Weather:

Weather:

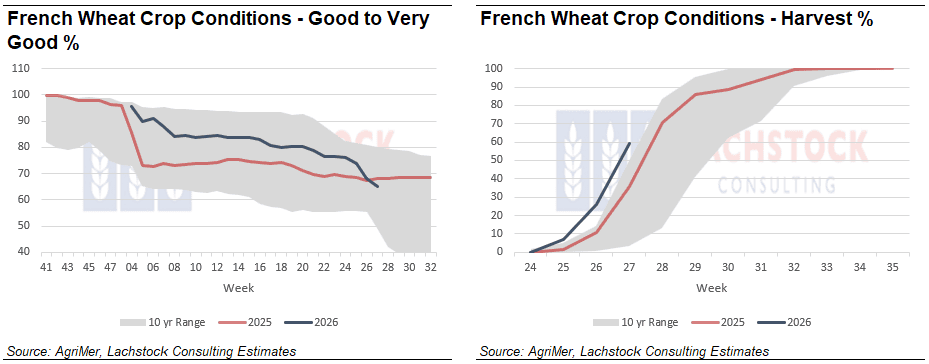

Many areas in France eclipsed the previous record of a week or so ago. Harvest pace is well ahead of normal right through Europe. X is full of farmers indicating that crops are up to 3 weeks early and all crops are ready at once.

Good rains through Madhya Pradesh but Uttar Pradesh is still lagging.

WA has some more rain on the way but east coast looks relatively dry for the next 8 days.

Not crop damaging but Argy is set to see temps 7-10 degrees above normal for the next weeks.

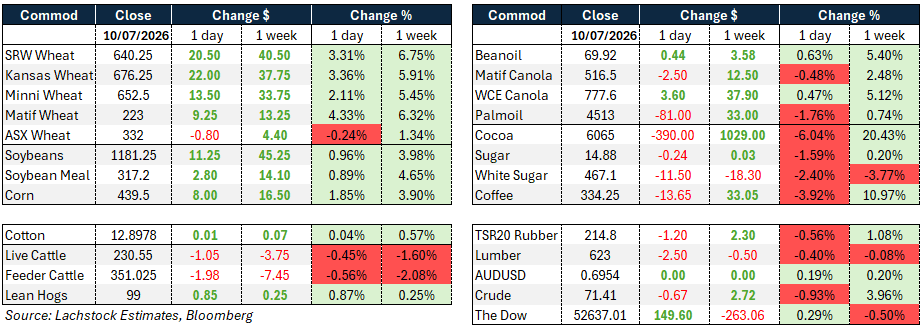

Markets

Post WASDE excitement. It’s increasingly difficult to disentangle market drivers – war risk premium or the smallest US wheat crop since the 1970’s. As we have been banging on about for weeks, 35% of the major exporters available wheat sits in two countries blowing the hell out of one another.

Between Iran and Russia has the market built enough risk premium yet?

Day Ahead – Australia

Markets should be relatively firm today – the risk to the Asian consumer is disruption of the Black sea supply chain – should this continue, Australian old crop would be needed to fill the gap. Argentina did a great job of filling up homes like Vietnam post their massive crop – but northern hemisphere new crop is needed at some point

.

Wheat: Geopolitics did the heavy lifting Friday, not the WASDE.

Wheat: Geopolitics did the heavy lifting Friday, not the WASDE.

Russia’s move to halt vessel traffic through the Kerch Strait and Sea of Azov, a response to Ukrainian strikes on more than 25 tankers and cargo ships in two days, put a bid under wheat well before the report crossed. Contacts estimate the closure could bottle up disruption for weeks to a month, with Russia now prioritizing security over export flow.

WU implied vol jumped to 33.22% from 29.71% Thursday, and a 2,100-lot block of WU 700c calls traded just ahead of the rally.

The USDA layered in supportive fundamentals: US wheat production was cut to 1.536 billion bushels, the smallest crop since 1970, with HRW down to 471 mil bu (471 vs 497 in June, expectations at 481) on both lower harvested area and yield.

SRW production eased on acreage alone, ending stocks a tight 101 mil bu against only 100 mil bu of projected exports, leaving China as the swing factor.

HRS was the surprise, at 436 mil bu versus expectations near 400, though hot northern-plains temps put that figure at risk before harvest.

HRW ending stocks fell to 308 mil bu from 437 a year ago, with exports seen at 210 vs 320, a fair clip given where US values sit against the world. ASX has been lagging the global move, today will be interesting.

Other grains and oilseeds: Corn found support in a friendly WASDE, old-crop stocks trimmed 125 mil bu on higher feed and residual use partly offset by weaker ethanol demand, while new-crop exports rose 50 mil bu to leave a 1.790 billion bushel carryout, well under trade ideas near 1.899 billion.

The EU corn crop was slashed to 53.78 mil tonnes from 57.5, with some regional estimates already below 50, a number worth watching into subsequent reports.

Global stocks fell to 275.26 mil tonnes from 281.22 in June, tighter than the 278.50 expected.

Beans firmed on a similarly snug balance sheet, old-crop carryout unchanged at 310 mil bu against ideas of 332, new-crop at 330 versus 340 in June and estimates of 337, with a 264,000-tonne new-crop China sale announced ahead of the report.

Crush eased slightly as product strength outran the bean move.

Canola caught spillover from the soy complex and saw chart-driven buying return after Thursday’s selloff, with heat forecasts across the Prairies replacing flood stress as the weather concern.

Export pace has slowed sharply, just 52,500 tonnes shipped in the week to July 5, down 79% on the week, leaving crop-year-to-date volume at 8.26 mil tonnes versus 9.15 mil a year ago with a month left to run.

The USDA held new-crop US soybean stocks unchanged at 310 mil bu, slightly below trade guesses for an increase.

Cocoa’s sharp daily reversal, still up more than 20% on the week, stands out as the complex’s most volatile mover.

Macro: Crude gave back ground Friday even as the US launched fresh strikes on Iran and Tehran declared the Strait of Hormuz closed until further notice, a divergence that speaks to the market largely accepting US assurances the waterway remains passable.

US Central Command maintained the strait is open to all vessels, and reports suggest roughly 20 commercial ships transited in coordination with the US military despite the rhetoric.

Iran’s retaliatory strikes hit US allies including Kuwait, Jordan and Qatar, causing only minor damage, while attacks on Iranian energy and port infrastructure continue to escalate the tit-for-tat.

The risk premium is real but crude’s fade suggests traders are pricing continued flow rather than an actual chokepoint closure, at least for now.

Equities held a firm daily tone despite the headlines, though the Dow remains lower on the week.

AUDUSD sat still, with the local unit yet to find a clear driver from either the wheat or Middle East storylines.

Local: In the west of the country on Friday bids eased for canola, and were broadly unchanged on cereals. New crop bids in Albany PZ were $853 FIS for canola and $810 for GM, wheat $354, and barley $329.

Downs wheat actually showed some strength over the week but on very small volume.

According the the MLA, feeder steers finished the week up another 2% to close at 553c/kg – its highest level since 2022.

Mutton and lamb both hit records as well amid the lowest weekly mutton kill since 2020.

HAVE YOUR SAY