Weather: Weather remains a key swing factor across global grain markets. In the US, forecast rainfall across HRW regions over the next two weeks is critical, with meaningful moisture expected that could stabilise early crop conditions if it materialises, though follow-up rain through April will be needed. In South America, conditions are more mixed, with hot and dry weather starting to threaten Brazilian corn yields in key regions, while excess moisture in other areas is slowing soybean harvest progress.

Markets

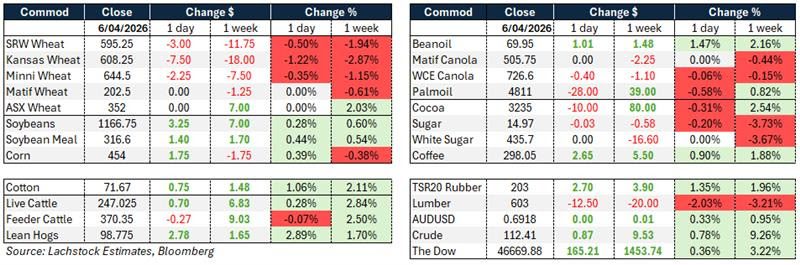

Grain markets were mixed, with wheat softer while corn and soybeans held modest gains, supported by strong US export inspections, particularly in corn. Oilseed markets remained firm, underpinned by strength in soyoil and supportive crush margins, while canola stabilised despite large speculative length. Global supply remains adequate, but ongoing demand and positioning are keeping markets supported in the near term.

Broader commodity markets are being driven by escalating Middle East tensions, with the US ultimatum to Iran keeping a firm risk premium across energy and ag markets. Oil remains elevated, supporting biofuel demand and underpinning vegoil strength. The next 24 hours will be telling, with the deadline around the Strait of Hormuz likely to dictate direction — either easing risk and taking some heat out of markets, or a sharp escalation that could see another leg higher across energy and commodities.

