Weather: A hot finish to the soybean crop in the US creates some interest. It will be in the 90s°F for the next few days. Harvest is just kicking off so maybe this won’t be an issue.

Markets: A massive outside market day – huge revisions to US jobs data with 911k fewer jobs in the year to March 2025. This puts a little more credence behind a 50 bp cut next week by the Fed. Israel had a crack at the Hamas leader in Qatar – this marks a huge escalation when they are involving other Arab nations. Additionally, Trump is wanting to cause Russia as much pain by hitting their buyers of oil such as China. Just a thought but if Donald wanted to help his farmers, sanctioning Russian wheat would be a pretty quick way to add some value.

Australian Day Ahead: From a price perspective we have some headwinds. Russian values bleeding lower coupled with the potential for a 50bp cut by the Fed would firm the AUD (partially priced in already).

Offshore

Offshore

Wheat

US wheat futures eased modestly, giving back part of Monday’s rally. Chicago December lost 3.5c, Kansas dropped 7c, and Minneapolis slipped 3.5c, while Matif Dec fell €2.25/t and Russian cash moved down to US$228.

Spreads were flat to weak and participation light, with implied vol in WZ at 21.24 percent.

StatsCan reported all-wheat stocks at 4.1 million tonnes (Mt) vs 4.4Mt expected and 5.3Mt last year, a mildly supportive number but overshadowed by larger production expectations elsewhere.

US carryout is expected near 865m bu versus 869m in August, with world carryout projected at 261.1m vs 260.1m.

Ukrainian officials are pushing for tighter sanctions on Russia following escalations, while Ukraine plans to lift 2026 winter grain sowing to 5.43m ha (wheat 4.78m ha). Russia has already harvested 105Mt of grain and kept its full-year forecast at 135Mt.

US wheat continues to feel like a residual supplier, with export demand weak, while EU values show better potential to feed into rations.

Other grains and oilseeds

Corn futures were lacklustre, trading in a tight 3.5c range and closing down 2c.

The debate over yields continues with expectations for Friday’s WASDE at 186.2 bu/acre vs 188.8 in August.

Analysts remain split, with disease worries versus high yield forecasts from private forecasters.

EIA ethanol output is expected at 1.078m bpd with stocks near 22.6m. Soybeans traded down 2.5c in a narrow range. Meal rallied $5.80/t after a fire at ADM’s Decatur complex, though details suggest damage may have centred on the corn plant.

Oil lost ground, with funds exiting spread positions.

The tug-of-war continues between dry US finishing conditions and lack of China buying.

Malaysian palm oil futures steadied at MYR 4,485/t as traders await MPOB data, with inventories expected to rise for a sixth month despite stronger exports.

Turkey issued a tender for 18,000t of crude sunflower oil, while Iran’s SLAL tendered for up to 120,000t each of feed corn, feed barley, and soymeal.

In Argentina, authorities approved a Beijing Dabeinong subsidiary to grow GM soybeans.

Macro

US payroll revisions showed job growth was slower than previously thought, with 911k fewer jobs added in the year to March 2025 (76k/month vs 146k).

Markets are fully priced for a 25bp Fed cut next week, with a small chance of 50bp. Small business optimism ticked up in August to 100.8, though labour quality remains the top concern.

France appointed Sébastien Lecornu as PM, its fifth in two years, tasked with navigating a budget through a fractured parliament.

Cattle futures locked limit down despite stronger beef values, with expectations of softer beef demand tied to weaker labour data. China’s beef demand is projected to decline for a second year in 2026 as household incomes shrink.

Perdue Farms is cutting 300 jobs as turkey production slumps to 30-year lows, hit by avian influenza, inflation, and shifting consumer preferences.

Geopolitically, Trump floated sweeping tariffs on India and China if the EU joins in, aiming to pressure Russia, while new sanctions on Russian oil majors and its shadow fleet are under discussion.

Argentina’s peso hit a record low after Milei’s party lost local elections, sparking a 13pc equity market drop.

In the Middle East, Israel struck senior Hamas leaders in Doha, marking its first attack on Qatari soil. The move angered Arab nations and raised tensions, pushing oil up 1.8pc to above $63/bbl. Regional security risks are heightened, with criticism from Qatar, UAE, Iran, and Kuwait.

Additional headlines include widening of the US ag trade deficit to $33.6b YTD, extreme weather in China with its hottest summer since 1961 and record-long rains in the north, and continuing political battles in Washington over renewable fuel blending obligations.

Australia

Through the west canola slipped again yesterday with conventional around A$815 FIS Albany. GM still isn’t clawing back any ground on conventional, which is a bit surprising given the Winnipeg move. Wheat eased to $337, and barley ticked down to $310.

In the east, canola was off another $5 to $783 track Port Kembla. Wheat held steady at $322 and barley at $302.

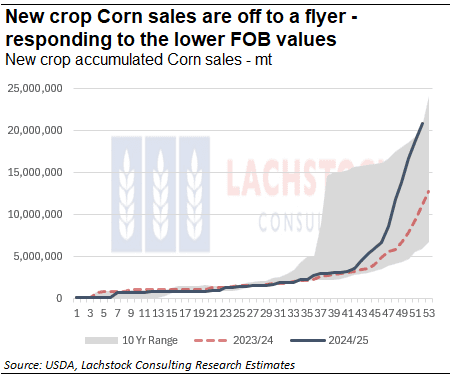

Faba bean exports are shaping up for about 600kt in 24/25, with close to 500kt of that pencilled for Egypt. New crop Egyptian demand is sluggish though, and with roughly 80pc of exports headed there last year it’s pretty clear why new crop bean prices are under pressure.

Handy rain through SA and Vic overnight with 10–20mm across the Mid North/Yorkes, Eyre and Murraylands, and a nice 20mm in the northern Vic Mallee. Southern NSW looks set to grab a share today as the front rolls through.

HAVE YOUR SAY