Weather: Illinois is 4 percent harvested and has received over 140mm in the last week with more on the way; the forecast is now pushing over 100mm into eastern Kansas as well – super wet. The Indian Monsoon start has been patchy, but generally above average in the main wheat-production areas; some forecasts are calling for well below average for the next two weeks.

Weather: Illinois is 4 percent harvested and has received over 140mm in the last week with more on the way; the forecast is now pushing over 100mm into eastern Kansas as well – super wet. The Indian Monsoon start has been patchy, but generally above average in the main wheat-production areas; some forecasts are calling for well below average for the next two weeks.

Markets: WASDE keeps the focus; we’re not expecting big changes.

Day ahead – Australia: The AUD is pretty shaky as it looks to test US70 cents again. Rain is sticking in the forecast, but parts of Western Australia have dried up a little. WASDE is on the way, which keeps things quiet.

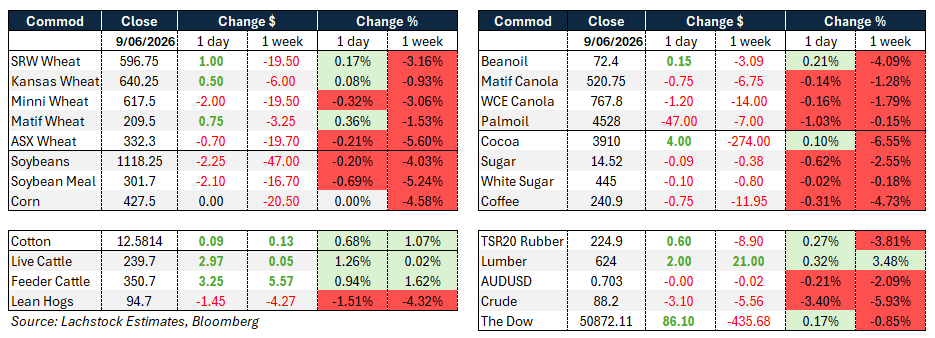

Global wheat: Wheat markets opened firmly but faded into the close, leaving Chicago fractionally higher and Kansas outperforming on the back of poor Hard Red Winter crop conditions. The most recent USDA Crop Progress report cut winter wheat good-to-excellent ratings by one point to 25pc, the worst on record, with traders engaging in short-covering ahead of Thursday’s June WASDE. Early harvest reports suggest HRW protein is running a little better than feared, though the sample size remains small and a crop below 500 million bushels versus the May estimate of 515m is plausible. Quality risks for Soft Red Winter are also emerging, with heavy rainfall forecast across the southern corn belt and mid-south over the next 10 days.

Managed money sold 58,000 contracts of wheat in the last COT reporting period, leaving the market in better structural shape to trade both sides rather than the one-way price action that characterised late May and early June.

On the demand side, Jordan purchased 60,000t from CHS at $275.20/t for second-half August shipment and has issued a fresh tender for September-October. EU soft wheat exports for the season reached 22.05 Mt, up from 20.55Mt a year earlier, with Morocco, Saudi Arabia and Egypt the leading destinations.

Ukraine’s deputy economy minister noted grain exports would total roughly 37Mt tonnes this season, leaving an extra 6-7Mt to carry into the new season.

Russian cash prices were unchanged at $241. In Paris, MATIF September settled €1/t higher on the session.

Other grains and oilseeds: Corn managed only fractional gains, despite an intraday spike following Trump’s Truth Social post on Iran, with July settling around $4.20 per bushel. The underlying demand picture remains supportive, with the USDA confirming a flash sale of 120,000t to unknown destinations for 2025-26 delivery, and South Korea’s Major Feedmill Group purchasing an estimated 134,000t of feed corn in an international tender.

US crop conditions held steady at 67pc good to excellent, the same as last week, and the weather outlook for the coming week is benign, with good rainfall and seasonally warm temperatures expected across most growing areas.

Thursday’s WASDE is not expected to bring major domestic changes, though world corn and soybean ending stocks are seen moving higher with upgrades expected to Brazilian and Argentine production.

Soybeans recorded their eighth consecutive lower close, with July off 2c to $11.14c/bu, meal down $1.60 and bean oil the lone bright spot, finishing up 35 points.

Brazil continues to dominate world trade flows and its weather outlook remains non-threatening.

Indonesia announced a 500 billion rupiah subsidy on 250,000t of soybeans to offset pressure from the weak rupiah.

ICE canola settled marginally lower after a choppy two-sided session, with July finishing down C$1.20/t at $760.10 and November also off $1.20.

Gains in Chicago soyoil provided early support but faded, while lower crude oil and mixed signals from the Canadian dollar offered little sustained direction.

Flooding concerns in parts of western Canada and the possibility of some intended canola area going unseeded were modestly supportive. Canadian canola exports in April totalled 780,600t, down from just over 1Mt in March, though Chinese purchases rose to 480,000t from around 384,000t the prior month.

Macro: The dominant macro theme of the session was the escalating US-Iran conflict, which delivered a jolt to markets mid-session before most commodity futures reverted to pre-announcement levels. US Central Command confirmed self-defence strikes against Iran following Trump’s claim that Iranian forces shot down a US Apache helicopter over the Strait of Hormuz, with Iran’s state media reporting explosions on Qeshm Island. Both pilots were recovered safely.

Crude settled modestly higher on the day as some traffic returned to the strait, but WTI moved higher in after-hours trade as the fresh strikes came through. Mediation efforts involving Pakistan as an intermediary are reportedly continuing, and a broader deal remains on the table, though the attacks add fresh uncertainty to peace prospects.

The Houthis in Yemen separately announced a complete ban on maritime navigation for Israeli vessels in the Red Sea.

The Iran war risk premium that had swept through crop and fertiliser markets has been fading, with urea prices falling more than 30pc since mid-April and the Bloomberg Agriculture Spot Index retreating roughly 10pc from its mid-May peak.

China’s May crude imports slumped 29pc to their lowest level since February 2018 at 7.79 million barrels per day, continuing to weigh on global oil prices.

The Dow finished down 80.77 points. The AUD was little changed on the day.

Thursday’s June WASDE will be the next major scheduled catalyst for grain and oilseed markets.

Local markets: Canola started the week in the east around $770/t current crop and $810/t new crop, wheat was $328/t and $335/t, while barley was $312/t and $320/t track Geelong. In the west, canola was steady with current season around $800/t and new crop $845/t, wheat firmed slightly to $348/t and $358/t, while barley was $333/t and $328/t FIS Albany.

Forecast rainfall over the next 10 days remains favourable for most cropping regions, although El Niño concerns continue to linger, particularly across northern Australia. With seasonal uncertainty still ahead, growers remain reluctant sellers at current new-crop values and continue to target prices well above the market.

April export data again highlighted the strength of barley demand, with 1.53Mt shipped during the month, taking 2025-26 exports to 8.01Mt. China accounted for 6.3Mt of that total. Wheat exports reached 1.40Mt in April, alongside 512,000t of canola and 341,000t of sorghum.

HAVE YOUR SAY