Weather:

Weather:

A pretty clear week in the northern hemisphere, allowing winter crop harvest to continue.

A mixed week in India – Uttar Pradesh and Madhya Pradesh both came in below normal – still lots of time for the monsoon to catch up but this will be watched – we are watching their local wheat price catch a bid, from a low base but is definitely firming

Markets

With the 4th of July holiday things where quiet into the end of last week. AUD sneaking back above 0.6900 but without conviction.

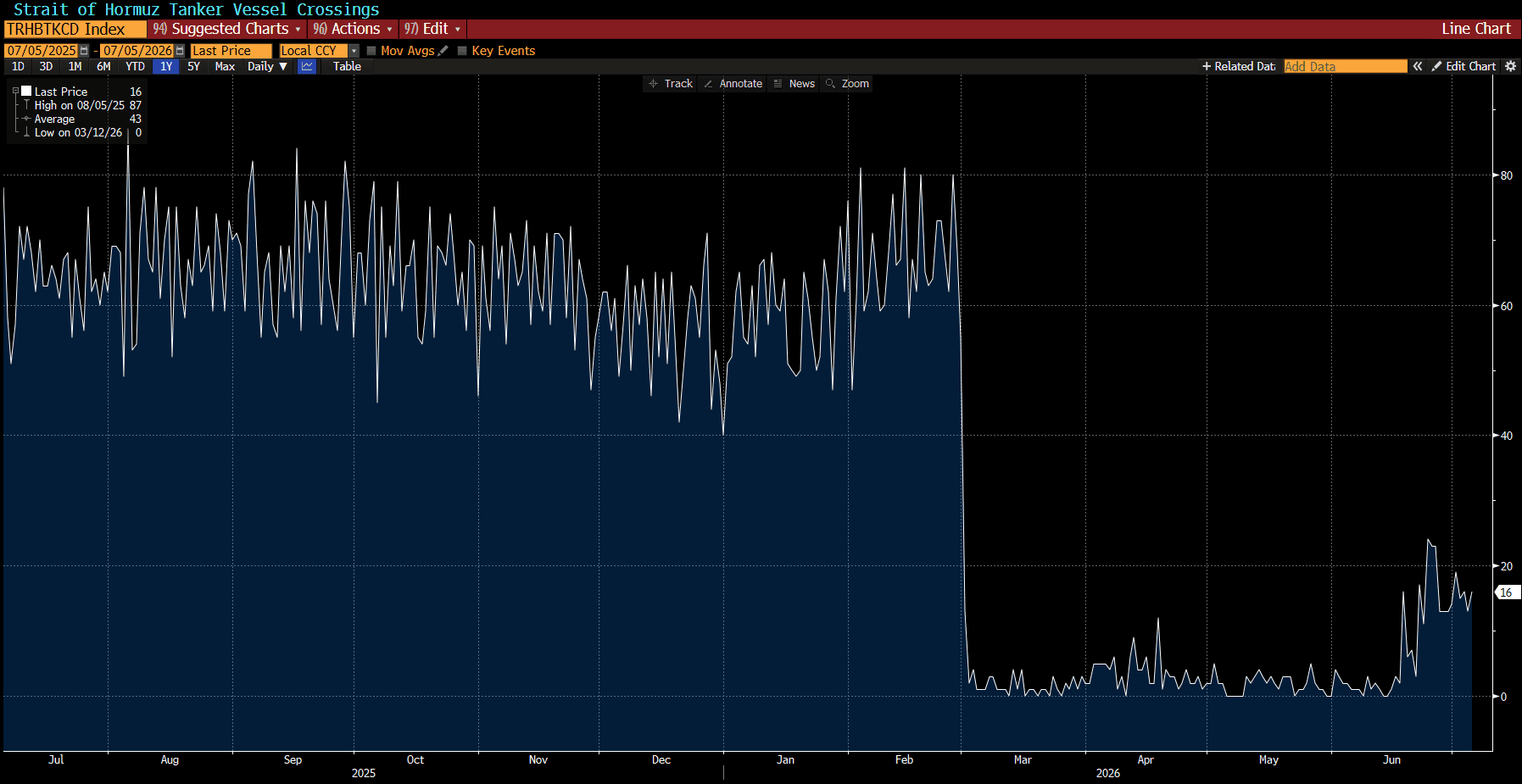

Energy markets have opened this week softer – vessels are flowing through the strait but not in any great style as yet.

Day Ahead – Australia

A mild week from a rainfall perspective – some will welcome this.

Markets should be relatively unchanged to start off the week.

Source: Bloomberg – Strait of Hormuz Tanker Crossings

Commodities and macro: 4th of July holiday in the states so a quiet news day.

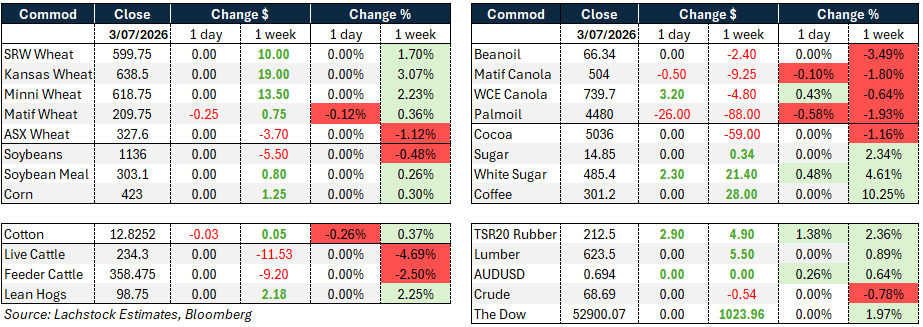

Nothing moved on the day with the US closed for Independence Day, so today’s session was really just a continuation of Friday’s settle. The bigger story is the week just gone, where Chicago, Kansas and Minneapolis all pushed higher, Kansas leading the complex at better than 3 percent. Matif held a similar path but far more muted, nudging fractionally lower into the weekend after its own weekly gain. ASX wheat sits apart from the pack, slipping on the week even as the US contracts firmed, a reminder that domestic conditions are still setting the tone locally rather than following Chicago’s lead.

Beans softened modestly on the week while meal and corn eked out small gains, a fairly unremarkable spread given the holiday-thinned trade. The more interesting divergence sits in oilseed products: bean oil and palm oil both fell hard on the week, palm oil extending losses into today as well. That weakness tracks the crude complex lower and reflects a softer biofuel demand read as OPEC+ signals more barrels coming to market. Canola told its own story either side of the Atlantic — Matif slipped both on the day and week, while Winnipeg firmed on the day even as it stayed underwater for the week, leaving the two markets pulling in different directions.

Equities carried Friday’s momentum into the new week, with Wall Street futures holding onto gains built before the holiday shut and the Dow’s weekly tally reflecting that lift. Sentiment remains cautious rather than euphoric — traders are still weighing the energy shock from the Iran conflict against whether AI-driven spending translates into earnings once Q2 season gets underway. Crude eased on the week as shipping through the Strait of Hormuz showed signs of stabilising via the Oman-side route despite a spate of unexplained tanker U-turns late last week, and OPEC+ added to the pressure by backing another modest output increase. Gold has been the standout macro mover, extending a fourth straight day of gains near $4,190 an ounce as markets pare back expectations for a Fed hike. The Aussie held firm on the week, tracking a broadly steady US dollar.

HAVE YOUR SAY