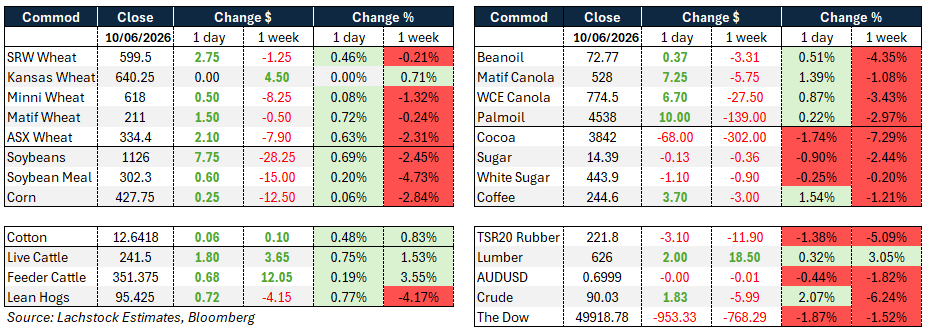

Weather: If the forecast is correct, things are going to be pretty damp in the Southern part of the east coast belt over the next week

Weather: If the forecast is correct, things are going to be pretty damp in the Southern part of the east coast belt over the next week

Widespread rain drenches the US Midwest through the weekend (1.5-3″+ from Oklahoma to northern Illinois), broadly bearish for new-crop corn and beans and likely to lift weak crop ratings, though too much rain in SRW areas threatens wheat test weights.

In the Canadian Prairies, heavy storms flooded fields across western Manitoba and eastern Saskatchewan (250mm+ in Stonewall, 117mm in Winnipeg), threatening canola acres.

Markets

Pete Hegseth summed up the current state of the war, indicating the US will “Negotiate with bombs”.

Crude jumped as much as 2.7% to $92.45 before settling around $90 as fresh US strikes on Iran for a second straight day strained an already-fragile ceasefire, with Iran retaliating against US bases in Jordan, Kuwait and Bahrain

The last three session have seen massive trading ranges in Chicago – not wildly unusual leading into a WASDE but shows the market really doesn’t know what to do with wheat.

Day Ahead – Australia

AUD sub 0.7000 adds support that the rainfall outlook takes away.

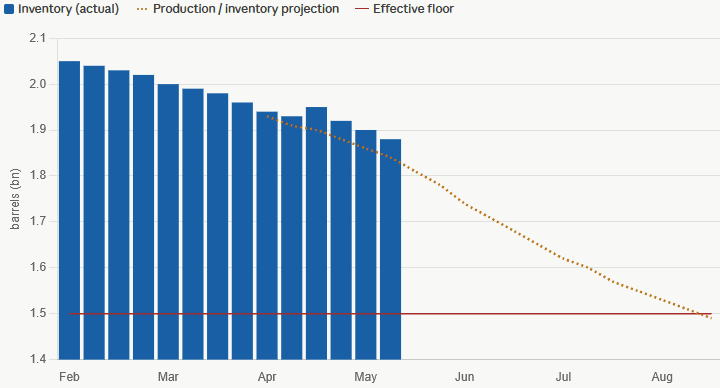

More talk about the inventory draw on refined products – Terminal gate prices certainly dont tell you there is a problem but i cant see how we cut 20% of global supply off and there isnt a draw down/tightening coming… and coming hard.

Oil Products:

Global inventory of oil products

Source: S&P Global, Macrobond, ANZ Research

Global wheat: Wheat posted another modest day-session gain, with WN up 2.25c, KWN off a quarter, MWN up fractions, Matif Sep up €1.50 and Russian cash up $1 to $242.

The week’s pattern held: strength overnight, struggle by day. WN touched 600.25 pre-pause but settled at 587.50, not far above the recent 580 low.

Drivers were familiar — too much rain threatening SRW quality, likely lower HRW production in tomorrow’s WASDE, and the “super El Niño” (now a 67% chance of a strong event into 2027).

Old crop exports are seen flat, new crop near 400k.

Globally, Rusagrotrans pegs June Russian exports at 1.85m tonnes; Coceral left EU-UK wheat little changed at 143.7m tonnes (-4.7% y/y); and Ukraine’s farmers’ union warned Black Sea port damage threatens a significant cut to shipments, with sowing 96% done.

Other grains and oilseeds: Corn ended mixed (CN off fractions, CZ up 1.5c) as benign weather leaves the market range-bound, but the options pit lit up: 44k CZ 490/530 call spreads blocked over two days plus another 32.9k Dec 490/530 on the day.

With rain everywhere, the hunch is Chinese demand — JCI suggesting China’s back-to-back auctions are clearing warehouse space for large-scale corn imports.

Sales are seen at 1.15 mil old, 350k new. Coceral cut EU-UK corn 5% to 57.2m tonnes. Beans broke an eight-day losing streak, SN up 9.25c on unconfirmed China-buying rumours, though a bounce was overdue regardless; SMN up $0.80, BON up 42pts.

Only minor WASDE changes expected, with Conab also due.

Canola firmed as flooding across western Manitoba and eastern Saskatchewan (250mm+ in spots) threatens acres, with spillover from crude, soyoil, rapeseed and palm; Nov settled 774.50, up 6.70.

Macro: Crude jumped and equities fell after fresh US strikes on Iran for a second day, with WTI up as much as 2.7% to $92.45 before settling at 90.03 and the Dow down nearly 2%.

Iran retaliated against US bases in Jordan, Kuwait and Bahrain, escalating beyond April’s ceasefire.

The flare-up overshadowed a softer US CPI (core +0.2% vs +0.3% expected), but traders held a Fed hike by year-end and extended the rotation out of tech (Nvidia -3.7%, Super Micro -28%).

The AUD fell ~200 pips on the week to 0.6993 — the CPI miss too small to shift Fed pricing, the Aussie hit as a risk proxy in thin Asian hours, and NAB’s shift to no RBA hike removing a pillar of support.

Local markets: WA bids were steady yesterday with canola at $810/t and new crop $846/t, wheat at $346/t and $357/t, and barley at $330/t and $327/t FIS Albany.

In the east bids were slightly firmer with canola at $771/t and $809/t for new crop, wheat at $325/t and $340/t, and barley at $310/t and $319/t track Geelong.

Liquidity has improved in the barley market across Victoria and NSW, with growers generally willing to meet current bids. Wheat remains a different story, with growers still estimated to hold 30–40% of old crop stocks and showing little urgency to sell. The end of the financial year may encourage some movement, however current global fundamentals remain bearish and growers may be waiting some time before seeing prices return to levels they are targeting.

HAVE YOUR SAY