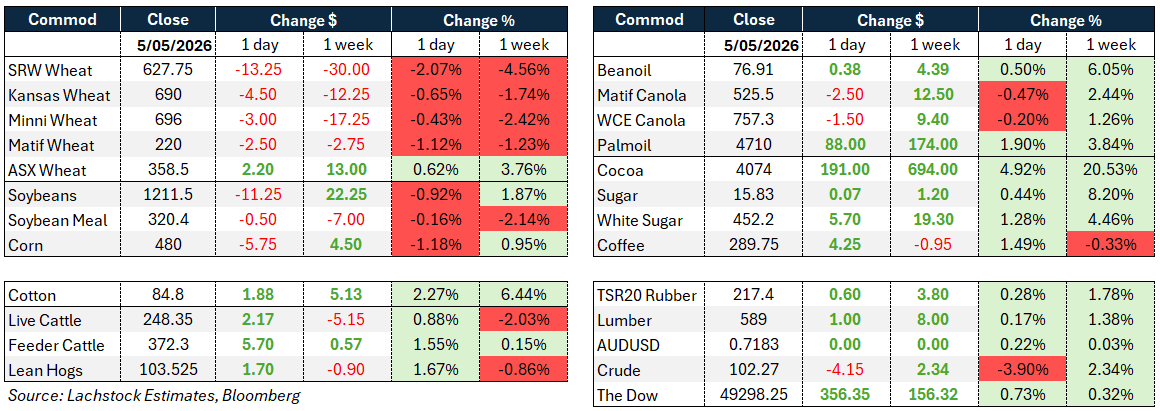

Weather: Weather remains a key driver for wheat markets, with ongoing drought, freeze and frost concerns across the US HRW belt continuing to threaten production and lift abandonment risk through Kansas and Oklahoma. Elsewhere conditions are more stable, with improving rainfall forecast for parts of Europe, Russia and southern Australia, although dryness is beginning to emerge in Brazil’s safrinha corn regions while forecasts for a below-normal Indian monsoon later this year are starting to attract attention.

Markets

Overnight grain markets were softer overall as weaker crude oil and profit taking weighed on futures, although ongoing drought and freeze concerns across the US HRW belt limited downside in wheat. Corn and soybeans eased on rapid US planting progress, while canola traded either side of unchanged amid weaker veg oils and crude oil offset by Prairie planting concerns. Broader markets were firmer as the Iran ceasefire held and the AUD stayed strong following the RBA’s hawkish tone.

Day Ahead – Australia

A little more engagement starting to emerge, with growers slowly beginning to come to the party on old crop marketing with northern markets having eased around $5 since mid to late last week. Expect wheat and canola markets to be softer today following weaker overnight futures and a slightly more enthused grower.

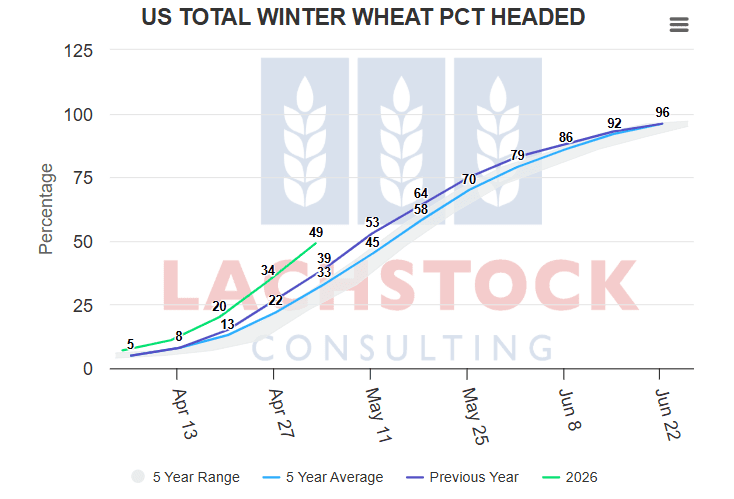

Global wheat: US HRW wheat crop conditions continue to deteriorate through Kansas, Oklahoma, Texas and Colorado, with drought, frost and freeze risk driving fresh concern around abandonment and production losses. Oklahoma tour estimates surprised to the downside with implied abandonment potentially record large.

