Weather:

Weather:

Heat in the US is easing but weather is taking the back seat today.

Markets

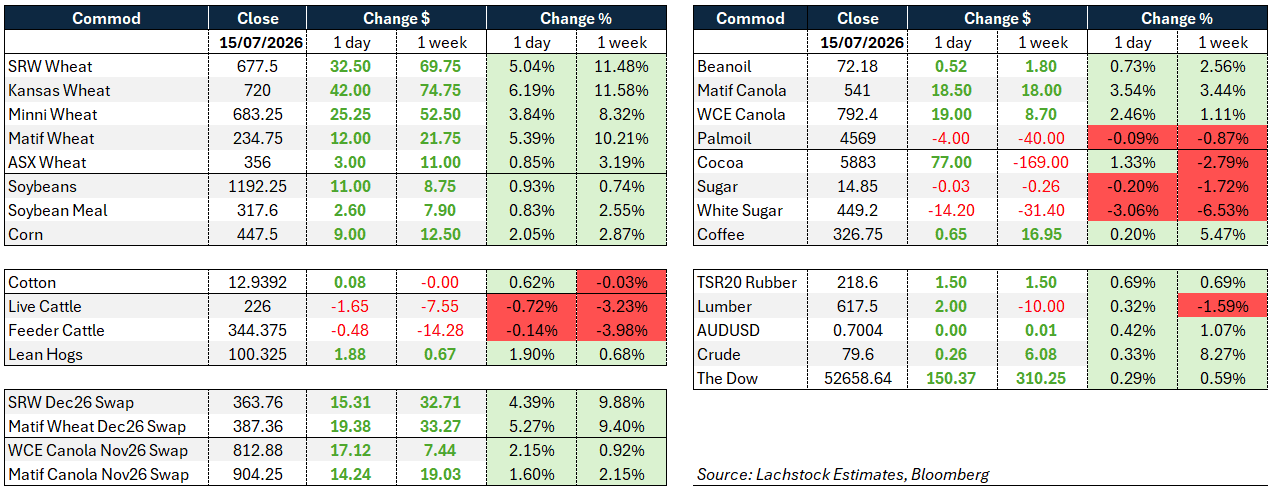

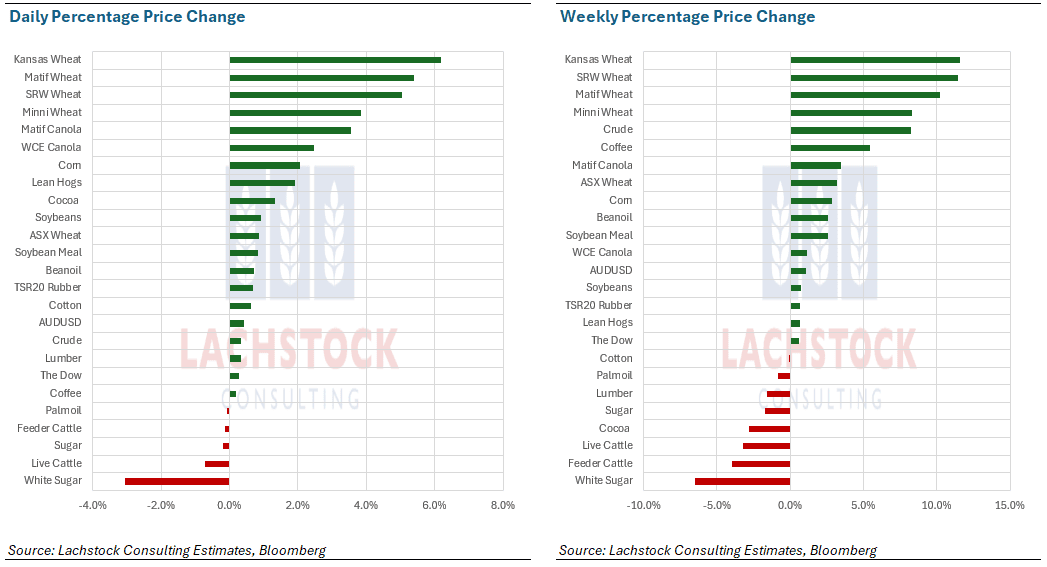

Russia and the Ukraine punched out 8.25 million tonnes wheat exports in July/Aug last year. This, for the moment at least defines the risk in the wheat market. Yes some will bleed out but if the drone strategy continues, the shortfall will build quickly. There is still a niggling feeling of déjà vu here – war premiums seem bullet proof (pun intended) when things are blowing up but, as the history of this conflict has shown, bulls need feeding. Every escalation has felt different, yet every market move has not; maybe this time?

