Weather:

Weather:

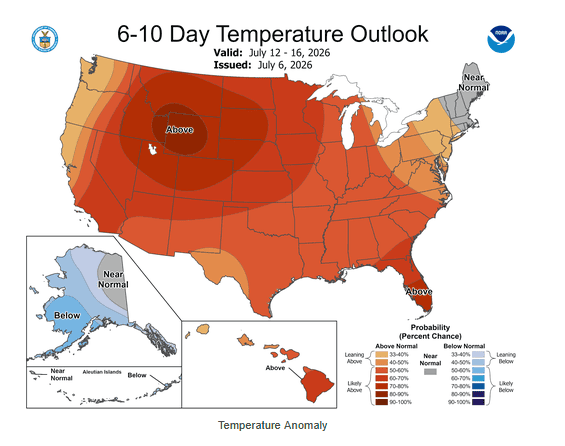

All about the US row crop heat – remember that one of the main determinant of yield in corn is overnight temps during the pollination window. Add to this rumours of China buying and it makes sense we caught a bid.

Indian monsoon is still lagging – local price has also been firming but is well below the highs of last year.

Argy could do with a drink – additionally, we note a few frosts – not so much crop damage but certainly sucks the moisture out.

Markets

Corn and beans led the charge (and this is not just US-centric) French corn conditions got hammered and the US is set to get hot.

There was a massive day in the Russia/Ukraine conflict but you would be excused for not knowing – hard to find daily commentary at the moment. Ukraine took out another 3 refineries in a clear strategy, meanwhile Russia smashed into Ukraine rail infrastructure. Both of these events will effect grain flow yet the massive Russian crop coming down the pipe trumps all.

Day Ahead – Australia

A strange thing in an El Niño year – but many will be happy for a few days of dry weather.

Canola looks amazing but so does demand – already this looks like the cash crop for this harvest.

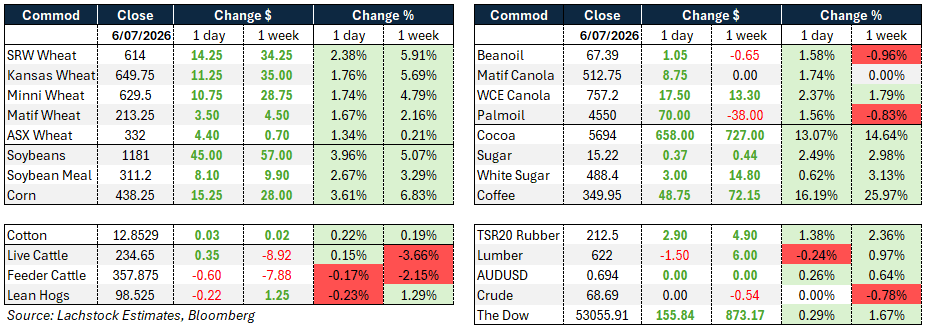

Wheat: Wheat snapped back hard after the long weekend. Chicago spreads firmed, KC softened, Minneapolis mixed, and WU vol jumped to 29.09 percent from 26.11pc as the market repriced ahead of Friday’s by-class balances — SRW carry-in is just 91 million bushels.

Wheat: Wheat snapped back hard after the long weekend. Chicago spreads firmed, KC softened, Minneapolis mixed, and WU vol jumped to 29.09 percent from 26.11pc as the market repriced ahead of Friday’s by-class balances — SRW carry-in is just 91 million bushels.

A hotter, drier six-to-fifteen day outlook drove the bid, though GFS still runs cooler than the EU model. Europe reinforced the tighter tone:

French wheat slipped to 68pc good/excellent from 74pc, harvest running well ahead of average at 26pc done, while French corn ratings collapsed 18 points to 58pc as a third heatwave bears down.

Black Sea flows are thinning — Sovecon pegged Russian June grain exports at 2.65 million tonnes (Mt) versus 3.6Mt in May, Ukraine’s 2025/26 wheat exports are 1.6Mt behind last year — while Saudi Arabia cleared 661,000t at $268-273.

War risk stayed live: Ukraine hit three Russian refineries and a Baltic terminal, Russia answered with a deadly Kyiv barrage, rail losses exceed 200 locomotives this year, all ahead of Trump-Zelenskiy talks in Turkey.

Brazil added a slower bullish plank: Conab sees 2026 wheat area down 13.4pc, Safras & Mercado down 17pc with output off 26.8pc to 5.9Mt, as weak prices and El Niño rain risk discourage sowing — a smaller crop points to heavier import needs ahead.

Other grains and oilseeds: Beans led on tightening balances plus demand optimism — China’s framework agreement in principle on tariffs turned into roughly ten cargoes bought Monday after weeks of empty morning checks.

The $17 billion annual ag-purchase target is a stretch, but Trump floating a Xi visit around September 24 kept the story alive.

Crush reacted: SX up 44.5c, BOQ up 99 points, SMQ up $7.40, though August margin slipped 20.5c to 249.75.

Corn rode the same wave off a short market and the Corn Belt’s hot, dry two-week outlook, with below-normal rainfall stretching from North Dakota to Tennessee.

Canola tracked beans higher, WCE clearing its 20-day average for the first time in three weeks on heavy volume (66,686 contracts vs 11,919 Friday, nearly half of it spreads), aided by a softer loonie; excess Prairie moisture now sits alongside Midwest heat as a shared weather worry. Palm oil outpaced a softer crude tape.

Macro: Light US data week. Wednesday’s June FOMC minutes are the focus and should show a hawkish tilt — six of eighteen members penciled in a hike in the June dot plot — but they’re the first under Chair Warsh, who’s already flagged easing inflation risk since that meeting and a preference to step back from forward guidance, so expect the tone to have moved on.

Rate-hike pricing has already been pared back post payrolls.

Urea has fallen near 17pc from its April/May peak of $866 to about $720, with Washington’s $500 million fertilizer aid adding further relief for growers. AUD steady; crude soft; equities grinding higher into the minutes.

Local: In the west of the country bids were reasonably strong yesterday on canola, unchanged on wheat and slightly lower on barley. New crop bids were A$835/t FIS for canola and $800 for GM, wheat was in the very low $350’s, and barley $330 FIS Albany.

Feeder cattle values, particularly on the Downs continue to strengthen amid solid feedlot demand.

HAVE YOUR SAY