Weather: Kansas missed out again – nothing new here but there was hope leading into the weekend.

Good falls through southern Australia – 1-2 inches across SA, Vic and southern NSW.

Not convincing but some weather forecasts have built in up to an inch in NNSW/Southern Qld.

Markets

Markets feel like they are exhausted – wheat fell into the weekend after showing signs that US futures have rallied enough. Delivery against futures is generally the canary in the coal mine for wheat rallies.

Day Ahead – Australia

The local market will unpack the rain fallen and the rain forecast. The timing of this rain couldn’t have been better with the heat we have recently seen. Warm dirt, rainfall, lets go.

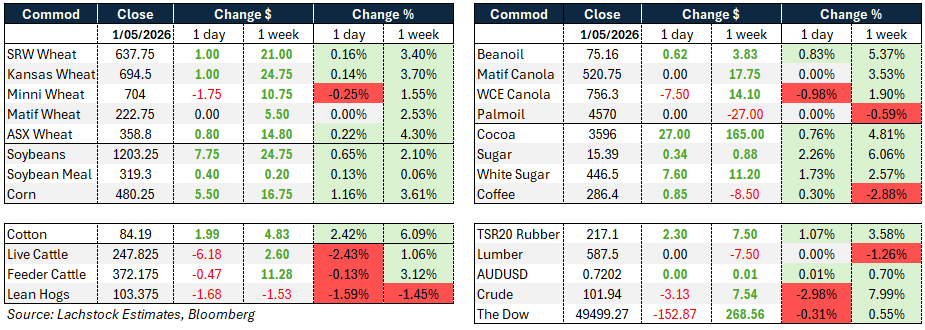

Global wheat: Chicago July +1c, Kansas +1c, Matif closed.

Global wheat: Chicago July +1c, Kansas +1c, Matif closed.

Wheat markets were narrowly mixed and largely directionless through the session, with world markets closed for May Day keeping participation light.

Chicago July and Kansas City July each firmed a cent while Minneapolis slipped 1.75c. Spreads were firm in Chicago, mixed in KC and weak along the Minny curve, with implied vol in Chicago wheat edging slightly higher to 33.30 percent.

The market struggled to find a catalyst in either direction, with support from firm row crops offset by a lack of fresh bullish news.

Recent rains across Colorado and western Kansas disappointed, doing little to alleviate ongoing dryness concerns in Hard Red Winter wheat country.

The market remains in a wait-and-see mode ahead of a busy tour calendar, with the WQC event on May 11 the highlight.

Grower and analyst sentiment is that US wheat has likely overshot to the upside if Kansas can salvage its crop without further complications elsewhere, with the broader narrative now framing as a balancing act between supply loss and demand destruction at elevated price levels.

Deliveries were 312 in Chicago and 245 in Kansas City.

On the international front French soft wheat conditions fell 2 points to 81pc good-to-excellent, though that still compares favourably with 74pc a year ago, and the EU Commission lifted its soft wheat production estimate to 127.3 million tonnes (Mt) from 125.9Mt.

Other grains and oilseeds: Corn +5.5c, Soybeans +7.75c, WCE Canola -7.50c.

Corn was the standout performer, with the December contract scaling 500 cents for the first time before settling up 4.5c at 498.75.

A USDA flash sale of 148,240t corn to unknown destinations added to the bullish tone, reinforcing hopes of strong global demand.

Ethanol demand also surprised to the upside with USDA reporting 474.4 million bushels used in March against expectations of 462.2 million.

Ongoing safrinha crop concerns in Brazil, excessive rainfall in parts of Argentina’s Santa Fe province, optimism around a Trump-Xi meeting providing a potential demand catalyst, and cold Midwest forecasts raising germination concerns all contributed to the supportive tone.

Fund money continued to flow to the long side of grains at the start of the new month, with seasonal price trends and weather concerns seen as keeping that momentum intact near term, though the size of net long positions leaves the complex exposed to a sharp reversal.

The soybean complex was unanimously higher with July beans gaining 7.75c and breaking back above $12 a bushel for the first time since March, a level described as psychological resistance.

Soyoil rallied 62 points supported by higher crude, meal added 40 cents, and July crush settled unchanged at 326.

The overriding driver for old crop beans remains the prospective Trump-Xi meeting in a fortnight, with cancellation or delay likely to see a meaningful selloff.

The USDA crush figure came in below expectations at 227.4 million bushels against 231.4 expected.

Argentine harvest rain chatter provided some background support.

