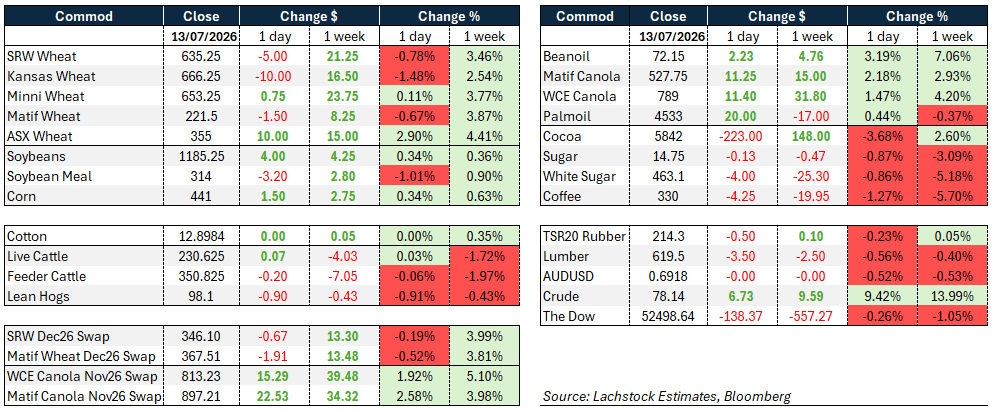

Weather:

Weather:

All of a sudden there is lots of market-driving activity. The heat wave currently hitting the north of the US is setting record temps in many areas. The core Corn Belt area under the ridge is expected to see a flash-drought develop over the next 1-2 weeks as it misses the surrounding rain, compounding heat-stress accumulation (stress degree days already 20+ units above average around Des Moines, nearing the ~140-unit threshold where corn yield loss begins).

One analysis flagged substantial, irreversible damage to spring row crops in Spain, the UK and France, with the 10-day EU/Black Sea forecast showing 92-101°F in France driving further rapid soil-moisture loss. Cooler/wetter conditions are seen possible after July 20, but too late to help corn potential meaningfully.

Markets

Take profit while it is there. Grains were all higher during the night session (southern hemisphere day session) as the military escalation in the Black Sea hit markets. Oddly, nothing really changed but profit taking stepped in. Makes sense given that, since this conflict began, war-led rallies fail. The market has learnt its lesson and profits will be taken and fundamentals reassessed.

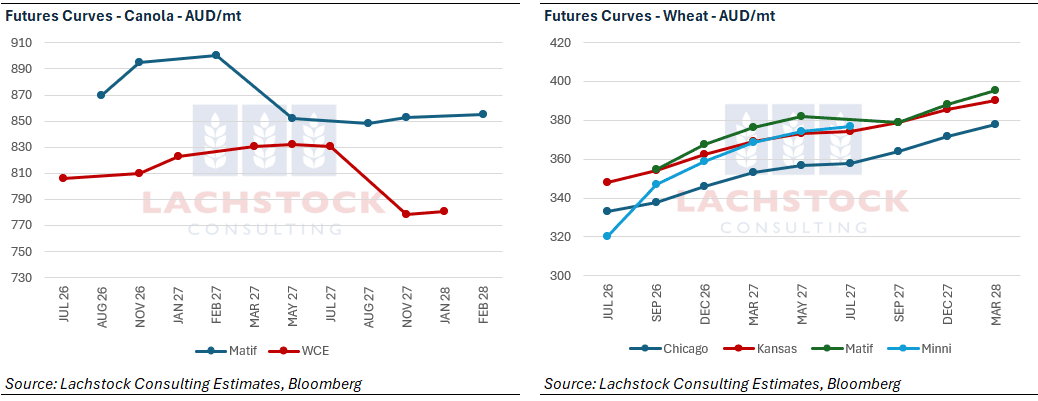

Canola was the one market that held the gains. A combination of the energy link and the reality that bio-mandates create a level of inelastic demand that don’t allow for crop shortfalls. The wet planting season in Canada has arguably reduced planted area and now it looks like extreme heat is pushing across the growing belt.

In the background, the El Niño fear is building globally. Nutriens’ Snodgrass is more and more compelled that it’s going to hit in the back half of this year and it’s going to be a belter. The Australian market is weighing up if there is enough moisture underneath the crop to get it through.

Day Ahead – Australia

Canola should continue to strengthen. Grains are more complicated. The NSW export path hasn’t performed which has increased stocks – meanwhile, the Asian consumptive market will be weighting up the risk associated with having a large percentage of its requirements penciled in from the Black Sea.

Slightly firmer across the board.

