Weather:

Weather:

Australian conditions are broadly favourable — scattered showers and near-normal temps across WA, southern SA/Vic/NSW seeing above-normal warmth with isolated showers. Globally, harvest weather is cooperating in the Black Sea and Europe, US Plains and Canadian Prairies are supportive, while Argentina remains dry and could use rain.

Markets

Markets continued to digest the USDA report which, against the average guess, tightened the US wheat balance sheet. The key theme for me is the world can probably do without a meaningful US export program – a fact not lost on the market given recent price action. However, a big percentage of the major exporters available export tonnage sits in the Black Sea – and they are still at war – baffling.

D4 RINs rallied yesterday, Indo moves to D50 and the world waits for China buying. Veg oils feel supported.

Day Ahead – Australia

Rain filled in the blanks. Amazing falls through the east coast of Australia with some suggesting they could do with a few dry weeks – amazing.

Given the falls over the last few days and the calendar rolling over to the next financial year it will be interesting if we see old crop liquidity freeing up. Slightly softer for me.

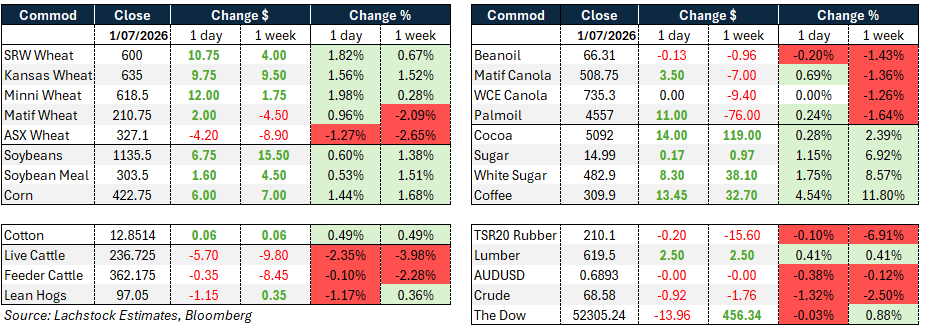

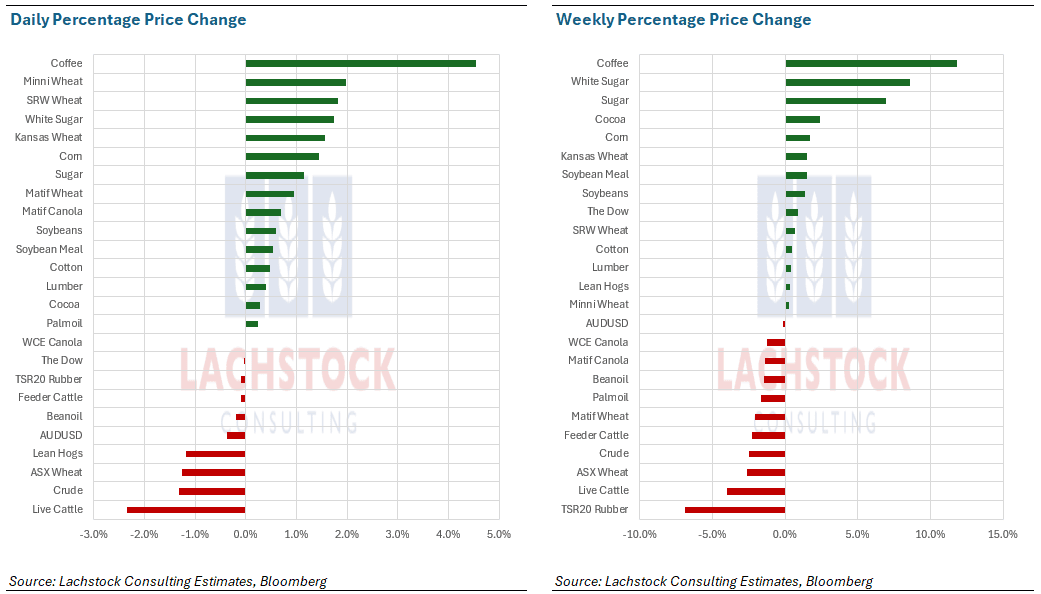

Wheat: Wheat rallied higher across the board, Chicago leading with vol pushing out to 26.2 percent as spreads firmed.