Day Ahead – Australia

Canola back on the bid. Cereals will be interesting for me – what is the Asian consumer thinking today with the Northern Hemisphere supply chain impacted at best, shut off at worst. Everything should catch a bid today.

Wheat: Black Sea supply is unraveling in real time. Ukraine’s drone campaign against Russian shipping has escalated to the point where both sides now appear willing to strike anything in reach, and vessel operators are responding by avoiding the region altogether. Kernel confirmed extensive damage to its Chornomorsk terminal, with roughly 45,000t wheat and 9000t sunflower oil spoiled or destroyed, and Ukrainian sellers are pulling back from local origination as a result.

Wheat: Black Sea supply is unraveling in real time. Ukraine’s drone campaign against Russian shipping has escalated to the point where both sides now appear willing to strike anything in reach, and vessel operators are responding by avoiding the region altogether. Kernel confirmed extensive damage to its Chornomorsk terminal, with roughly 45,000t wheat and 9000t sunflower oil spoiled or destroyed, and Ukrainian sellers are pulling back from local origination as a result.

Kansas wheat locked limit up on the news, and MATIF added the equivalent of US49 cents per bushel. Russia’s own export capacity is caught in the crossfire, with Moscow reportedly pulling vessels from the Azov to regroup. Adding to the bullish case, France cut its 2026 soft wheat estimate to 32Mt, down 4pc on the year and below the five-year average, as a run of heatwaves offset a modest gain in planted area.

With a 90Mt Russian crop now stranded behind a closed shipping lane, the market has little incentive to find a seasonal low, and until either side shows restraint the path of least resistance stays higher.

Other grains and oilseeds: Corn caught execution premium alongside wheat, with Ukraine’s disrupted export flows a direct threat to Europe’s feed grain supply during a summer already marked by drought. A river-and-rail workaround exists but can’t move the volumes required to plug the gap, which raises the burden on the US crop to deliver. A national yield below 181-182 bushels leaves little room for the extra 10Mt demand this situation could generate.

The US Corn Belt heat is expected to break this weekend, though the next wave shifts toward the Plains and western belt while sparing the east, and Wednesday’s EU model added rain for US corn next week. Higher wheat and corn together tighten the math for livestock feeders, since wheat can only substitute so far into rations before cost undermines the swap.

Soybeans lagged the rally before catching a bid on fresh Chinese cargo purchases and a much larger than expected June crush; NOPA’s 214.3M bushels beat estimates comfortably, and the resulting bean oil stock draw, at just 1.5 billion pounds, was a record for the month. Export sales tomorrow are expected to reflect the Chinese buying, with soybean sales forecast as high as 2Mt against a market accustomed to closer to 300,000t.

Canola continues to build its own case: Ventum’s David Derwin sees the November WCE contract testing C$805/t, pulled by seasonal strength, spillover support from crude and Chicago soyoil, and export demand that could still reach Agriculture Canada’s 8.4Mt target despite lingering drag from China’s tariffs. The bigger unknown is area: wet Prairie conditions may cut planted-to-harvested area by as much as 5pc, well above the usual 1pc loss, even as yield potential still looks sound.

Palm oil sat rangebound on the absence of fresh catalysts.

Macro: Crude’s weekly gain reflects Middle East risk stacking on top of the Black Sea disruption.

Iran’s Revolutionary Guard has threatened to shut every export corridor that benefits the US and its allies, following its earlier closure of the Strait of Hormuz and Washington’s naval blockade response, and the rhetoric on both sides continues to escalate.

China’s economy grew at its slowest pace in three years last quarter, missing forecasts as weak household consumption offset resilient manufacturing and exports, a result that raises fresh doubts about the durability of its growth model even as it steps in for physical grain purchases.

Washington is also expected to impose a 25% tariff on thousands of Brazilian imports after months of stalled negotiations, a move that would touch roughly US$15 billion in annual trade.

Equities shrugged off the mounting geopolitical noise, with the Dow adding to its weekly gain as inflation data outweighed concerns elsewhere in markets .

Local: In the west of the country bids backed off across all commodities yesterday. New-crop bids in Albany PZ were A$865/t FIS for canola and $832 for GM, wheat $358, and barley $328. Today should see 2026-27 bids test the recent highs again on canola, and look for wheat bids to head towards the $370s. East coast flow has been dominated by canola, both old and new. With global cereal markets firming it will be interesting to see if the southern market can shake the grower, despite the El Niño risk.

HAVE YOUR SAY