Weather: Some more chatter around planting delays through the spring wheat areas of Russia – not sure I’m overly concerned given how good the rest of the country looks.

Weather: Some more chatter around planting delays through the spring wheat areas of Russia – not sure I’m overly concerned given how good the rest of the country looks.

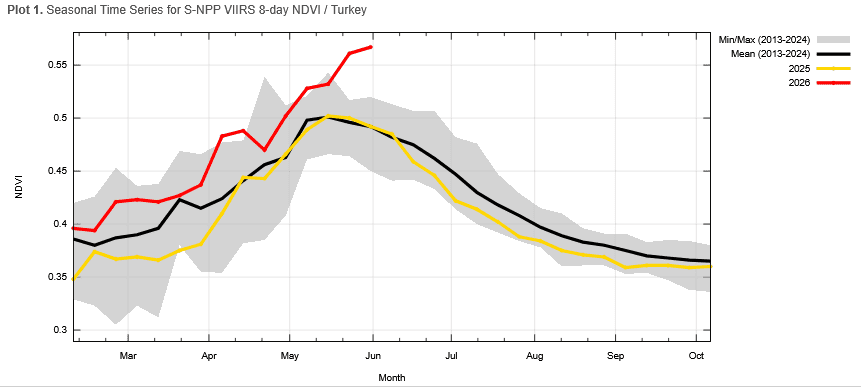

Turkey is having a cracking season and, while NDVI can be a little missleading without context, Turkey is off the chart.

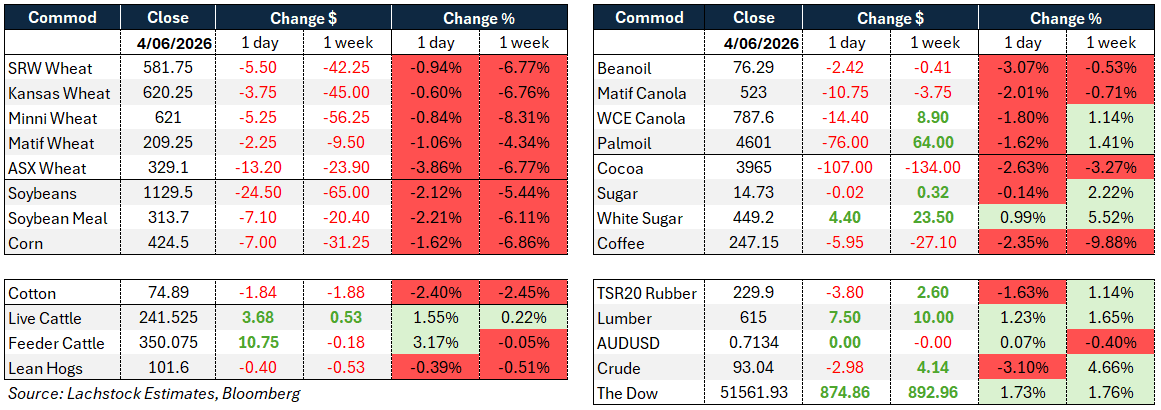

Markets

Wheat loves taking a beating – seems to enjoy it. US futures markets were too cheap given conditions throughout the HRW belt, so things rallied hard, then the market decided we had rationed enough demand and markets had done what they are designed to do. Now, we are back to where we started – literally. July wheat settled at 580 usc/bu, exactly where the rally started. Funny that.

Iran/Donald market influence is fading. Don’s timelines are not even close to a reality – ceasefires are good as long as that means you can keep bombing and negotiations seem further away, not closer. The kicker could potentially be the US Senate trimming Don’s wings but I can’t help but think he will find a way around that.

Day Ahead – Australia

Canola down, cereals sideways. The story in canola is not a simple one. The influence of the US Renewable Fuel Standards on the global veg oil markets cant be understated. This has particular relevance to diesel given the mandate jumps but the structural shift is the pending reduction of foreign feedstocks into the bio pool. So while crop fundamentals matter – there is far more at play.

Source: USDA NASA – NDVI, Turkey

Global wheat: Wheat markets endured another soft session, with Chicago July off US5.50c/bu, Kansas slipping 3.75 cents, and MATIF September easing €1.50/t.

An early attempt at independent strength proved fleeting, quickly overwhelmed by weakness in row crops and a 3pc drop in crude following news of an Israel-Lebanon ceasefire.

Export sales for the week were a significant miss at 196,300t against expectations of around 375,000t, with the bulk of announced sales representing rollovers from old to new crop.

