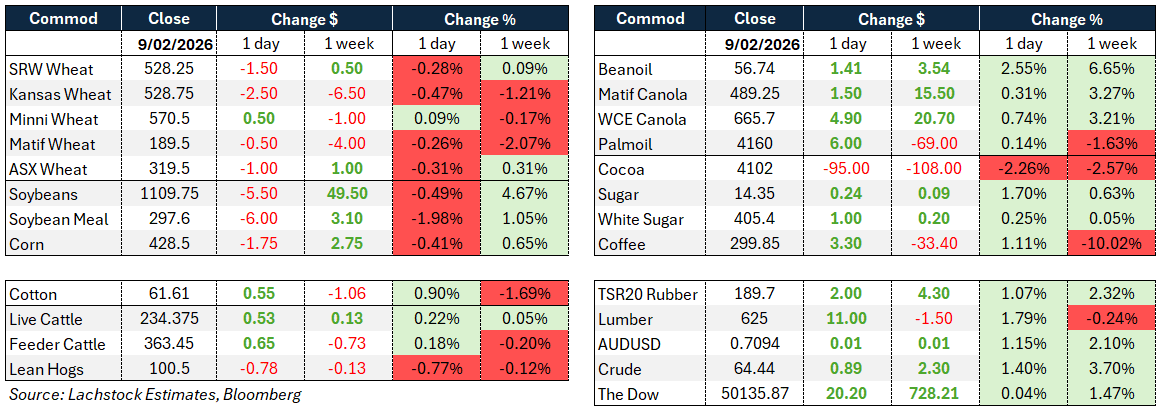

Weather: Given the recent hot temps through the US the crop is well and truly awake. The focus is now on moisture levels, particularly through the Mid west. Spring is in front of us but with SRW sitting at low $5/bu is there enough risk premium?

Russian logistics still dogged by excessive snow.

Rain through Qld/NNSW is becoming binary – good falls will give the northern grower some confidence, anything under 50mm would keep the market on edge.

Markets

All about the AUD- pushing 0.7100. RBA gave the market a stark reminder that growth is in question and Jim Chalmers gave us a word salad on what is driving inflation, govt spending or the private sector. Long story short, hedge funds haven’t been this long the AUD since 2017 when the AUD hit 0.8000

Australian Day Ahead

AUD will make values a little defensive today, as will the wait-and-see on the northern rain forecast.

Canola should stay a little flat.

Global Wheat:

Chicago -1c, Kansas -2.5c, Matif -0.50

Wheat remained directionless with markets largely treading water ahead of WASDE.

US futures eased modestly with no fresh catalyst, while spreads in Chicago and KC softened and Minneapolis held firmer.

