Weather:

Weather:

The recent run of hot weather in EU is now starting to filter into the production estimates, with Germany the latest to cut production of cereals.

WA the only place really getting rain in the next week to 8 days.

Markets

Will this consolidate or will the risk premium erode. We have seen this movie a hundred times and, while there is plenty of reasons that this time is worse than all the others, markets are guarded and waiting for the next escalation to trade around.

The one thing that wont go away, even if FOB markets bleed back, is the freight risk premium. The other thing that will linger is the performance doubt global buyers will have.

Day Ahead – Australia

Take a breather – actually, wait to see if any Asian demand arrives.

The Aussie market will oscillate from war news to El Niño news. I feel flat today.

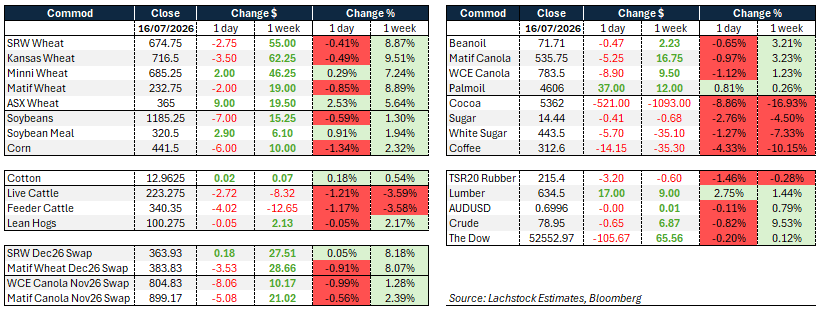

Wheat: Two very different sessions again. Overnight WU rallied hard, within sight of 700 at 698.25, a spike traders put down to someone in a rush to cover a short and triggering stops along the way, hours before Matif opened. By daylight the market had faded to the low 680s and only made it back to 684.50 intraday, and CBOT wheat touched a two-year high, up as much as 3.1 percent, before erasing the move once USDA showed weekly export sales of just 235,000t, the lowest since May and well short of the 425,000 expected against a needed pace of around 315,000.

Wheat: Two very different sessions again. Overnight WU rallied hard, within sight of 700 at 698.25, a spike traders put down to someone in a rush to cover a short and triggering stops along the way, hours before Matif opened. By daylight the market had faded to the low 680s and only made it back to 684.50 intraday, and CBOT wheat touched a two-year high, up as much as 3.1 percent, before erasing the move once USDA showed weekly export sales of just 235,000t, the lowest since May and well short of the 425,000 expected against a needed pace of around 315,000.

StoneX’s Arlan Suderman pointed to the sales miss landing just ahead of the morning pause as the trigger, while Hightower’s Randy Place put some of it down to profit-taking and position-squaring into the weekend after an aggressive week, with Ukraine-Russia shipping still the dominant driver.

Turkey, Morocco and Egypt are all showing muted import interest, which is helping cap the market for now, though that calm won’t last if it persists. Egypt’s own June imports fell to an all-time monthly low of 405,000t after a front-loaded procurement campaign earlier in the year, and Rouen loadings slipped to 103,386t from 173,481 the prior week.

The Black Sea situation continues to deteriorate. Ukrainian forces have struck over 100 Russia-linked vessels in the Sea of Azov plus targets in the Black Sea, while Russia has intensified strikes on Chornomorsk, Odesa and Pivdennyi, with Chornomorsk’s grain intake sharply reduced. Azov/Kerch Strait trade is described as virtually shut, and Ukraine has already lost roughly a third of its Black Sea export capacity per the Ukrainian Agrarian Council. CVB is picking up the slack with FOB offers around 260-270.

Rabobank’s Vitor Pistoia argued the reaction should stay more contained than 2022 since the disruption this time is hitting exports rather than coinciding with planting, while CRM’s Mike Verdin flagged broader food inflation risk if disruption spreads into fertilizer.

Russian cash slipped $1 to $237, Matif Sep fell €2, and AgResource called wheat technically overbought after the run-up, a view echoed in today’s pullback.