South Korea was the week’s largest buyer of US wheat.

Tunisia tendered for 75,000t soft wheat at $268.16/t landed.

On the production side, Russian spring wheat planting continues to face weather-related delays, with rainfall across key growing regions running 60–118pc above seasonal norms, raising concerns around planted area and late-season disease pressure – not sure I’m overly concerned to be honest.

Russia’s July-to-May export pace remains strong at 45 million tonnes (Mt), up 10pc year-on-year.

In France, Rouen port loadings fell sharply to around 57,500t for the week.

Chinese state buyers are reported to be considering higher wheat imports for millers after harvest rains damaged a portion of the crop, with analysts estimating up to 7pc of output facing quality downgrades (I feel like we have seen this movie).

Implied volatility in Chicago July wheat edged higher to 24.72pc from 23.91pc.

Other grains and oilseeds: Corn extended its losing run, with July falling 7 cents to fresh contract lows and December off 8 cents.

The familiar combination of benign weather, absent Chinese demand, and continued long liquidation drove the move, with crude’s decline adding a further headwind.

Weekly corn export sales of 883,000t were below the 1.4Mt estimate, with the usual buyers of Japan, Mexico, and South Korea leading purchases.

Colombia was separately credited with 115,000t new crop in a daily announcement.

A confirmed case of New World Screwworm in a Texas calf attracted some market attention as a potential negative for cattle supply and downstream feed demand, though most participants viewed it as too early to trade.

Argentine corn harvest reached 40.6pc complete versus 34.7pc the prior week.

Soybeans were the session’s hardest hit, with July off 24.50 cents as Section 301 tariff concerns rekindled fears around Chinese buying of US soybeans, though some trade commentary pushed back on the severity of the risk given last month’s US-China summit commitments.

Old crop soybean sales of 277,000t and meal sales of 169,000t both came in below estimates.

Argentine bean harvest is 91.7pc complete.

Canola on ICE gave back most of Wednesday’s gains, falling around C$14/t across the board as soyoil, European rapeseed, and palm oil all declined in sympathy with crude. The Canadian dollar was marginally softer on the day.

Macro: The macro backdrop was somewhat bifurcated.

Crude fell nearly 3pc as the Israel-Lebanon ceasefire announcement raised hopes for broader Middle East de-escalation and potential reopening of the Strait of Hormuz, though Iran signalled little progress in parallel talks with the US and Hezbollah rejected the ceasefire terms.

The Republican-led House passed a war powers resolution 215-208 directing Trump to withdraw forces from Iran absent a congressional authorisation, though its path through the Senate remains uncertain.

Falling oil prices dragged Treasury yields and the dollar lower.

Weekly jobless claims came in at 225,000, above the consensus of 215,000 and up from a revised 212,000 the prior week.

The AUD was essentially flat on the day.

The Dow, despite the soft commodity and energy backdrop, registered a strong gain of nearly 875 points.

Russia’s deputy prime minister acknowledged for the first time that domestic oil production has declined since the start of the year, attributing it to unscheduled refinery maintenance, though Ukraine’s intensified attacks on Russian refinery infrastructure are widely seen as a contributing factor.

Local markets: Through the west of the country bids were firmer yesterday for canola with new crop A$860/t and current $820, while GM was $800 and $765. Wheat was $346 and $356, barley $325 current and new FIS Albany.

In the east canola was up $10 with old crop $781 and new $825, wheat was softer $334 and $349, barley $310 and $319 track Geelong.

Northern markets are trading slightly softer around $389 for barley and $387 for nearby wheat delivered Darling Downs, with new crop bid at similar levels. Barley remains harder to source than wheat.

The next week is looking promising for further follow-up rainfall across the country. Most growers through SA and Vic are now only a spring rain away from a crop, while another decent system is forecast for SQLD and NNSW where, after months of chasing moisture, growers are now waiting for paddocks to dry out enough to finish sowing. Quite the turnaround.

A proposed new US tariff could see Australian lamb, mutton, goat meat and wool products hit with an additional 12.5pc duty from late July, taking total tariffs as high as 22.5pc if current measures remain in place. The move, linked to a US investigation into forced-labour import controls, has been labelled “unwarranted and unjustified” by the Australian Government and adds another layer of uncertainty for sheep and wool exporters, while reinforcing the need for market diversification into destinations such as Vietnam, India and Bangladesh.

HAVE YOUR SAY