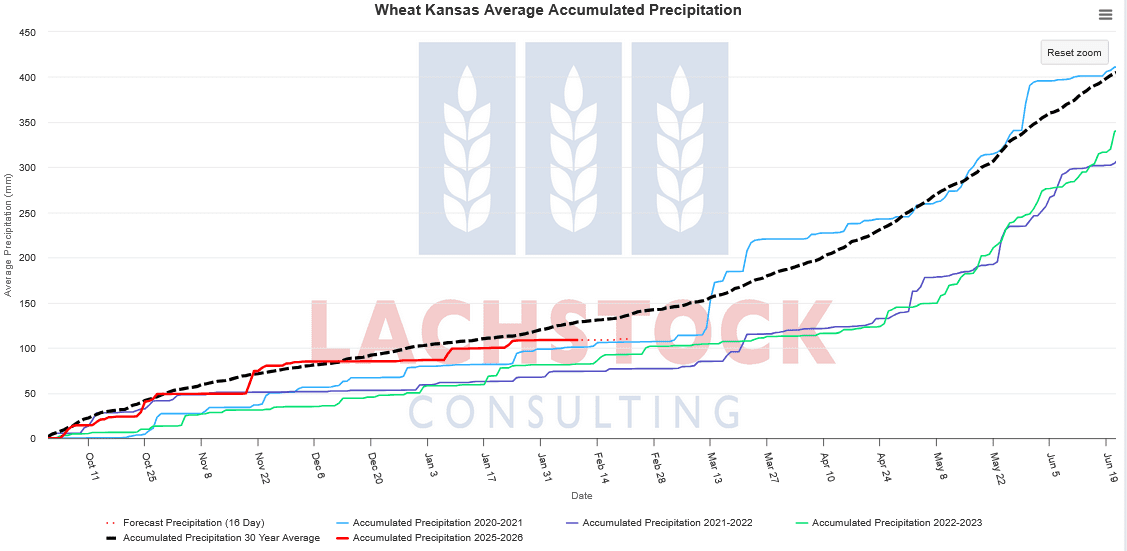

Limited rain is forecast for parts of the southern Plains later this week, but moisture looks short-lived.

Export inspections were a relative bright spot, coming in at 580kt and lifting the US shipment pace to around 18 percent y/y, with the Philippines, Bangladesh and Mexico the key destinations.

Globally, conditions remain unchanged: Argentina continues to ship aggressively, Australian grower selling remains restrained, Russian logistics are hampered by winter weather, and Ukraine exports are still constrained by the war.

Expectations for WASDE are low, with only minor reductions anticipated in US and global ending stocks.

Other grains and oilseeds:

Corn -0.4pc, Soybeans -0.5pc, Matif canola +$1.50

Row crops drifted lower ahead of WASDE, led by soybeans, as traders positioned for a largely uneventful report.

A USDA flash sale of 264kt of soybeans to China failed to impress the market and was largely treated as buy-the-rumour, sell-the-fact.

Attention remains on South America, where Brazil’s soybean harvest and safrinha corn planting are advancing, while improved rainfall is forecast for southern Brazil and Argentina later in the week.

US corn inspections surprised to the upside at 1.308 million tonnes, lifting shipments to 47pc y/y, though larger South American supplies and competitive Argentine FOB values are expected to curb US export demand later in the season.

Canola strengthened, supported by a sharp rally in soyoil and firmer veg oil markets, with good nearby pricing and basis continuing to attract attention despite expectations for a low-impact WASDE.

Macro: AUD0.7094, Dow +20.2, Crude +0.89

Macro sentiment was mixed. US inflation expectations eased further in the NY Fed survey, reinforcing the view that inflation remains well-anchored and supporting the case for rate cuts later this year. Focus now turns to upcoming US labour market and CPI data.

In Australia, the RBA’s historically weak medium-term growth forecasts have intensified debate over government spending, productivity and fiscal sustainability, with concerns mounting around long-term living standards.

Energy markets firmed as crude oil rose on renewed geopolitical risk in the Middle East, following warnings to US-flagged vessels near Iranian waters and concerns that tensions could disrupt supplies through the Strait of Hormuz.

China-related uncertainty also lingered, with reports that regulators are advising financial institutions to curb US Treasury holdings due to volatility concerns.

Local: Bids started the week steady in the west with canola A$780/t and GM $695, wheat $315 and barley $322 FIS Albany.

Through the east, bids were $759 for canola, wheat $320 and barley $306 track Geelong.

Barley continues to trade at a premium to wheat in the west, around $7 above APW, while spreads remain tight in the east with barley $10–$15 under APW. Barley liquidity is noticeably stronger than wheat in the east, with growers happy sellers into current strength.

Sorghum remains firm, with delivered Darling Downs trading $344 and Brisbane $366.

Donald Trump has temporarily lifted tariff-free US beef access for Argentina from 20,000t to 100,000t, specifically for lean trimmings used in ground beef — increasing competition into the grinding market that absorbs around 70pc of Australia’s US beef exports and likely capping upside in US trim prices despite tight domestic supply.

HAVE YOUR SAY