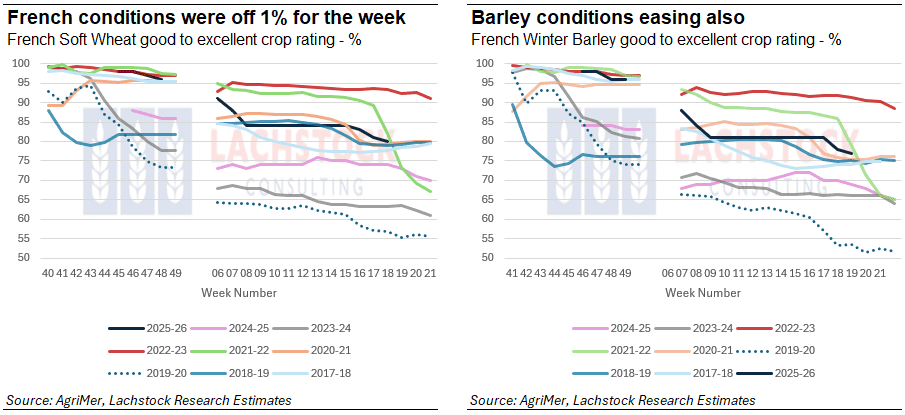

Weather: France’s wheat crop remains in solid condition at around 80% good to excellent, while dryness and delayed planting through Brazil have weighed on safrinha corn yield potential. Markets will continue to monitor US Plains weather alongside the upcoming Winter Wheat Quality Council tour and next week’s WASDE report.

Markets

Wheat markets were weaker overnight, led by sharp losses in Kansas futures after feared frost damage through the US Plains failed to eventuate, removing much of the weather premium from the market. Corn and soybeans were also softer, although both recovered well from early session lows as crude oil stabilised and buyers emerged at lower levels. Macro markets remain heavily focused on escalating Middle East tensions and ongoing disruption through the Strait of Hormuz, keeping energy and fertiliser markets volatile despite broader risk-off sentiment across equities and commodities

Day Ahead – Australia

Australian markets are likely to be softer today following weaker global wheat and oilseed markets overnight.

Yes, no, maybe- models can’t quite agree on the rainfall over the next 14 days with some showing moisture for NSW/QLD but not to the extent it was earlier in the week, fingers crossed.

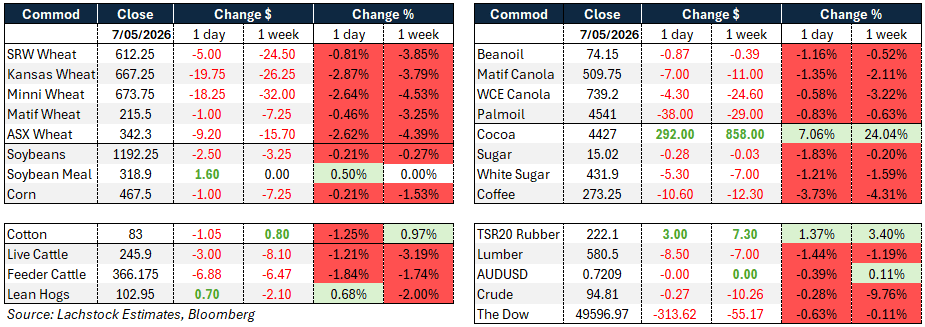

Global wheat: Chicago SRW -5.00 (-0.81%), Kansas -19.75 (-2.87%), MATIF -1.00 (-0.46%)

Global wheat: Chicago SRW -5.00 (-0.81%), Kansas -19.75 (-2.87%), MATIF -1.00 (-0.46%)

Wheat markets came under pressure across the board, with Kansas City the standout underperformer as a feared frost event in western Kansas and eastern Colorado failed to materialise, removing the weather premium that had been supporting hard red winter prices through the week.

Temperatures came in 7–10 degrees warmer than forecast, triggering aggressive selling across KC futures. Export demand did little to provide a floor, with old crop US wheat sales of just 79,000 tonnes well below the 200,000 tonne expectation, though new crop sales of 188,000 tonnes were ahead of ideas.

Algeria’s purchase of at least 390,000 tonnes of soft wheat at $268–270 per tonne provided some offshore demand context, with Cofco, Cargill, Bunge and others named as sellers.

The upcoming May WASDE is expected to show US wheat production down roughly 250 million bushels year on year to around 1.73 billion bushels, with some balance sheets now circulating with HRW exports below 200 million bushels as the market adjusts to elevated prices.

Drought conditions in the western Plains continued to worsen, with roughly 64% of Nebraska now in extreme or exceptional drought.