Wheat: Wheat gave back a slice of last week’s near-9% run as profit-taking dominated, Kansas leading the retreat while Minneapolis held firmest on northern heat and thin spring wheat prospects.

Wheat: Wheat gave back a slice of last week’s near-9% run as profit-taking dominated, Kansas leading the retreat while Minneapolis held firmest on northern heat and thin spring wheat prospects.

The pullback came despite a geopolitical backdrop that, if anything, deteriorated further: the Kerch Strait remains closed, Russian cash values pushed higher to $233-240 basis Novo, and Ukraine’s Azov shipping lanes stayed restricted after strikes on tankers and dry-bulk carriers on both sides.

Kernel’s (Ukrainian agribusiness) Chornomorsk terminal was knocked offline over the weekend, with roughly 45,000 tonnes of wheat and 9,000 tonnes of sunoil caught in the damage, even as Ukraine’s APK-Inform lifted its 2026 harvest forecast to 59.6mmt and wheat output to 22.4mmt on improved yields.

US wheat simply ran out of room after entering the session on a 60c bulge to Russian values. Demand chatter added some support: unconfirmed China interest in SRW and HRS surfaced Friday, plausible given persistent quality complaints out of China, while Jordan issued a 120k tonne milling tender for July 21.

Crop conditions were mixed but manageable — spring wheat gained a point to 58% good/excellent against a 5-year average of 53%, and winter harvest reached 67% versus 61% on average — while inspections of 374k ran slightly light and shipments remain 17% behind last year’s pace.

Net, the Azov closure and lack of any ceasefire progress in Iran argue against fading this leg of the rally too aggressively, even after Monday’s give-back.

Other grains and oilseeds: Beanoil was the standout, tracking diesel and crude’s spike higher and lifting the August crush 13.75c to 302, while meal sagged and dragged on soybeans’ net gain.

Corn firmed early but faded into the close as Midwest heat, already expected to persist another 5-7 days, drew fresh attention to yield risk — the market doesn’t need a disaster, just a marginal miss below 182 to tighten the balance sheet meaningfully.

Both crops nonetheless posted improved conditions after the close, corn up a point to 68% and beans up a point to 65%, against trade expectations for declines in both, and corn inspections at 1.54m ran at the high end of estimates, up 25% year-on-year.

China added another new-crop soybean purchase, 136,000 tonnes, continuing a pattern that so far looks confined to state-level buying rather than broader commercial demand pending tariff clarity.

Brazil’s supply picture firmed further: a Bloomberg survey points to this season’s soybean crop running about 600,000 tonnes above Conab’s June estimate, corn little changed near 140.4mmt, with Conab’s own update due July 14, and AgRural has Center-South winter corn harvest at 40% complete, in line with last year.

Canola was the other big mover, ICE WCE and Matif both gaining alongside the crude-driven strength in soyoil and rapeseed, compounded by wet Prairie conditions likely to cut harvested canola acreage by more than the usual seasonal one percent; China’s move to let private processors import Australian canola adds a supportive demand thread.

Palm oil edged up on the same soyoil/crude tailwind despite a softer weekly print. Livestock, cocoa and softs were the session’s laggards, with cocoa’s sharp daily drop the notable outlier against its firmer weekly trend.

Macro: Crude’s near-10% spike was the session’s defining move after Trump reinstated the US blockade on Iranian shipping through the Strait of Hormuz and demanded a 20% toll on all other cargo transiting the waterway, framing the US as the strait’s “guardian.” Strikes on Iran resumed for a third consecutive night, and Tehran’s response — Foreign Minister Araghchi calling Iran the strait’s permanent guardian and mocking the toll proposal — signals no near-term de-escalation.

The fee plan itself faces real hurdles: international law generally bars charging for transit passage, and the IMO has already pushed back, while shipping market contacts say they were blindsided and can’t yet price the risk.

Equities and bonds sold off on the news, with the Dow’s weekly loss outpacing its daily move as markets digest a conflict that looked closer to resolution just three weeks ago.

The Aussie dollar was essentially flat, underperforming the scale of the crude move and reflecting broader risk-off positioning rather than any local driver.

Local: In the west of the country bids were stronger across all commodities yesterday, but the main movers were GM canola and wheat. New crop bids in Albany PZ were $852 FIS for canola and $830 for GM, wheat $361, and barley $330.

Downs wheat is quoted at $375 for old crop and $395 for Jan +, Barley would be $380-385 of old crop but somewhat hard to extract, while new crop would be closer to $375 for Jan +. Sorghum old crop was quoted at $345-350 Downs.

HAVE YOUR SAY