Wheat: Wheat rallied higher across the board, Chicago leading with vol pushing out to 26.2 percent as spreads firmed.

The driver remains a shrinking US balance sheet — another 900k winter wheat acres gone in Tuesday’s report, HRW carry now a few clicks under 300 versus 450 a year ago, SRW carryout pinned under 100.

None of it is new, but two straight reports have cut hard into US area and the market is short everywhere, Chicago most of all. Heat across the globe into a long weekend added fuel.

Thursday’s export sales should print near 450kt, well clear of the 315kt pace needed. September futures cleared US$6/bu, up roughly 2pc, though desks note the rally still lacks a fresh bullish catalyst beyond what’s already known — strong yield potential in the forecast is the counterweight.

South Korea split a wheat tender between Australian and US origin; Ukraine’s June grain and oilseed exports slipped to 3.76 million tonnes (Mt) from 4.0Mt in May.

The bigger tension is carry-in versus carry-out. A sub-500 HRW crop barely squares with October expectations, and SRW keeps losing acres too — arguably the tighter risk is the 91-bushel SRW carryout rather than the 297 HRW figure, since Chicago doesn’t have the depth to service Chinese demand if it materialises.

A strong HRW carry-in is the only thing keeping the balance sheet workable. Add thinner acres across the US and Canada and a late El Niño risk in Australia, and the global cushion looks thinner than it did a year ago.

Other grains and oilseeds: Corn finally bounced, up 6c-plus, on heat, the acreage cut and unverified but market-moving chatter of Chinese corn and bean buying for Sep/Oct. Beans followed, meal firmed, but bean oil and crush both eased.

The real driver is optionality on a Trump/Xi outcome — talk of 12-17Mt of potential Chinese bean purchases is circulating, but it’s contingent on politics lining up rather than anything confirmed.

USDA’s own numbers showed US soybean acres up 5pc on the year to 85.4 million.

Indonesia’s new 50pc palm-based biodiesel mandate kicked in this week, tightening the regional vegoil call even as Malaysian palm firmed on stronger soyoil and a weaker ringgit.

Canola pared early losses in Winnipeg, spot month actually finishing higher while new crop slipped on pressure from soyoil, rapeseed, palm and crude. StatsCan’s acreage report was the domestic story — a record 23.44 million canola acres for 2026-27, above the 2017 high and well up on last year’s 21.62 million — alongside May crush of 1.04Mt versus 831kt a year earlier.

November clawed back above its 100-day moving average by the close; the loonie was flat.

Macro: ECB rhetoric is softening. Lagarde now sees inflation and growth risks as more balanced, and even Wunsch — a prior hawk — thinks one more hike could be sufficient. The data backs the shift: June euro area headline inflation fell to 2.8pc from 3.2pc, well under the 3.0pc consensus, core dropped to 2.4pc from 2.6pc, and services eased to 3.2pc. Both core and services are now close to pre-conflict levels, with no sign of the broadening the hawks were waiting on. Weak growth and a softening labour market leave little case for renewed persistence.

Local: Bids were softer through the west of the country yesterday with canola A$790 and $830 for new crop, wheat was $331 and $348, barley $326 and $331 FIS Albany.

Similar story in the east with canola back to $750 and new crop $785, wheat was $324 and $345, barley $309 and $313 track Geelong.

Some handy falls over the last 48 hours, with much of SA and Victoria now bordering on too wet. Importantly, some of the drier pockets through southern NSW were able to fill in, with the Griffith–Rankins Springs region receiving 30–50mm right where it was needed.

HAVE YOUR SAY