Weather:

Weather:

French temps are expected to peak on the 14th for the second heat wave in as many weeks.

Russian harvest is a little later than usual with domestic press citing diesel shortages.

Markets

Game back on it would seem – the US returned to bombing Iran, Russia and Ukraine are stepping up their infrastructure attacks and Donald is threatening to cut off Spain.

The EU corn situation isn’t getting any better – the heat is set to increase into the weekend but it’s not just France. Poland crushers are looking at decent shortfalls with their rainfall well behind normal.

Grains don’t care however, wheat in particular giving back yesterday’s strength ahead of next week’s USDA report.

Day Ahead – Australia

Strong canola, flat to weak cereals. Pretty consistent theme. Despite a huge Russian crop coming down the pipe, Australian values are approaching export parity (depending on port) – the test will be how confident Asian demand is of accessing grain from a country that is actively at war.

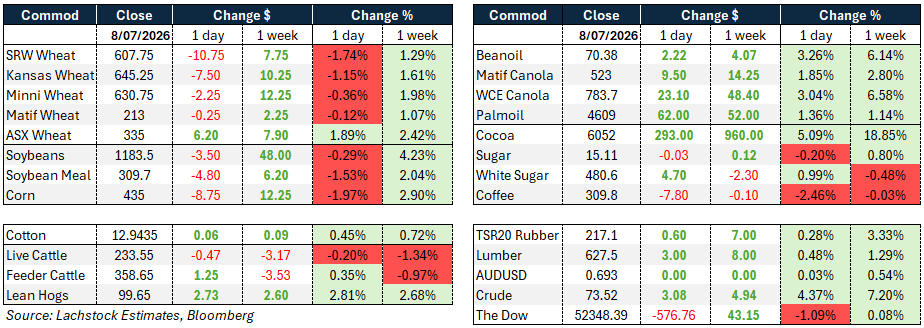

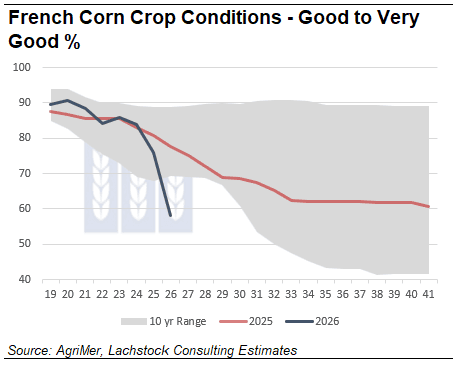

Condition rating good-to-very-good plummeted in weeks 25 and 26 outside the 10-year range indicated by the grey shaded area. Source: Agrimer, Lachstock Consulting Estimates

Wheat: Wheat gave back part of this week’s surge, WU stalling above 625 and running out of steam despite a firmer crude complex after the Iran ceasefire collapsed.

Focus shifted instead to a Russian crop tracking toward 90 million tonnes (Mt) and an absent El Niño in Australia, with rain forecast across both east and west over the next fortnight.

September SRW implied vol eased to 28.48 percent from 29.27pc, Russian cash sits near US$227.50/t fob.

SovEcon lifted its Russian export forecast 200,000t to 46.5Mt on larger carry-in stocks, though Sizov flagged a slow start to the campaign with buyers well supplied by local and Ukrainian grain.

Russia’s harvest is underway across 16 regions, over 4.5Mt threshed with yields ahead of last year.

Ukraine, targeting 23Mt this year, faces rain risk across the west, north and centre that could slow harvest and hit quality, a repeat of last year’s problem.

WASDE Friday is the next test: WSJ’s survey sees US wheat production at 1.52 billion bushels, down from 1.56 billion in June and the lowest since 1970.

Stratégie Grains cut EU soft wheat to 128.3Mt from 129.5Mt.

Thursday’s export sales are expected near 425,000t against a 315,000t pace requirement. Range view here is 590-630 September Chicago given the Russian crop and Australian conditions, with EU heat now more a corn story.

Other grains and oilseeds: Corn fell a second session, unwinding short-covering once CZ cleared US460c/bu and drew sellers, with the midday GFS flip turning cooler for the 11-15 day — the fourth straight day the model has reversed its prior read, leaving nothing reliable beyond five days out.

Stratégie Grains cut EU corn to 53.7Mt from 54.9Mt, still above the sub-50Mt estimates some are carrying.

Ethanol production slipped to 1.093 million b/d against 1.103 million expected, stocks down 3.1pc to 23.928 million barrels versus 24.64 million expected, the lowest since January.

Trump’s threat to halt Spanish trade is a wrinkle for corn demand given Spain’s drought-driven need for an estimated 150 million bushels of US imports this year.

Beans slipped despite a confirmed 472,000t flash sale to China (136,000 old crop, 336,000 new), which underpinned nearby spreads even as the front month’s push to 1204 drew profit-taking.

Five more China cargoes were bought overnight, part of Beijing’s move toward the White House’s 25Mt annual target, and open interest keeps building, up 19.5k Tuesday-basis.

Meal fell 3.90 in Q; bean oil was the standout, Q up 226 points as August crush expanded 16.75c to 273.25 on a diesel-led rally tied to renewed Iran tension.

Malaysian palm tracked the same vegoil strength, September contract up 21 ringgit (0.46pc) to 4,568. Canola rode the crude/soyoil complex to one-month highs at midday Wednesday, ICE November up C$17.00 to 777.60 and the curve firm throughout.

Chart-based buying above major moving averages and Western Canada flood damage added support.

Poland’s oilseed crushers flagged a 1.3Mt shortfall against 4.1Mt of capacity, harvest seen at 2.8-3.2Mt versus 3.6Mt last year after a 9pc cut to plantings; the industry is pushing government to lift the Ukrainian rapeseed import ban, and Poland looks set to be overtaken by Romania as the EU’s third-largest producer.

EU data showed 2025/26 rapeseed imports down 29pc to 5.4Mt, soybean imports down 3pc to 14.1Mt.

Macro: Crude jumped 4.37pc as the Iran ceasefire collapsed, Trump saying strikes hit Iran hard overnight with more to follow, after Washington revoked Tehran’s oil export waiver in response to attacks on commercial shipping.

Ukrainian drones hit three Russian refineries and tankers on the Sea of Azov overnight, extending a campaign that has left Russia short of fuel in places after Monday’s strike on the Omsk refinery, 1,700 miles inside Russian territory.

The Dow dropped 576.76 points on the day but is flat on the week, the geopolitical overhang offsetting an otherwise steady tape.

Trump also used the NATO summit in Ankara to threaten cutting off all trade with Spain over alliance spending, calling Madrid a poor partner; Spain’s response was measured, pointing to the trade surplus the US runs with it and calling the relationship “excellent.”

AUDUSD held flat at 0.693.

Cocoa extended its run, up another 5.09pc on the day and near 19pc on the week. Coffee eased 2.46pc; rubber and lumber both firmed modestly.

Local: In the west of the country bids improved again on canola, with fresh 26/27 highs being reached on GM. New crop bids were A$845/t FIS for canola and $812 for GM, wheat $354, and barley $330 FIS Albany.

Growers continue to be engaged on forward canola sales, and at the same time most exporters are keen to own some tonnes given the recent China buying activity.

HAVE YOUR SAY