Weather: The forecast is looking exceptional for all of Australia; if it materialises, it will fill in the gaps, particularly in Western Australia. In the US, rainfall through the eastern HRW belt and across the whole SRW belt is arguably not ideal. Need to watch. Good rain is forecast for Russia

Weather: The forecast is looking exceptional for all of Australia; if it materialises, it will fill in the gaps, particularly in Western Australia. In the US, rainfall through the eastern HRW belt and across the whole SRW belt is arguably not ideal. Need to watch. Good rain is forecast for Russia

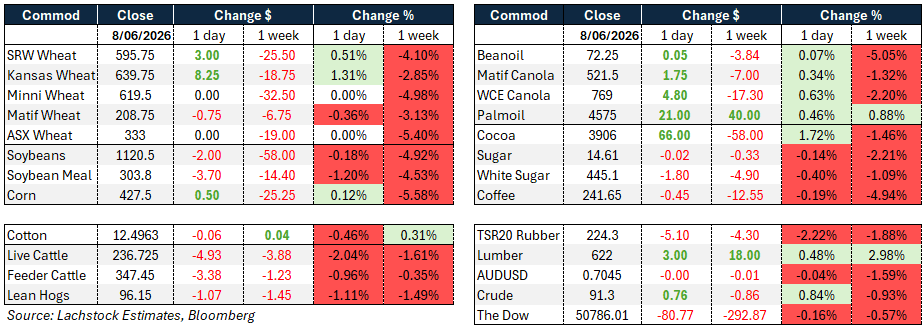

Markets: Game on again. Any talk of Middle East ceasefire is followed by missiles – zero confidence. WASDE this week will keep flows a little tight until we get the numbers. Australian wheat into The Philippines is becoming its only home; South-east Asian buyers are comfortable and watching Russian estimates tick higher.

Day ahead – Australia: Rain on the way will keep things quiet. It’s hard to see what changes in the export market at the moment; this Russian crop could be a behemoth.

Global wheat: The wheat complex found some relief Monday with Kansas Hard Red Winter leading the charge, supported by a reassessment of HRW crop prospects ahead of Thursday’s WASDE. The average trade guess for the HRW crop sits at 508 million bushels versus the May estimate of 515Mb, and sentiment has shifted meaningfully from the post-May view that we had seen the season’s low production figure. Conditions have continued to deteriorate rather than recover, with HRW states declining from 20 percent good to excellent in early May to just 14pc currently, a stark contrast to 2023, when ratings recovered significantly between May and final, adding 81Mb.

Winter wheat conditions dropped a further 1pc after the close to 25pc good to excellent, below trade expectations of 27pc, while spring wheat improved 5pc to 52pc, beating the 52pc estimate.

Anecdotal harvest reports from Texas and Oklahoma suggest crews are skipping typical stopping points or starting earlier than normal, though weekend rainfall has complicated harvesting logistics in those areas.

In SRW, excess rain moving into the mid-south is putting quality on watch.

Paris MATIF slipped €0.75/t with Russian cash around $241/t following a $3 hit on Friday.

Wheat inspections came in at 320,000 tonnes against 350,000t expected, though the pace remains 7pc above year-ago levels.

With the COT report showing 58,000 contracts of net selling in the wheat complex through last week, the market is positioned for a more meaningful recovery into the WASDE if the crop narrative continues to deteriorate.

Other grains and oilseeds: Corn managed modest gains despite fresh contract lows early in the session, with July adding 1.25 cents while December settled flat. The market continues to grapple with ideal early-season weather across the belt, with weekend rains described as heavy across northern Missouri and southern Iowa, providing a serious boost to developing crops. Corn inspections of 1.911Mt topped all trade estimates, and a daily sales announcement of 103,000t heading to Japan provided some support.

After the close, corn conditions were unchanged at 67pc good to excellent, marginally below trade ideas of 68pc and the five-year average of 69pc for the current week.

The broader narrative remains one of a market working through the aftermath of aggressive long liquidation — funds remain net long but at a fraction of recent peaks, with some suggesting the oversold condition may slow further selling.

China’s absence from the market remains a key pressure point, with tariff clarity seen as the likely trigger for any meaningful buying programme.

AgRural revised Brazil’s winter corn production estimate down 900,000t to 108.2Mt, with harvest at 4.4pc complete.

In beans, the sell-off continued with July dropping 5.75c, soybean meal shedding $5.80, while soyoil gained 44 points leaving July crush down 2.25c to 370.25c.

A daily sales announcement of 264,000t of new-crop beans to unknown destinations briefly supported prices, lifting new crop commitments to just over 1Mt, though notably none has come from China.

Bean inspections of 398,000t fell short of the 450,000t expected, and after the close conditions came in at 65pc good to excellent versus market expectations of 68pc, though slightly above the five-year average of 66pc.

The combination of absent Chinese demand, perfect early growing conditions, Brazil’s continued dominance of world trade flows, and still-elevated speculative length is keeping pressure firmly on the complex.

MATIF canola and ICE Winnipeg canola both recovered Monday, with the November contract settling at C$769.00, up C$4.80, as the market corrected higher after Friday’s sharp losses were deemed overdone. Both July and November contracts reclaimed their 20-day moving averages. Firmer crude oil provided spillover support alongside strength in Chicago soyoil and European rapeseed, while Malaysian palm oil was narrowly mixed. Seeding operations across western Canada are nearing completion, though some intended canola acres remained unseeded heading into the week.

Macro: The dominant macro theme Monday was the Israel-Iran exchange of missile attacks and the subsequent fragile de-escalation. The conflict’s disruption to the Strait of Hormuz continues to weigh on fertiliser shipments, adding an agricultural cost dimension that G7 agriculture ministers, meeting Monday, flagged as a key concern though without announcing specific relief measures.

Local markets: Through the west of the country cereals were steady to slightly firmer to start the week, with barley bid $325 current season and $329 new crop, wheat $345 and $358, while canola eased $15 to $810 current season and $840 new crop FIS Albany. Forecast models continue to point towards widespread follow-up rainfall over the next 7–10 days, further cementing what is shaping as an excellent start to the season across most Australian cropping regions. A softer AUD should provide some support for pulse exports, however underlying lentil demand remains subdued. With production prospects improving and another large crop increasingly likely, any meaningful rally still appears difficult without a material lift in offshore buying interest.

HAVE YOUR SAY