Weather: Small changes, the Euro model is starting to build some moisture into the southern belt in Russia, however, both models have temps falling to minus 10°C. The GFS model has removed some of the moisture for Argy – still getting rain however.

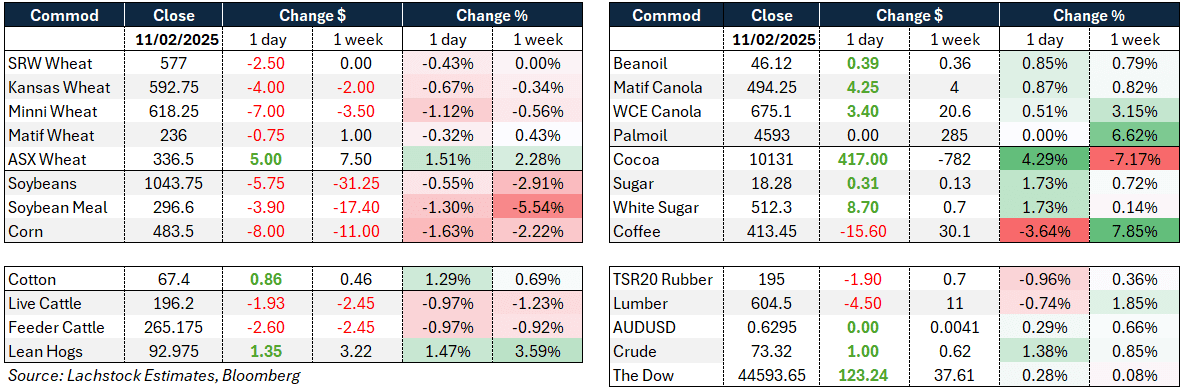

Markets: Ho Hum – the reaction to the WASDE report was pretty boring with most numbers coming in pretty close to the average guess. Swings and roundabouts. The USDA did take the sword to Chinese demand which is still the wet blanket on global values.

Australian Day ahead: USDA is now behind us. The fact they took 2.5 million tonnes (Mt) out of wheat imports certainly isn’t friendly to Australia given we were set to be their biggest supplier however, you need to dig into the numbers. The USDA bucket of “South East Asia” actually saw a small import increase, from 30.05Mt to 30.25Mt – so other countries are offsetting the China cuts. AUD firmer, suggest we are slightly lower to sideways today.

Offshore

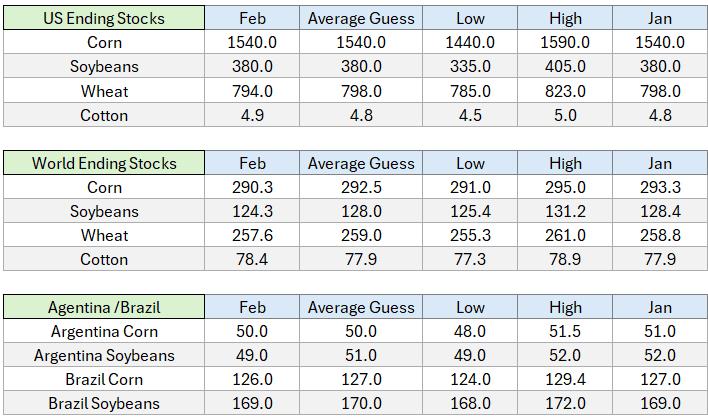

USDA WASDE

- The 2024/25 U.S. wheat outlook projects slightly higher domestic use, with food use rising to 970 million bushels. Ending stocks decrease slightly to 794 million bushels, though still 14pc higher than last year. The season-average farm price remains at US$5.55 per bushel. Globally, wheat supplies increase slightly, reaching 1,061.3Mt, mainly due to higher production in Kazakhstan and Argentina. Consumption rises to 803.7Mt, driven by increased feed use in the EU, Kazakhstan, Thailand, and Ukraine. However, global trade declines to 209Mt, with export reductions for the EU, Mexico, Russia, Turkey, and Ukraine. China’s imports drop significantly to 8Mt, their lowest in five years. Global wheat ending stocks fall to 257.6Mt, primarily due to reductions in China, partially offset by increases in Russia, Kazakhstan, and Ukraine.

- The 2024/25 U.S. corn supply and use outlook remains unchanged from last month, but the season-average farm price is raised by 10 cents to $4.35 per bushel. Globally, coarse grain production is reduced by 1.8Mt to 1.492 billion tons. Foreign corn production is lower, with cuts for Argentina and Brazil. Argentina’s reduction is due to heat and dryness in January and early February, affecting early-planted corn yields. Brazil’s forecast is lowered due to slow second-crop planting in the Center-West, leading to lower yield expectations. Global trade sees reductions in corn exports from Brazil, Ukraine, and South Africa, while China’s corn imports are lowered, and imports increase for Vietnam and Chile. Foreign corn ending stocks are also reduced, particularly for China. Global corn ending stocks drop by 3Mt to 290.3Mt.

- The 2024/25 US soybean outlook remains unchanged, with the season-average price lowered by 10 cents to $10.10 per bushel. Soybean meal and oil prices remain at $310 per short ton and 43 cents per pound, respectively. Globally, soybean production declines due to heat and dryness in Argentina and Paraguay, while Brazil’s production remains steady at 169Mt. Favourable weather in Brazil’s centre-west boosts prospects, but dry conditions in the south impact yields. Global soybean crush increases, driven by higher crushing in Brazil due to strong biofuel demand and soybean meal exports. However, Paraguay’s crush and meal exports decline due to lower supplies. With minimal changes in global soybean exports, ending stocks fall by 4Mt to 124.3Mt, primarily due to reductions in Argentina and Brazil.

Lachstock summary of select data WASDE February report (left column) versus January (right column). Million tonnes. Click expand.

Australia

WA canola bids were unchanged yesterday at around $850, wheat at $377, and barley at $343. New crop canola was bid at $800 and wheat at $390.

Canola bids were off in the east of the country, down around $5-$10 to be bid at $754. Wheat was down slightly, bid at $344, with barley at $314. New crop canola was bid at $735, with wheat at $353.

The ABS December numbers, which were released last week, were higher for wheat than line-ups had suggested for SA, Vic, and NSW. NSW showed the biggest variance, with around 454kmt of wheat leaving NSW—45kmt of this in containers—compared to the line-ups number of around 300kmt. The increase is welcome news given the work needed to move the big crop out of the state.

Feed grains continue to catch a bid as feed mills and end users try to extend their coverage levels, with SFW delivered to Geelong/Melbourne trading at around $355, with barley at $337.

HAVE YOUR SAY