Weather: Spot fires – challenging conditions in Brazil for corn, the situation in the US HRW belt, most significantly KS and NNSW and SQld.

Depending on who you follow, there could be some decent rainfall for the north – always a reach when models are not aligned but there is a chance.

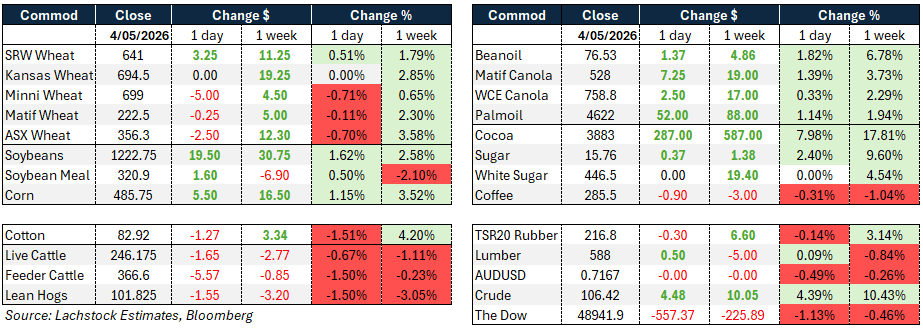

Markets

No end in sight – a break in the cease fire is strange – I get the action in the Strait but the drone strike in the UAE just seems random. Kuwait weighing in as well – something feels off.

Energy markets reacted as you would expect although its worth noting that they are giving some of the gains back in the night session.

China is still the barometer for global Ag commods – and its clear how excited the bean market is at the prospect of a China/US deal.

Day Ahead – Australia

All about the rate announcement today – not a certainty but close to it. The budget will be a stinker – the deficit blow out the cherry on top.

Grain markets are digesting the rainfall through the south which has generally been pretty good.

The north is still trying to find the spot that the grower gives up some of the length from last harvest.

Source: Bloomberg

Global wheat: Chicago July +3.25c, Kansas unch, MATIF -0.25 EUR/t

It was a mixed session for wheat, with Chicago SRW finding modest support while Kansas and Paris struggled for direction.

The headline driver was renewed Middle East tension after the US moved to reopen the Strait of Hormuz, sending crude sharply higher and generating broader market unease.

Wheat drew some indirect benefit from the energy bid but largely sat on the sidelines as crude and equities dominated price action.

On the weather front, the southern plains received less rain than expected over the weekend, though some additional rainfall is expected in the driest areas before a cold system moves through. Freeze watches are in place for a wide area stretching from Nebraska through Kansas and into the panhandles, with 49% of the winter wheat crop already headed and therefore at risk.

Monday’s crop condition ratings showed a marginal improvement of 1% nationally to 31% good-to-excellent, slightly above expectations, though Kansas slipped a further 1% to just 22%.

SRW conditions improved 2% to 60% while HRW states dipped 1% to 19%.

Spring wheat planting came in at 32% against an expectation of 33% and a five-year average of 35%.

Weekly export inspections of 434k tonnes were at the upper end of estimates, keeping the cumulative pace 12% ahead of year-ago levels.

Russian cash prices were quoted near $241 and US FOB values remain uncompetitive against global rivals, leaving the bull case short of fresh fuel.

With the May WASDE and various crop tours approaching, the market is expected to start assembling a clearer picture of production prospects next week.

Other grains and oilseeds: Corn +5.50c, Soybeans +19.50c, MATIF Canola +7.25 EUR/t

Corn and soybeans both posted solid gains, with energy markets firmly in the driver’s seat.

The extended closure of the Strait of Hormuz is raising concerns about input costs and the flow of agricultural commodities, and a longer closure is being seen as a potential threat to corn acreage intentions going forward.

Germination concerns and a frost threat for Parana’s safrinha regions added further support.

Weekly corn inspections of 2.028 million tonnes exceeded every estimate and pushed the cumulative export pace 31% above year-ago levels.

After the close, corn planting was confirmed at 38%, in line with expectations and ahead of the five-year average of 34%.

Fund positioning remains a factor, with CFTC data showing more than 50,000 long contracts added in corn for the week ended April 28, taking the net long to over 264,000 contracts — a level that limits the upside from any positive weather news.

In soybeans, the dominant theme was optimism surrounding the upcoming Trump-Xi summit, with reports that President Trump’s delegation has departed for China via US Air Force transport, cementing the meeting.

Old crop beans have been waiting for precisely this catalyst and the market responded with July soybeans up 19.5c, soybean meal advancing $1.60, and soyoil spiking sharply on the back of crude oil strength given its role as a feedstock for renewable fuels.

Bean inspections of 450k tonnes were at the low end of estimates and remain 24% below year-ago levels, and planting came in at 33% against an expectation of 35%, though well ahead of the 23% five-year average.

Macro: AUD 0.7168, Dow -557.37, Crude +4.48

It was an uneasy session as Middle East tensions flared sharply following the US effort to reopen the Strait of Hormuz.

US forces began escorting American-flagged commercial vessels through the waterway, while around 50 other ships were diverted.

Iran responded with cruise missiles, drones and small-boat attacks targeting US-flagged shipping, and carried out its first strike on the UAE since the early-April ceasefire.

Kuwait condemned the attack on a UAE-flagged tanker, and US Treasury Secretary Bessent called on China to apply pressure on Iran to reopen the strait.

Crude oil surged more than $5 at its peak before settling $3.69-$4.48 higher, and equity markets sold off aggressively in response to the geopolitical uncertainty, with the Dow closing down over 557 points.

The AUD was effectively flat on the day.

Domestically, the RBA is expected to raise the cash rate by 25 basis points to 4.35% at today’s meeting, with the decision driven by a still-tight labour market and trimmed mean inflation running at 3.5% year-on-year in Q1 2026, though the outcome is expected to be close with several board members likely to vote for a hold.

Local: WA canola was slightly softer to start the week at $800 and $840 for new season, wheat $343 old and $359 for new crop, barley $350 old crop and $340 for new crop FIS Albany.

In the east canola was steady at $790 and new crop $820, wheat was $345 and $374 for new crop, barley $319 and $332 nc track Geelong.

Delivered markets were largely unchanged despite some rainfall, with ASW Murray Bridge $353 for nearby and $365 Jan+, Griffith $372 and $388, Geelong/Melbourne $381 and $395 for new crop.

The two-week outlook is looking a little more conducive for rainfall further north into NSW and SQLD, which if it materialises will likely see some seeders pulled out, with barley hectares to be the most fluid here.

HAVE YOUR SAY