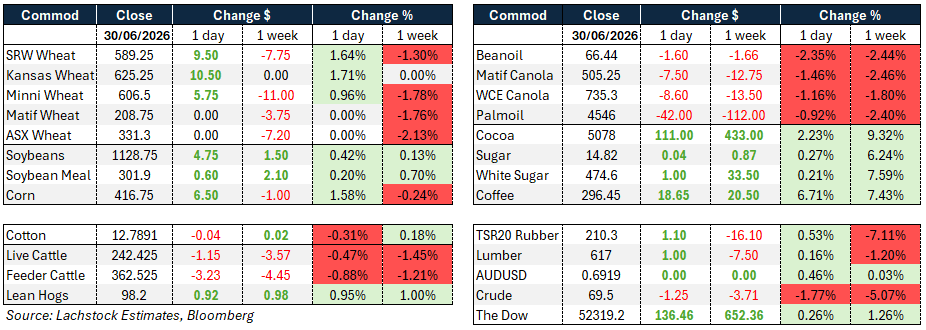

Weather:

Weather:

Not much difference day on day – USDA corp conditions tell you we have had some challenging seasonals in the US but thats nothing new.

EU/Black Sea/India all same same.

Markets

Are we calling a low in US wheat futures? We rallied Chicago US$1.60/bu from the start of the year as seasonal conditions deteriorated and crop conditions suffered. Same fundamentals and we broke the market US$1.26/bu on ideas you simply cut exports off and solve supply with demand reductions. Then, last night the USDA just reminds the market that things are still tight. In the meantime, the CFTC shows the spec loves selling wheat.

Day Ahead – Australia

Belting down in parts of SA at the moment with rainfall prospects looking good for the east coast.

USDA report behind us and maybe the seed is sown that the international situation is mixed as opposed to being just being flat out bearish.

July 1 selling anyone?.