On a more constructive note, France’s soft wheat crop condition held firm at around 80% good to very good as of May 4, above last year’s 74%, and the Winter Wheat Quality Council tour is set to vie for attention alongside the WASDE next week.

Russian cash wheat remained just above $240 and Turkey and Morocco crop sizes are the subject of growing trade discussion, with larger harvests there potentially reducing import demand for US supplies.

Other grains and oilseeds: Corn -1.00 (-0.21%), Soybeans -2.50 (-0.21%), MATIF Canola -7.00 (-1.35%)

Corn staged a recovery from sharp early session losses to finish down just a cent, aided by a reversal in crude oil prices through the day and the fact that US corn remains competitively priced on world markets.

The market found buyers around 25 cents off recent highs, with weekly export sales of 1.362 million tonnes coming in close to the 1.4 million tonne expectation, with Mexico the leading buyer.

The upcoming WASDE is expected to show the 2026 US corn crop at 15.95 billion bushels, reflecting USDA’s March planting intentions of 95.3 million acres. Brazil’s safrinha corn crop was estimated at 112.1 million tonnes by Agroconsult, down sharply from last year’s record 123.9 million tonnes, with total Brazilian production seen at 140.5 million tonnes.

Dryness in key producing regions in April, combined with delayed planting caused by a wet soybean harvest in February and March, drove average yields down to 101.9 bags per hectare from 114.4 last year, though planted area edged up 1.5% to 18.3 million hectares.

Soybeans were choppy, finishing down just 2.5 cents after being off 10 cents earlier, but the fundamental backdrop remained soft.

Weekly US soybean export sales of 142,000 tonnes were a marketing year low, well below trade expectations of around 350,000 tonnes, with the old crop picture now largely contingent on the outcome of the Trump–Xi summit scheduled for May 14–15.

The WASDE is expected to show the 2026 US soybean crop at 4.45 billion bushels, a near 200 million bushel increase on 2025, on 84.7 million planted acres.

Argentina’s soybean harvest reached 34.3% complete, up from 18.3% the previous week, though a separate concern emerged with an unapproved GM soybean strain known as HB4 detected in shipments to Europe, raising the risk of cargo rejections for Argentina’s most valuable export. In products, soybean meal gained $1.60 while bean oil dropped 87 points, with South Korea’s Major Feedmill Group purchasing around 50,000 tonnes of soymeal at roughly $414.79 per tonne CFR.

Macro: AUD 0.7209 (-0.39%), Dow -313.62 (-0.63%), Crude -0.27 (-0.28%)

Markets remained firmly in the grip of Middle East risk sentiment, with the fog of the US–Iran conflict driving much of the price action across asset classes. US forces responded to Iranian attacks on Navy destroyers in the Strait of Hormuz, with Iran deploying missiles, drones and small boats against three warships, though no US assets were struck.

President Trump described the exchange as a “love tap” and stated the ceasefire remained in effect, though the situation remains fluid with Iran yet to formally respond to the US one-page proposal to reopen the strait.

The Dow fell over 300 points on the day, reflecting broader risk-off positioning ahead of the weekend and the evolving conflict. Crude oil whipsawed before recovering, with the war’s ongoing disruption to Strait of Hormuz traffic — affecting an estimated 13 million barrels per day or roughly 13% of world supply — continuing to keep energy markets on edge.

US gasoline prices have breached $4.50 per gallon for the first time since mid-2022.

On the US economic data front, April nonfarm payrolls are expected to show a gain of around 65,000 jobs, with the unemployment rate steady at 4.3% and average hourly earnings up 0.3% month on month.

While stronger than the zero-growth scenario outlined by Fed Chair Powell in March, the composition of gains is expected to be concentrated in non-cyclical education and health sectors, leaving underlying labour market momentum soft. The JOLTS job openings to unemployed ratio sits at 0.94:1.0, indicating a degree of excess labour supply.

Kevin Warsh takes over as Fed chair next week, with the Fed currently on hold against a backdrop of elevated energy prices and rising durable goods costs, with real WTI spot prices estimated to have risen around 20% in the first four months of 2026. India received phosphate fertiliser offers above $900 per tonne in a tender, a further sign of the war’s impact on input costs for major agricultural importers.

Local: WA canola was back A$15/t to $788, while new crop held at $835. Wheat was $340 and $358, with barley $342 and $338 FIS Albany.

In the east, canola eased to $776 and $812 new crop, wheat was $340 and $365, while barley was $316 and $328 track Geelong.

The Port Kembla/Geelong new crop wheat spread remains wide, with Port Kembla around $392 versus Geelong $360 track. While dryness through NSW is supportive, it is hard to see that spread as sustainable.

Delivered markets took a breather yesterday, with Hanwood back $5 to $365 for July and $381 Jan+.

HAVE YOUR SAY