ICE canola pulled back, with July settling down C$7.50 at 756.30 as speculative profit-taking weighed alongside crude oil weakness and a seven-week high in the Canadian dollar. Despite the session’s losses, crush margins remain historically wide at around C$350 per tonne over July futures, roughly three times year-ago levels.

Canadian canola exports for the week ended April 28 came in at 194,000t, up 40pc week-on-week, though crop year-to-date exports of 6.2Mt remain well behind the 7.7Mt shipped at the same point last year.

Macro: AUD unchanged, Dow -152.87, Crude -3.13.

The macro backdrop was shaped by ongoing developments around the Strait of Hormuz and the broader US-Iran-China dynamic. President Trump announced “Project Freedom,” a US military-supported initiative to begin guiding neutral ships trapped in the Persian Gulf through the Strait of Hormuz from Monday, using guided-missile destroyers, aircraft and drones. Trump indicated US-Iran discussions are ongoing and described them as positive, though he expressed doubt that Iran’s latest 14-point peace proposal goes far enough, and has not ruled out military strikes on nuclear facilities.

Crude oil fell around 3pc on the session, with some pressure from cautious optimism around a potential Iran deal, though the underlying fear of a major escalation and a second significant inflationary shock remains very much in play.

The Strait of Hormuz remains closed to normal commercial traffic, with hundreds of tankers, bulk carriers and cargo ships still stranded in the Gulf and regional oil production curtailed due to storage constraints.

Compounding the geopolitical picture, China instructed domestic companies to ignore US sanctions on five Chinese refiners linked to Iranian oil trade, deploying a blocking statute for the first time since its introduction in 2021. The move allows affected refineries to seek compensation through Chinese courts against any entity that complies with the US sanctions, and analysts from Eurasia Group noted it signals Beijing is taking a more assertive posture on countering US sanctions ahead of the anticipated Trump-Xi summit.

The Dow closed down 152 points.

The AUD was effectively unchanged on the day, though the Canadian dollar hit seven-week highs against the USD, relevant context for canola trade flows.

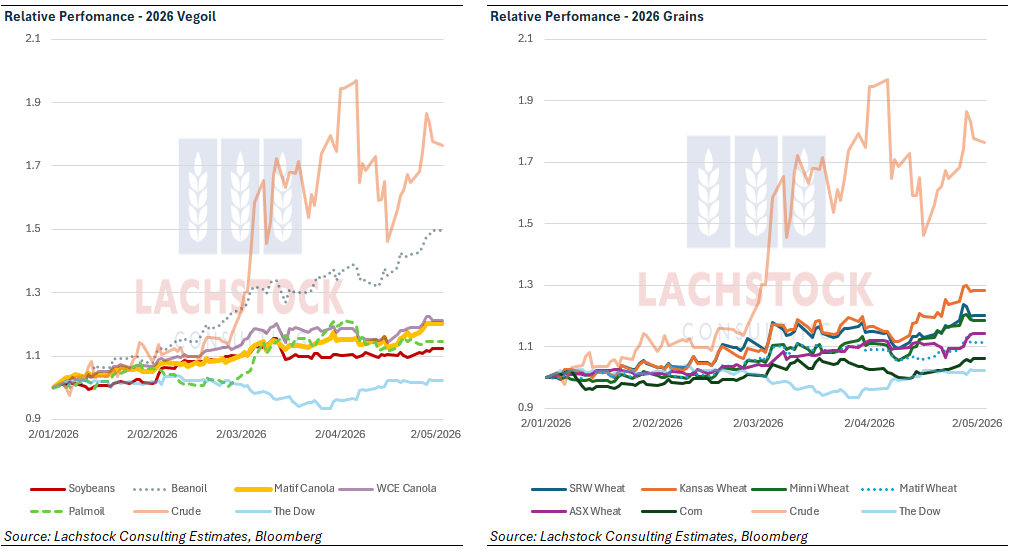

The latest CFTC COT data showed net long positions increased across the complex with the exception of soybeans, with bean oil and Minneapolis wheat both sitting at record long levels.

Local: WA bids were steady to slightly softer, with canola A$800/t current season and $844 new crop, wheat $345 and $363, and barley $350 and $338 FIS Albany.

In the east, canola was $785 current season and $825 new crop, wheat $345 and $377, and barley $318 and $332 track Geelong.

Some very handy falls came through SA, Vic and SNSW over the weekend, with 15–50mm across large parts of the cropping regions in those states.

It will be interesting to see what liquidity does off the back of the rain, with old crop wheat well bid through Vic last week and some old crop length already tipped out, although estimates still have around 40pc of Victorian wheat yet to be marketed.

HAVE YOUR SAY