Global wheat: US HRW wheat crop conditions continue to deteriorate through Kansas, Oklahoma, Texas and Colorado, with drought, frost and freeze risk driving fresh concern around abandonment and production losses. Oklahoma tour estimates surprised to the downside with implied abandonment potentially record large.

Wheat futures pulled back early in the week on profit taking, improved rainfall forecasts and weaker crude oil, however markets recovered off session lows as weather risks in the US Plains remain unresolved.

Funds remain heavily long KC and Minneapolis wheat, the largest bullish positioning since 2022 in some contracts, helping underpin the market despite recent consolidation.

Global wheat conditions outside the US are more stable, with Russian production forecasts still around 90mmt, Europe seeing improving rainfall and little concern currently around Black Sea planting conditions.

Attention now turns to next week’s WASDE and Kansas Wheat Quality Tour, with the market looking for confirmation of smaller US HRW production and elevated abandonment levels.

Wheat continues to take direction from broader macro and energy markets, with cheaper crude oil and improving Australian rainfall forecasts briefly pressuring values, although ongoing US weather issues are limiting downside.

Other grains and oilseeds: Corn and soybean markets saw profit taking after recent rallies, with fast US planting progress weighing on sentiment. Corn planting is running ahead of average while soybean planting is significantly advanced, supporting production expectations.

Despite the pullback, corn remains supported by elevated fertiliser prices, energy volatility, safrinha concerns in Brazil and ongoing uncertainty around US crop establishment conditions.

Brazilian safrinha corn conditions are beginning to deteriorate as the rainy season finishes, with dryness emerging in southern growing regions ahead of grain fill.

Soybean markets remain heavily focused on next week’s Trump/Xi meeting, with speculation around potential Chinese buying continuing to underpin sentiment. However, traders remain cautious that any confirmed buying could become a “buy the rumour, sell the fact” event.

Bean oil and crush margins remain extremely strong, with renewable fuel demand and RFS policy continuing to support crush economics and veg oil values despite weaker crude oil.

ICE canola traded either side of unchanged with weaker crude oil, soybeans and rapeseed weighing on prices, although cool Prairie temperatures and possible planting delays are increasing weather premium and market risk aversion.

Indian monsoon forecasts are beginning to attract attention, with below-normal rainfall expectations under El Niño potentially impacting pulse production and increasing import demand later in the year.

Macro: Markets adopted a more risk-on tone overnight as the US indicated the Iran ceasefire remains intact, pushing equity markets higher while crude oil eased lower.

Despite the ceasefire, disruption through the Strait of Hormuz remains unresolved, with Iran implementing new shipping protocols and concerns growing around tightening global oil and LNG supplies.

Falling crude oil prices pressured grains and oilseeds through the session, highlighting the increasing correlation between agricultural markets and broader energy volatility.

The RBA delivered another 25bp rate hike with a more hawkish tone than expected, supporting the AUD which continues testing recent highs.

US economic data continues to point toward a slowing but stable economy, with labour markets described as “low hire, low fire” and services activity remaining expansionary.

Aluminium, copper and precious metals all found support from easing Middle East tensions and ongoing supply concerns tied to the Persian Gulf region.

Traders remain highly focused on energy inventories and any acceleration in global stock drawdowns, with further tightening likely to flow through into fertiliser, freight and broader agricultural input costs.

Local: Bids were slightly firmer through the west of the country yesterday with canola $806 current season and $850 new, wheat $347 and $364, barley $348 and $338 FIS Albany.

Through the east canola was $790 and $820 for new season, wheat was $345 and $374, barley $316 and $333 track Geelong.

Northern markets have cooled a little over the last week with the Darling Downs bid $430 with the offer side closer to $442 back $10-$15 from recent highs.

Recent rainfall through parts of NSW and SA appears to be slowing the aggressive cattle turnoff seen over the past two months, with processor grids in the south lifting 20c/kg in places and saleyard prices firmer across several centres. Queensland processors remain well covered through May after heavy supply pressure through March and April, however yardings are now starting to decline and one major processor noted the “panic has gone out” of the market following scattered rain and improved seasonal optimism.

HAVE YOUR SAY