Yield chatter runs 180-185 bu, with the BBG survey pegging Friday’s number at 182.9; the longer-range forecast has flipped from hot to average and back to hot within the week.

Beans extended Monday’s rally, SQ up 9.75c and SX up 5.5c, with SMQ up $3.30 and BOQ up 83 points — August crush firmed 6.75c to 256.50.

The anticipated China bean announcement didn’t land, though 105,000 tons of old-crop meal to Colombia was confirmed.

Word of further Chinese bookings — another 5-10 cargoes, 10-20 over two sessions — kept a bid under the market; the balance sheet already carries 25 mil tons of US beans to China this year.

Open interest tied to Monday’s trade rose 46k, reflecting shorts covering and new longs jumping ahead of any confirmed program. Friday’s bean carryout is expected at 332 mil bu, up 22 mil from June’s 310, built on a 350 mil view with a 53 bu yield — plenty of cushion if the yield holds, though this week’s price action suggests nobody’s comfortable betting on it.

Canola extended Monday’s gains on spillover from outside markets and Middle East risk, with November trading above key moving averages and drawing spec buying.

Western Canada flooding is now expected to cost up to 5pc of planted area to abandonment, versus a normal 1pc, though a firmer Canadian dollar capped the advance.

Volume eased to 62,271 contracts from 66,686 Monday. Palm oil added to Monday’s gains on firmer rival edible oils and El Nino-related production risk.

Macro: The US-Iran ceasefire took its most serious hit yet. Washington struck Iranian air defenses and weapons launchers overnight and barred new Iranian oil sales after July 7, retaliating for a fresh round of vessel attacks in the Strait of Hormuz — the heaviest single day of shipping attacks since the June 17 truce.

Iran called both the strikes and the waiver revocation violations of the agreement and has told the UN’s shipping body it holds territorial authority over parts of the strait; UK/France de-mining plans were also set back by the latest attack. Crude reflected the reloaded risk premium.

AUD/USD slid to two-day lows, off 0.39pc to 0.6928 (day high 0.6961), as the Hormuz escalation revived safe-haven demand for the dollar and pushed DXY up 0.26pc to 101.12.

US data added to the case: the NY Fed’s survey showed one-year inflation expectations rising to 3.7pc from 3.5pc, and swaps now price a full Fed hike for 2026.

The RBA, having already hiked three times this year, held a neutral tone in its last minutes but left the door open to another move.

The Dow gave back 0.25pc on the day but is still up 1.16pc on the week, with equities largely shrugging off the geopolitical overhang so far.

Local: In the west of the country bids improved yesterday for both canola and wheat, and were a tick lower on barley.

New crop bids were A$840/t FIS for canola and $805 for GM, wheat $353, and barley $328 FIS Albany.

Overall the demand for both old crop and new crop canola remains robust, and pockets of demand remains for old crop wheat with lower grade Albany trading at $340fis.

HAVE YOUR SAY