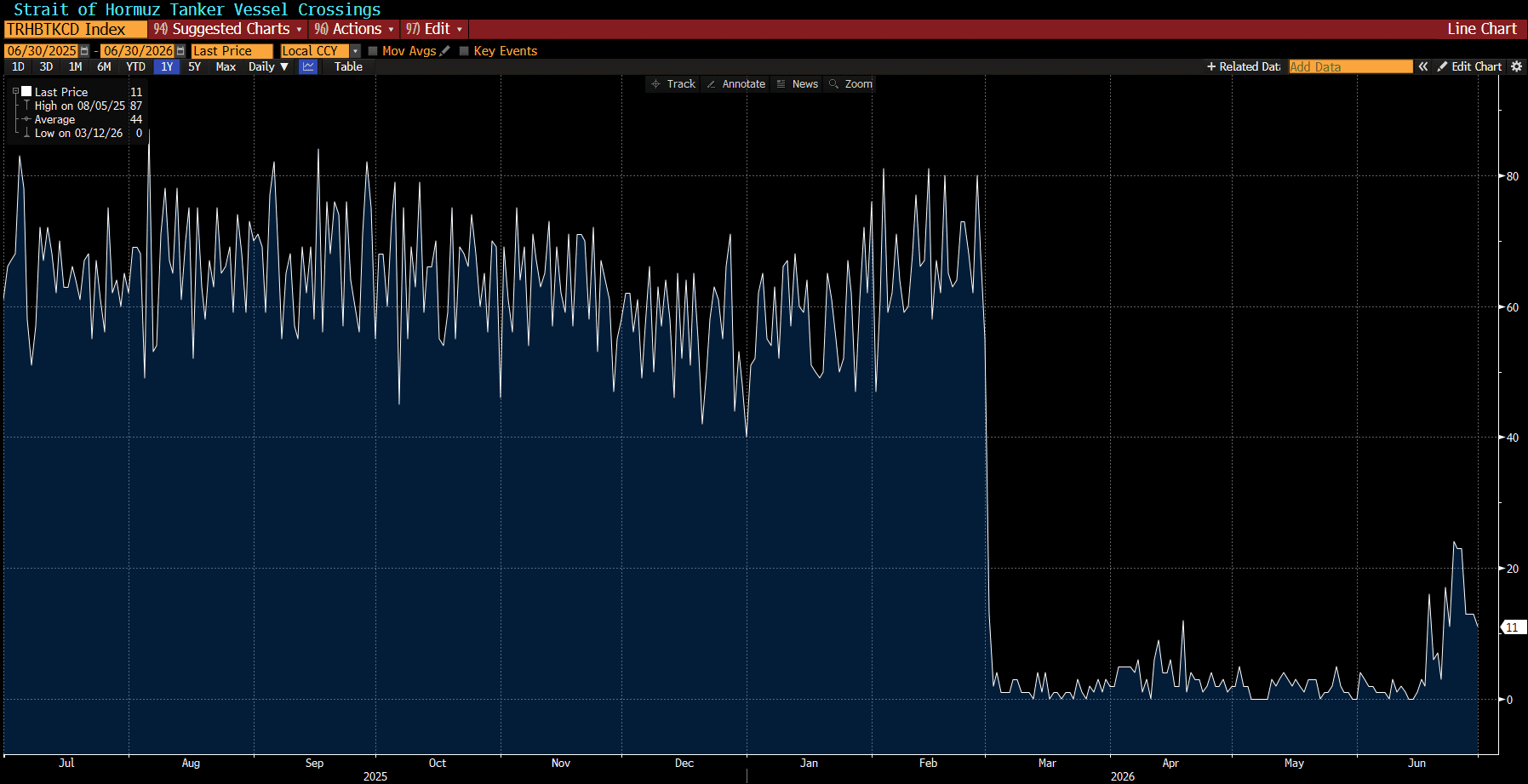

Source: Bloomberg. Strait of Hormuz Tanker Crossings

Wheat: Wheat led on USDA day. WU added 9.5c, KWU 10.5c, MWU 5.75c as Acreage and Grain Stocks came in friendly on both counts.

Total wheat acres fell to a record low 42.7 mil from 43.8, undershooting the average guess, with winter wheat wearing the cut — around 300k SRW acres and 600k HRW gone.

That drops HRW production to 483 from 497 and SRW to 285 from 300 on unchanged June yields, pushing most SRW carryout estimates under 100 mil.

Spring wheat held at 9.4 mil, roughly matching expectations. Stocks printed 920 mil against guesses clustered near 930-935. Chicago spreads firmed into the close, KC softened slightly, Minny was mixed, and WU implied vol edged up to 25.66 percent from 25.55pc.

Matif September eased €0.50/t while Russian cash slipped under $229 after a $2.75 drop Monday. Canada mirrored the acreage shift, rotating out of wheat into canola.

Nigeria picked up 100k HRS on a rare daily sale, taking advantage of Minny’s earlier weakness.

Winter crop condition ratings are a big part of the story — only 26% good/excellent, down sharply from 48% a year ago — which is why the market treated tight acres on a struggling crop as the most bullish element of the report.

None of it changes the bigger picture though: a 90-mil-plus Russian crop still puts a lid on Chicago, world demand for US wheat remains thin, and China stays an open question long after the Trump-Xi meeting. A Chicago short is harder to justify with carryout now near 91 mil.

Other grains and oilseeds: Corn had been trading a big-acreage story into the report, but NASS held acres at 95.3 mil, close to guesses. The real mover was stocks — a bigger feed number took the figure to 5.295 bil versus roughly 5.41 bil expected, opening the door to 150-200 mil coming off the carryout once export pace is layered in.

December futures popped on the release before fading as good growing weather and solid yield expectations capped the follow-through; most of the Belt got adequate rain in June, though July is opening drier.

With the report now behind it, China demand still unresolved, EU drought stress building, and heat advisories across the US, corn has a shot at bouncing into the holiday.

Soybeans were quieter — acres at 85.4 mil versus 85.2 expected, stocks a touch above forecast at 920 mil versus roughly 931 mil.

April bean oil use for biofuel came in soft, with food and other industrial use picking up the slack.

SQ added 5c, BOQ dropped 193 points, and crush eased 26c to 280.50.

Nothing today changes the core debate in beans — Chinese demand and US production risk heading into the critical oilseed weather stretch.

Canola stayed under pressure on both sides of the Atlantic, consistent with the acreage rotation showing up in Canada’s numbers.

Macro: Crude softened as Iran hardened its position on Hormuz ahead of the next round of Doha talks, with Tehran pushing for a joint oversight arrangement with Oman and signaling it will act alone if that doesn’t happen.

A fee or toll regime on Hormuz transit remains a live risk once the current waiver window closes, and that overhang is likely doing more to weigh on WTI than any single day’s headline.

Traffic through the strait has continued despite recent attacks, still below pre-war norms, and Washington has kept expectations for a breakthrough in Doha low.

Equities and the AUD didn’t show much concern — the Dow added to a strong week and the AUD ticked higher, holding near the lower end of its recent range.

Local: In the west of the country bids were stronger with canola $805 and new crop $845, wheat was $347 and $347, barley $330 and $333 FIS Albany.

Through the east bids were up slightly with canola $755 and new crop $798, wheat was $324 and $345, barley $310 and $313 track Geelong.

New year, new sales? It will be interesting to see whether the new financial year brings any additional grower liquidity, although at current price levels many producers remain reluctant sellers.

Canola values have recovered following the recent pullback alongside crude oil. Structurally, the market remains well supported by strong global biofuel demand. While harvest pressure from the northern hemisphere is likely to weigh on values over the next month, the longer-term outlook remains constructive.

HAVE YOUR SAY