Weather: The weather has arguably finally been priced in. This has been on the boil for a while, but the USDA has historically been slow to move. Not this time it would seem.

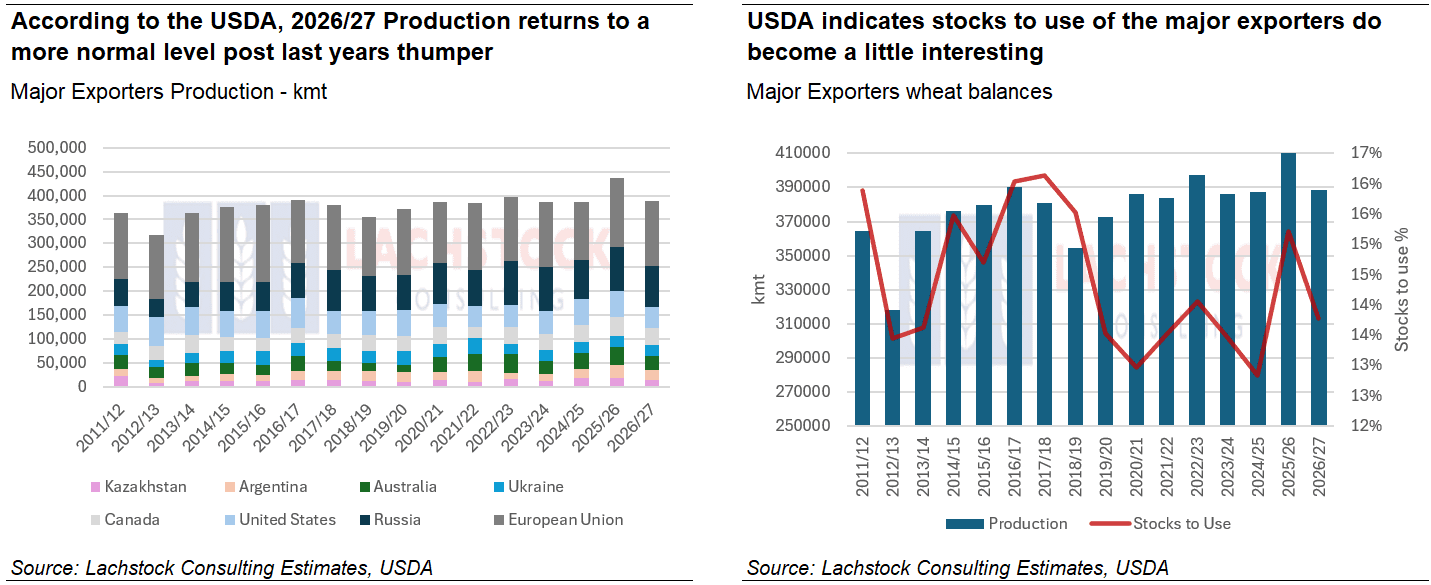

However, the rest of the global growing belt looks pretty good. The headline wheat production shift looks startling but, remember, last year was a thumper.

Markets

WASDE delivers. The cuts were meaningful for the US balance sheet. I caution not to get sucked into the global changes, not yet at least. The May report is the first crack at the global 2026 numbers so there will be more work done on these in the coming months but, from a headline perspective, it looks like more of a mean reversion after last years big production.

Day Ahead – Australia

It will be interesting today how the Aussie market reacts to the offshore fun and games – the US crop is probably now pricing itself out of the export path which, from an ending stocks perspective provides a bunch of relief.

Aussie relativity into Asia isn’t really influenced by the US markets however, so it will be interesting to see what the local trade does.

Global wheat: Chicago +45.00 (679.00), Kansas +45.00 (731.25), MATIF +7.75 (225.75)

Global wheat: Chicago +45.00 (679.00), Kansas +45.00 (731.25), MATIF +7.75 (225.75)

Wheat was the story of the day, with Chicago SRW and Kansas both finishing limit up 45 cents and MATIF spiking over 8 euros.

The catalyst was a WASDE that delivered a genuine shock on the HRW production figure, coming in at 514 million bushels against market expectations clustered around 575-600, with the trade’s official estimate sitting at 638.

SRW also missed, printing 301 vs expectations of 337.

The numbers reflected what the crop had been signalling for weeks — ten consecutive weeks of declining Kansas condition ratings, catastrophic conditions across Texas, Oklahoma and Nebraska, and a winter wheat abandonment rate of 32%.