Day Ahead – Australia

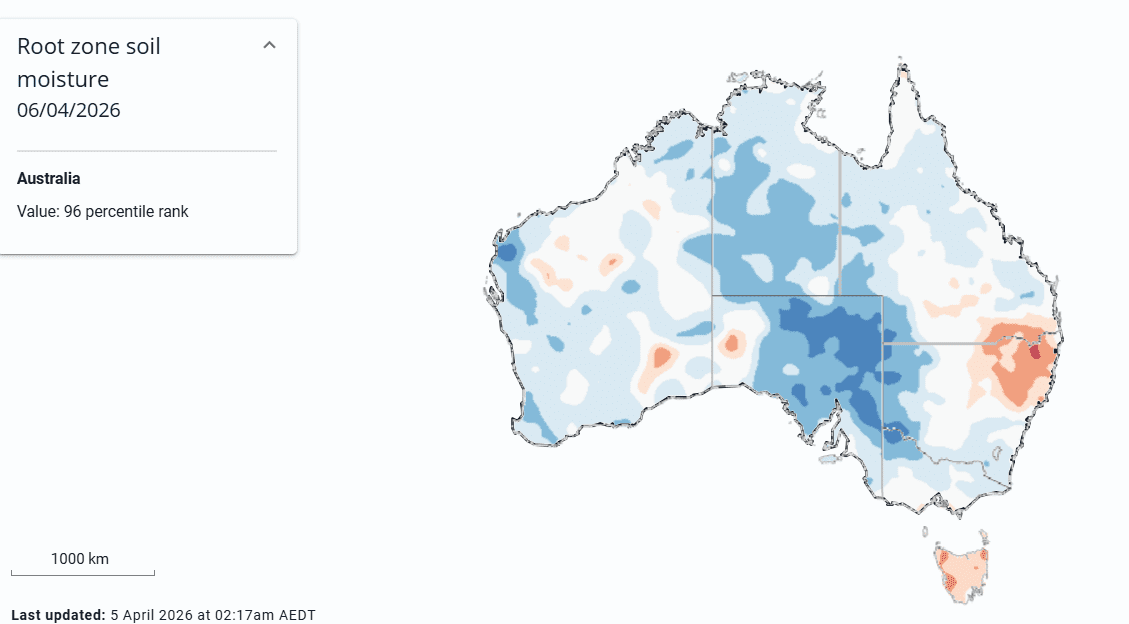

Australian markets should open largely steady. Canola firmer supported by strength in vegoil markets and elevated energy prices. The key driver today will remain macro, with Middle East developments front of mind — markets are likely to stay cautious, with direction dictated by whether tensions escalate or ease over the next 24 hours. Growing El Nino chatter- dry in NNSW and SQLD will see domestic homes continue to strengthen.

Global wheat: Wheat futures eased lower in a quiet, low-volume session, with markets largely in a holding pattern as traders wait on developments out of the Middle East and fresh US crop condition data.

Rainfall across US HRW regions is the key watch, with forecasts pointing to meaningful moisture over the next two weeks. If realised, this would help stabilise a crop that has started the season in relatively poor condition, though follow-up rain through April will be critical.

US export inspections slipped week-on-week but remain running ahead of last year overall, suggesting demand is still tracking well enough for now.

Globally, trade continues to flow with Australia picking up feed wheat demand into Asia, while Russia’s March export pace lifted sharply, reinforcing ongoing Black Sea competition and capping upside.

Positioning is notable, with funds holding large net long positions across US wheat markets, leaving the market vulnerable to volatility depending on how weather and geopolitics unfold.

Other grains and oilseeds: Corn and soybean markets were modestly firmer, underpinned by strong US export inspections, particularly corn which continues to run well ahead of last year’s pace.

Attention in corn is increasingly shifting to fertiliser costs, with India’s large urea tender highlighting tightening global supply and the potential for higher input costs to influence acreage and yield outcomes.

In South America, Brazil’s corn crop is facing growing risk from hot and dry conditions in key regions, while the soybean harvest is lagging last year due to excess moisture in some areas.

Canola markets stabilised and pushed slightly higher, supported by strength in soyoil and record crush margins, with a softer Canadian dollar continuing to underpin returns.

Broader vegoil markets remain well supported, with tightening palm oil inventories and rising biodiesel demand helping offset some macro uncertainty. At the same time, fund positioning across oilseeds is extended, increasing the likelihood of sharper moves if sentiment shifts.

Macro: Geopolitics remain front and centre, with the US issuing a firm ultimatum to Iran to reopen the Strait of Hormuz, while Iran has rejected ceasefire proposals, keeping the risk of escalation elevated.

Energy markets continue to reflect this risk, with crude oil holding elevated levels and physical markets tightening as buyers scramble for supply amid disrupted flows through the region.

The potential for prolonged disruption is extending beyond short-term logistics, with global LNG markets now facing a period of structural tightness following damage to key export infrastructure, reinforcing a higher energy price floor over the coming years.

Broader macro markets remain relatively contained for now, with US economic data surprising to the upside and supporting risk sentiment, although uncertainty tied to the Middle East continues to limit conviction.

Overall, markets are sitting in a highly reactive state, with weather, geopolitics, and input costs all pulling in different directions, setting up for increased volatility in the sessions ahead.

Local: Bids were softer on Thursday to end the week, although that already feels like a lifetime ago. Canola was $780 for current season and $825 for new crop, wheat $334 and $365, and barley $340 and $337 FIS Albany.

Through the east, canola was $760 and $796 for new season, wheat was $336 and $365, and barley $315 and $320 track Geelong.

There was no rainfall relief for NNSW and SQLD over the last week, and with El Niño chatter continuing to build, growers are shutting up shop and northern markets keep firming, with both wheat and barley delivered Downs now around $412.

Expect little trade today, with attention firmly on the Middle East conflict and the next 24 hours likely to be telling.

HAVE YOUR SAY