Weather: Europe and the Black Sea are all set to get a drink over the next week which will be beneficial.

Not much in the way of relief for the western part of the US wheatbelt – coincides with the wheat tour. They head to western KS over the next few days – 28°C and clear skies from what I can see.

Central Australia is going to get hit again with 2-25mm through the pastoral regions.

Markets

The Farrer By-election, triggered by Sussan Ley getting replaced by Angus Taylor, was a canary in the coal mine for both sides of the aisle. Farrer has historically been a Coalition stronghold – but, the Libs and Nats managed just 20 percent of the vote – One Nation getting 41pc. This is a clear signal that the Coalition have no chance without some sort of deal with Pauline. Meanwhile, on Budget Eve, Labor is arguably getting a vision of its future with Sir Keir Starmer in the UK getting smashed in local elections, on top of a local swing to One-Nation.

The budget will have some influence over the AUD – it has never been a significant trading event but, given some of the changes predicted, this one could be more meaningful.

Day Ahead – Australia

Like it or not, the Aussie market will have one eye on the budget this week. According to AI, the forgone revenue from both CGT and negative gearing comes in around A$20B, but is heavily concentrated over the top 10pc of Australian earners.

Mixed bag today – US President Donald Trump has rejected Iran’s response to a US proposal to end the war, calling it “totally unacceptable”. It was reported to include an offer to end the blockade of the Strait of Hormuz and dilute some its highly enriched uranium in exchange for sanctions relief and lifting a US ban on Iran’s oil sales. So we are still in a war market it would seem.

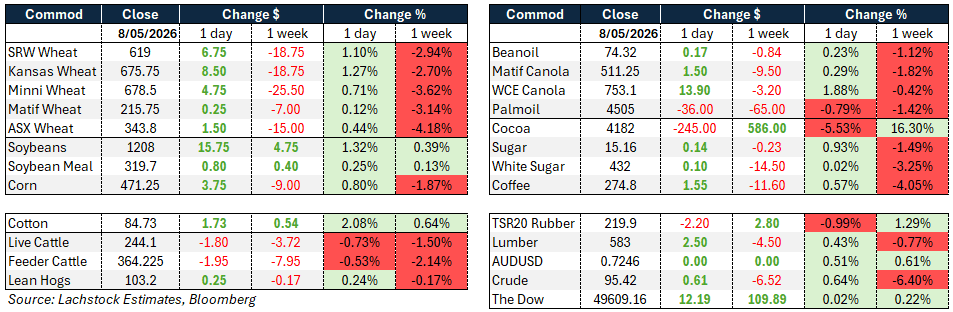

Global wheat: Chicago SRW +6.75c | Kansas +8.50c | Matif +0.25€

Global wheat: Chicago SRW +6.75c | Kansas +8.50c | Matif +0.25€

Grain markets found their footing heading into the weekend after a rough few days, with wheat the natural beneficiary of position-squaring ahead of a week loaded with risk events.

Chicago July wheat ended up 6.75c, Kansas gained 8.50c and Minny added 4.75c. Implied vol in Chicago wheat edged slightly higher to 30.96pc.

The bounce was largely technical in nature — markets had been sold off hard earlier in the week and with the May WASDE, the WQC hard red winter tour, and the Trump-Xi summit all due next week, few were keen to carry short exposure into the weekend.

The HRW crop remains the key wheat fundamental, with the USDA’s current production estimate of 629 million bushels looking increasingly optimistic against trade estimates clustering near 600 million and below.

Separately, the FAO flagged global wheat production edging down to 817 million tonnes in 2026, citing Strait of Hormuz disruptions lifting input costs and squeezing margins, though the figure remains above the five-year average.

In Western Australia, GIWA reported canola area set to jump by one-third to a record, with farmers rotating away from wheat – proving rotations are more about rainfall and its timing than anything else. Interesting to not they have total planted area up 8.2pc year on year.

Other grains and oilseeds: Corn +3.75c | Soybeans +15.75c | Matif Canola +1.50€

Corn ended the week with a quiet bid, July up 3.75c and December adding 4.00c.

Support came from the same risk-event positioning that underpinned wheat, alongside ongoing safrinha weather concerns in Brazil, though the worst of the cold threatening US germination appears to have passed.

Brazil’s 2025/26 corn crop is now forecast at 140.1-140.5 million tonnes (Mt) by both Safras and Agroconsult, down roughly 7-10pc on the year, with safrinha production slipping to around 99-112Mt depending on the source.

On the export side, South Korean NOFI tendered for up to 207,000t feed corn.

Soybeans were the standout, with July surging 15.75c as the market priced in optimism around potential Chinese purchases out of the Trump-Xi summit.

Brazil’s April soybean exports hit a new monthly record of 16.75Mt, up nearly 10pc year-on-year, and Brazilian beans remain the clear demand destination of choice regardless of any goodwill purchasing China might direct toward the US.

Crush margins softened on the bean rally, with July crush finishing down 12.25c at 312.75.

Canola found support from the soy complex and European rapeseed, with ICE July canola up around C$5.80/t, continuing to test its 50-day moving average with fund longs still largely intact.

Macro: AUD 0.7246 | Dow +12.19 | Crude +0.61

Markets spent much of Friday in a holding pattern waiting on Iran’s response to the latest US peace proposal, which remained outstanding at the close. The proposal calls on Iran to reopen the Strait of Hormuz in exchange for the US lifting its port blockade over the following month, with Trump warning of a return to “Project Freedom Plus” if terms aren’t accepted.

Clashes in the Strait continued over the week, with US forces striking two Iranian oil tankers attempting to break the blockade.

Brent crude settled around $101 a barrel, notching a weekly decline of around 6pc despite the ongoing disruption — the Hormuz closure remains a significant factor in world food prices, with the FAO reporting vegetable oils at their highest in more than three years.

Iran’s foreign minister confirmed the proposal was under review, while US Secretary of State Rubio met Qatari counterparts Saturday as Qatar continued its mediation role.

On the Ukraine front, Trump brokered a three-day ceasefire through May 11, allowing Putin to hold a subdued Victory Day parade in Moscow — notably without heavy military hardware for the first time since 2007.

A US trade court also dealt a further blow to Trump’s tariff architecture, ruling the 10pc temporary global duties unjustified under a 1970s trade law, though the order was limited to two private importers and the State of Washington pending any appeal.

The AUD was flat on the day, equities barely moved, and the broader macro tone heading into the weekend was one of cautious anticipation rather than conviction.

Local: WA bids were steady to slightly firmer, with canola A$795/t current season and $828 new crop, wheat $342 and $355, and barley $342 and $330 FIS Albany.

In the east, bids were softer to finish the week. Canola was $765 current season and $802 new crop, wheat $340 and $363, and barley $316 and $328 track Geelong.

Northern wheat markets are starting to falter as consumers extend coverage and growers step into the falling market, with nearby wheat now bid in the low $420s. Barley, however, remains firmer and harder to buy, with bids in the mid $430s.

Looking ahead, moisture is forecast to push down from the north over the next week, with 25–50mm possible through eastern SA and 15–25mm across most of Vic and NSW. Fingers crossed it lands — if it does, it would be close to a perfect start for most of SA and Vic.

HAVE YOUR SAY