Weather:

Weather:

Canada has had a strange old start to their canola season – way too wet and now, in parts, the heat is forecast to bite. Personally, I don’t think I have ever made money trading from the long side due to “too wet” but the extreme of the season has created some questions.

Europe is still hot – Sunday is the peak. Fun fact, normal rainfall from 1st of June to the 1st of Aug is around 125mm depending on which part of the country you are in. So far, ie with 2-and-a-bit weeks to go France is sitting around 35mm. Not an issue for cereals, but definitely will be a feature for corn.

Markets

Pre report bounce – wheat daily moves have been impressive this week – kind of weird given the point in the season. Hard to get excited about wheat specific fundamentals – outside market noise is the driver. Around 35 percent of the major exporters wheat will come from Russia/Ukraine which feels tenuous given recent escalations in the conflict – it feels like we are reaching a point that either there is an agreement/cease fire or there is a major increase in infrastructure damage – which will undoubtedly move markets.

Corn conditions in the US are non-threatening today but the impact through Europe will be significant – not great timing then if you are a Spanish consumer.

Day Ahead – Australia

Canola continues to improve but the risk of a nasty spring has throttled the selling weight to some extent.

With ocean freight markets providing some buffer to softening global wheat markets, export parity is not that far below today’s markets – particularly if you are executing through a non traditional pathway.

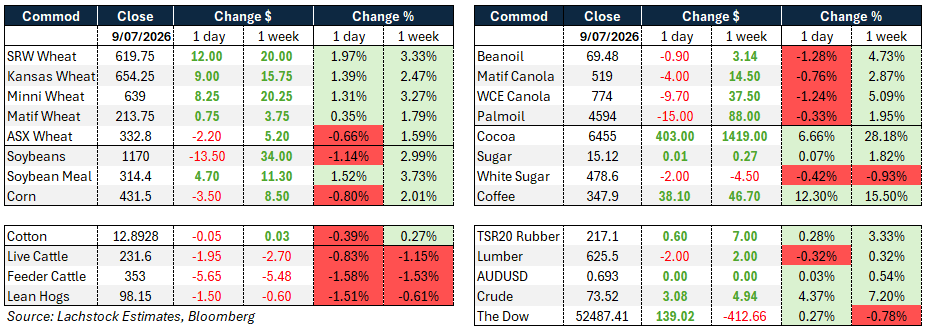

Wheat: Wheat led the complex into WASDE on classic pre-report short covering. WU added 12c, KWU 9c, MWU 8.25c, with spreads bid across Chicago and Minneapolis and implied vol in WU pushing to 29.71pc from 28.48pc

Wheat: Wheat led the complex into WASDE on classic pre-report short covering. WU added 12c, KWU 9c, MWU 8.25c, with spreads bid across Chicago and Minneapolis and implied vol in WU pushing to 29.71pc from 28.48pc

Wednesday. Matif gained just €0.50/t while Russian cash slipped US$0.25/t to $227.25 — a sign US futures were pulling Paris up rather than the Russian diesel shortage driving the move, since origination and FOBs haven’t shown any disruption yet.

The more credible trigger was Friday’s SRW balance sheet: estimates cluster near 91 mil c/o with China accounting for 5 mil bu, though at least one desk is running ending stocks closer to 75 mil on heavier Chinese demand assumptions. The sheet has been tightening since the acreage cuts and today’s move reads as short covering into that risk.

Export sales of 313k bu missed the 425k estimate but broadly matched the pace needed to hit the USDA number, with South Korea and Nigeria the week’s top buyers.

Spring wheat country is turning dry even as Chicago, shortest of the three markets, set the tone.

Argentina raised its 2026/27 harvest forecast 500k tonnes to 20.5 million tonnes (Mt) on expanded plantings, while Taiwan tendered for 98,150 tonnes of US milling wheat across DNS, HRW and soft white for September/October shipment.

Geopolitics stayed in the background but didn’t go away — Kremlin sources describe Putin favouring escalation over negotiation as the war enters its fifth year, with Ukrainian drone strikes on Russian refineries and ports only hardening that resolve.

Other grains and oilseeds: Corn gave back ground into the report, CU down 3.5c and CZ off 4.25c despite Matif maize gaining €0.75/t, as most models turn cooler for the US through mid-July.

Sales disappointed on both old and new crop — 566kt and 402kt against 850kt and 750kt expected — with Japan and Mexico the largest buyers; falling Argentine values are starting to erode US demand.

Soybeans sold off as a bid in meal pulled crush higher and left oil share weaker: SX fell 10.75c, SQ 15.5c, SMQ gained $5.10, and August crush firmed 16.5c to 289.75c.

The China buying story is fading fast — the market already has 25Mt priced into most grids, and Thursday’s daily sales of 136kt to China and 120kt to unknown buyers did little to change that math, even with USTR Greer flagging roughly half a million tonnes bought so far. Old crop sales at 54kt missed 275kt badly, though new crop beat at 408kt versus 325kt expected.

From here the bean market is weather’s to decide, with the key window still weeks away.

Canola pulled back on ICE after Wednesday’s sharp rally, WCE down C$9.70/t to $774 on profit-taking and spillover from weaker Chicago soyoil, softer European rapeseed and Malaysian palm, plus a weaker crude tape.

Technicals stayed constructive regardless — November cleared major resistance Wednesday and the uptrend held through the correction.

Western Canadian weather offered some support, with flood-hit areas now facing forecasts for excessive heat across southern Manitoba and Saskatchewan.

Palm oil eased in Kuala Lumpur as uncertainty over Indonesia’s biodiesel mandate allocation outweighed firmer crude; Jakarta’s 50pc biofuel mandate would lift crude palm oil absorption to a 16.3-17Mt range from 15.2Mt, but the market wants clarity on implementation before pricing it in.

Macro: Crude jumped over 4pc as the Iran conflict escalated again — fresh US strikes aimed at keeping the Strait of Hormuz open drew Iranian retaliation against Kuwait and Bahrain, framed by Washington as a response to Tuesday’s attack on three cargo ships transiting the strait. Trump has now said he considers the interim ceasefire over.

Marine insurers are pulling back on Hormuz cover and premiums are rising, just as the tanker backlog built up during the conflict had finally started clearing.

AUDUSD held flat on the day and remains up half a percent for the week, sitting in a market still digesting China’s fiscal position: provincial governments are within reach of finishing Beijing’s hidden-debt swap, having used 94pc of the 6 trillion yuan allowance by end-June, which should free local officials to refocus on growth rather than debt cleanup, though economists don’t expect fresh stimulus to follow.

The Dow added 0.27pc on the day but is still down 0.78pc for the week, with NATO tensions and the broader Trump-Europe relationship — a trade cutoff with Spain followed within hours by a renewed Article 5 commitment — adding to the noise around risk sentiment.

Local: In the west of the country bids were stronger again yesterday on canola, slightly lower on wheat and unchanged on barley. New crop Albany FIS bids were A$860/t FIS for canola and $825 for GM, wheat $353, and barley $330.

HAVE YOUR SAY