Harvested area losses year-on-year were severe across the southern plains with Nebraska down 28%, Kansas 14.7%, Oklahoma 17.9% and Texas 26.1%, while yield declines were equally punishing.

The resulting US new crop carryout landed at 762 million bushels against trade ideas of 845.

On the world front, USDA pegged Australian production at 30 million tonnes, down from 36, EU at 136 million versus 145 previously, and Argentina at 21 million down from 28.

World wheat production for 2026/27 came in at 275 million metric tonnes, well below the 281 million the trade had anticipated.

Winter wheat conditions in the weekly Crop Progress showed just 28% of the crop rated good to excellent, down from 31% the prior week and described by StoneX as sitting between the two worst crops of the last decade.

With expanded limits of 70 cents in place tomorrow and Kansas, Chicago and MATIF spreads all firming, the path of least resistance remains higher while these supply clouds persist .

Other grains and oilseeds: Corn +4.75 (480.00), Soybeans +13.75 (1226.75), MATIF Canola +7.00 (522.00)

Corn finished up 4.75 cents but was largely a sideshow to the wheat drama, with its strength more attributable to China trade speculation than anything delivered by the WASDE.

A Bloomberg story during the session cited unnamed sources suggesting US corn has a real shot at landing in China’s shopping cart, and that narrative carried more weight than the report itself, which lifted old crop carryout by only 15 million bushels and put new crop ending stocks at 1.957 billion versus expectations of 1.942 billion.

World corn ending stocks were the more notable figure, coming in at 277.5 million tonnes against expectations of 291 million, with lower acres and elevated input costs continuing to weigh on the global balance sheet.

Some in the market are already working with a 180 yield versus USDA’s 183, and June acreage could trim a further 1-3 million acres, leaving some creative balance sheets as low as 1.6 billion on new crop carryout.

Soybeans gained on the back of a tighter-than-expected WASDE, with old crop carryout at 340 million bushels versus 349 expected and new crop at 310 versus 366, though large crush figures kept meal in the frame.

World bean ending stocks came in at 124.78 versus 126.50 expected.

The near-term direction in both corn and beans is less about balance sheets and more about what China does this week. Canola recovered well, with WCE July settling up 10.80 to 754.20 and MATIF canola adding 7.00 to 522, supported by a weaker Canadian dollar, firming soyoil and European rapeseed, and broader oilseed strength flowing from the WASDE.

USDA held Canadian canola production for 2026/27 unchanged at 22 million tonnes with exports rising 600,000 tonnes to 8.2 million.

Macro: AUD 0.7240, Dow +56.09 (49760.56), Crude +4.11 (102.18)

Crude added over four dollars on the session as geopolitical risk premiums stayed elevated, with reports emerging that Trump was considering resuming attacks on Iran adding to an already tense backdrop.

The Strait of Hormuz closure continues to generate what Bloomberg described as the biggest oil supply shock in modern history, and the upcoming Trump-Xi summit in Beijing has added another layer of complexity.

The US is seeking China’s help to reopen the strait given Beijing’s position as Iran’s largest oil buyer, while Xi arrives at the table from a position of relative confidence, having stabilised rare earth leverage and watched US tariff credibility eroded by a Supreme Court ruling.

Agricultural purchases — soybeans, beef and Boeing aircraft — are expected to feature prominently in talks, with Trump seeking voter-friendly wins ahead of November midterms at risk from elevated fuel prices.

The Dow added modestly, up 56 points.

Domestically, the Australian federal budget landed with a broad sweep of measures including $10.7 billion directed at fuel and fertiliser security in response to Iran supply disruptions, a $3.2 billion fuel reserve targeting 50 days of diesel and jet fuel cover, and $53 billion in additional defence spending over a decade.

Tax offsets for workers and permanent small business instant asset write-offs were among the headline fiscal measures, while negative gearing on residential property will be limited to new builds from July 2027 alongside a 30% minimum capital gains tax rate, with the government flagging this could shave around 2% off house price growth.

Local: What a night for wheat — all eyes will be on how local traders react today. We should see some upside domestically, although expect basis to weaken given the forecast rainfall through the east coast over the next week coupled with the heavy carryout situation.

Yesterday bids were firmer in the west for canola, with current season at $800 and new crop $840. Wheat was $347 and $365, while barley was $338 and $332 FIS Albany.

Through the east, canola was up $3 to $770 while new crop traded $810. Wheat was $340 and $368, with barley at $316 and $327 track Geelong.

HAVE YOUR SAY