Weather adds another layer: US spring wheat is showing heat stress in the northern plains, France’s wheat yields are running 3pc below the five-year average nationally with 10-20pc shortfalls in central regions, and Germany’s DRV cut its winter wheat estimate to 19.9Mt from 22.6Mt last year, citing severe heat-driven premature ripening; barley eased just 1.8pc to 9.34Mt, largely unaffected, while rapeseed is meeting expectations in the west but falling short in the east.

Other grains and oilseeds: Corn had a poor technical session, CZ breaching its 100-day average, testing the 200-day, then settling near session lows right at the 50-day.

Export sales were weak across both old crop (315,000 vs 800,000 expected) and new crop (311,000 vs 700,000 expected), leaving Argentina in command of the world market on price.

Forecasts show moderating Midwest temperatures next week, keeping high temps mostly below 95°F and easing stress on reproductive corn and soybeans, though precipitation remains below average in the 8-14 day outlook.

Strategie Grains trimmed its EU corn estimate to 50.2Mt versus USDA’s 53.8m.

Beans sold off on the improved weather outlook while crush strength offset it, meal rallying $4.00 and bean oil down 49 points, pushing August crush up 10.5c to 312.

There’s chatter China is again asking for offers, a reminder that hitting 25Mt of purchases requires frequent engagement.

Brazilian bean and meal lineups remain larger year-on-year and the Argentine program is nearing completion; domestically, 107 certs were cancelled and cash stayed firm.

New crop sales beat expectations solidly (beans 1.77Mt vs 1.3Mt expected, meal 51,000t vs an anticipated 150,000t miss), though old crop bean and meal sales missed, and bean oil was soft on both fronts.

Canola gave back a good chunk of Wednesday’s gains as comparable oils stepped back, with weaker Malaysian palm oil and European rapeseed spilling over and crude reversing to modest losses; soymeal strength only partly offset the drag.

One analyst called it a breather in the broader upswing, with November pulling within C$22 of its 50-day moving average.

Saskatchewan’s canola crop is rated 76pc good-to-excellent, the loonie was flat at 71.16 US cents, and volume eased to 47,471 contracts from 50,122 Wednesday.

Palm oil itself slipped on expectations of stronger Malaysian output this month, with Pelindung Bestari’s Paramalingam Supramaniam noting seasonally firmer harvests building on June’s recovery.

Macro: US retail sales rose 0.2pc m/m in June, in line with consensus, with the softer headline driven by lower gasoline spending as prices fell; ex-gasoline sales rose a firmer 0.7pc, following 0.9pc in May, with 7 of 13 categories higher.

That extends a run of resilience: ex-gas sales have averaged 0.7pc m/m since February versus just 0.1pc in the five months prior, a pattern likely underpinned by tax rebates and a stabilising labour market.

In Europe, the euro area’s seasonally adjusted trade balance swung to a rare €5bn deficit in May, partly an energy shock but increasingly a structural story, with the ex-energy surplus narrowing steadily since early 2024 as the imbalance with China widens; weak Chinese domestic demand tied to the property downturn is cutting exports to China even as Chinese manufacturing overcapacity and eroding EU cost competitiveness push more imports in the other direction.

Weaker US export demand from tariffs has so far been offset by growth in exports to non-euro European economies, but the China gap remains a live policy concern.

Geopolitically, the US intensified strikes on Iran overnight, hitting an oil tanker near the country’s main export terminal as Strait of Hormuz traffic slumped; Iran retaliated against American bases in Kuwait and Jordan, with Trump warning of further escalation.

Washington’s 25pc tariff on Brazil renews friction with Lula’s government ahead of elections, though coffee, beef and certain ethanol products are exempt from the new duties, unlike ethanol itself, which remains subject to them.

Elsewhere, CME’s beef trim futures debut Monday, and the AFBF is lobbying Congress for broader relief after projecting 2027 per-acre losses climbing further across corn, soybeans and wheat.

Local: Bids yesterday were stronger across all commodities in the west of the country, with a significant lift seen in both canola & wheat. New crop bids in Albany PZ were A$880/t FIS for canola and $845 for GM, wheat $371, and barley $330. Growers have been reasonably active over past weeks marketing mostly canola and some barley.

East coast was all about canola yesterday, both old and new as depot prices for new crop non-GM eclipsed the $800 mark.

HAVE YOUR SAY