Weather:

Weather:

A slightly more favourable weather backdrop today. Heat in the US persists but forecasts have eased from a temperature perspective.

Warm and wet in the west of the Canadian canola belt – pretty crazy start to their season but the consensus is planted area will be lowered slightly given the wet start.

Markets

The new game to play today is how to get wheat out of Russia through an alternative pathway. How efficient and how costly that is will shape FOB values in the near term. Romanian wheat has rallied US$11/t in 2 days as the reality of the Russian/Ukrainian shipping path closures bite.

Tight for the moment, but for reasons aside from production which makes markets hard to trade. War premium has a 100 percent efficiency and puking back out 5 minutes after they are priced in. The length and depth of this conflict makes this closure a little more significant in my opinion. It feels like we are escalating, particularly around infrastructure damage and energy assets.

Day Ahead – Australia

After a busy canola day it will be interesting to see what the local market does. Not sure anything has really changed aside from a futures profit taking round. Yes the Canadian forecast looks a little better but acreage cuts are probably yet to be fully baked in.

Every day the Black Sea is less accessible is a day the Asian consumer gets a little more nervous. Shipping costs and the spread from north to south are having a material impact on Australia’s competitiveness, especially into our traditional Asian consumer homes but this freight spread has a history of fixing itself over time.

Strait of Hormuz Tanker Vessel Crossings: Bloomberg

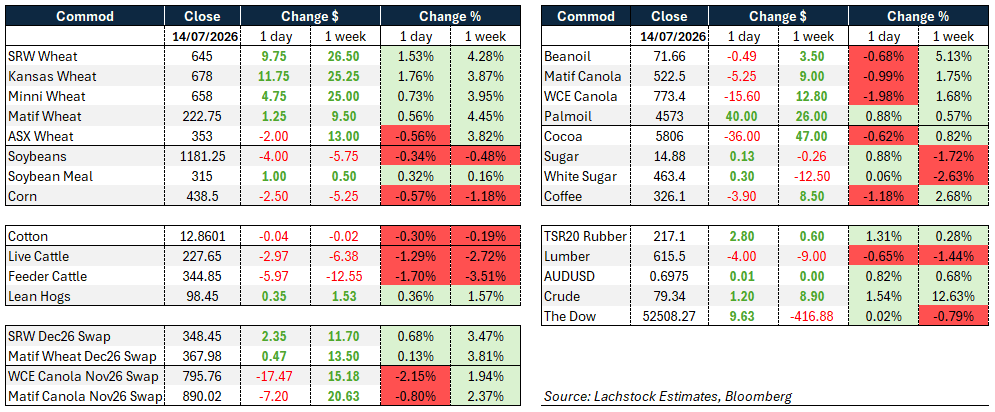

Wheat: BSEA risk is back in the driver’s seat.

Chicago led the complex higher, Kansas out in front on a firm winter-wheat spread structure, while the Minneapolis curve was mixed and spot vol pushed to 33.44pc from 32.57pc. Matif added another €1.75/t.

Russian cash traded US$233/t, but the more telling data point was Romanian wheat at $247/t, up $11/t in two sessions — a level nobody would have priced a week ago against a 90-million-tonnes Russian crop. That crop still exists; getting it out is the problem.

Ukraine and Russia are trading strikes on port infrastructure and bulk carriers, and Russia’s talk of routes bypassing Kerch runs into the same wall AgResource flagged: added truck and rail costs against constrained domestic fuel supply, plus Black Sea insurance that keeps climbing.

Saudi shorts were reported scrambling for cover and in no mood to test the market on words alone. This is typically where BSEA finds a seasonal low absent a genuine weather shock — the question now is simply whether the conflict escalates or eases from here, which will decide whether the remaining Chicago and Matif shorts stay or capitulate.

Continued focus on the shorter Brazilian wheat crop – historically a destination for Argy and HRW. Incremental HRW demand would test the US balance sheet further.

Other grains and oilseeds: Corn eased on cooler longer-range maps and a firmer overnight condition tick, though the Midwest is still baking under heat that isn’t expected to break until the weekend — and with model runs this erratic, nothing past five days deserves much confidence.

Both the 6-10 and 11-15 day outlooks turned cooler and drier, leaving only the western fringe exposed.

None of this changes the standing view that world corn doesn’t need a US disaster to get tight; anything near or below 181 million tonnes (Mt) starts to bite.

Brazil’s ethanol blend hike keeps absorbing domestic corn, reinforcing the export-share trend the US has been riding, and Conab lifted Brazil corn to 141.73Mt from 140.46Mt.

EU Nov maize closed at its high for the move, underscoring how tight Europe already is even as the US outlook loosens.

Beans sold off modestly on better-than-expected conditions and cooling temperatures, with front months down 3.75-4 cents.

Products were quiet — meal firmer, oil off 42 points, August crush steady at 302.

Some tried linking the Iran ceasefire collapse to a China pullback on US bean purchases; nothing confirms that read, and the more reliable drivers remain Chinese demand pace and forward weather.

Conab raised Brazil’s soybean crop to a record 180.57Mt, up 5.3pc year-on-year, on larger area and favourable weather.

Canola gave back all of Monday’s gains and more on a classic Turnaround Tuesday, pressured by weakness in Chicago beans and European rapeseed; firmer palm oil and a modest crude gain limited the damage.

The break in the Prairie heatwave removed a supportive prop, and a stronger loonie — 71.07 US cents versus Monday’s 70.70 — added further drag, even as November canola held above its major moving averages.

Separately, China is widening access to Australian canola beyond Cofco to private crushers under a trial permit scheme, a step toward formally reopening a trade largely frozen since 2020. It follows revised phytosanitary rules and comes alongside mended China-Canada relations and resumed Chinese buying of US beans — collectively broadening China’s oilseed sourcing just as Black Sea and Hormuz risk keeps a bid under the vegetable oil complex more broadly.

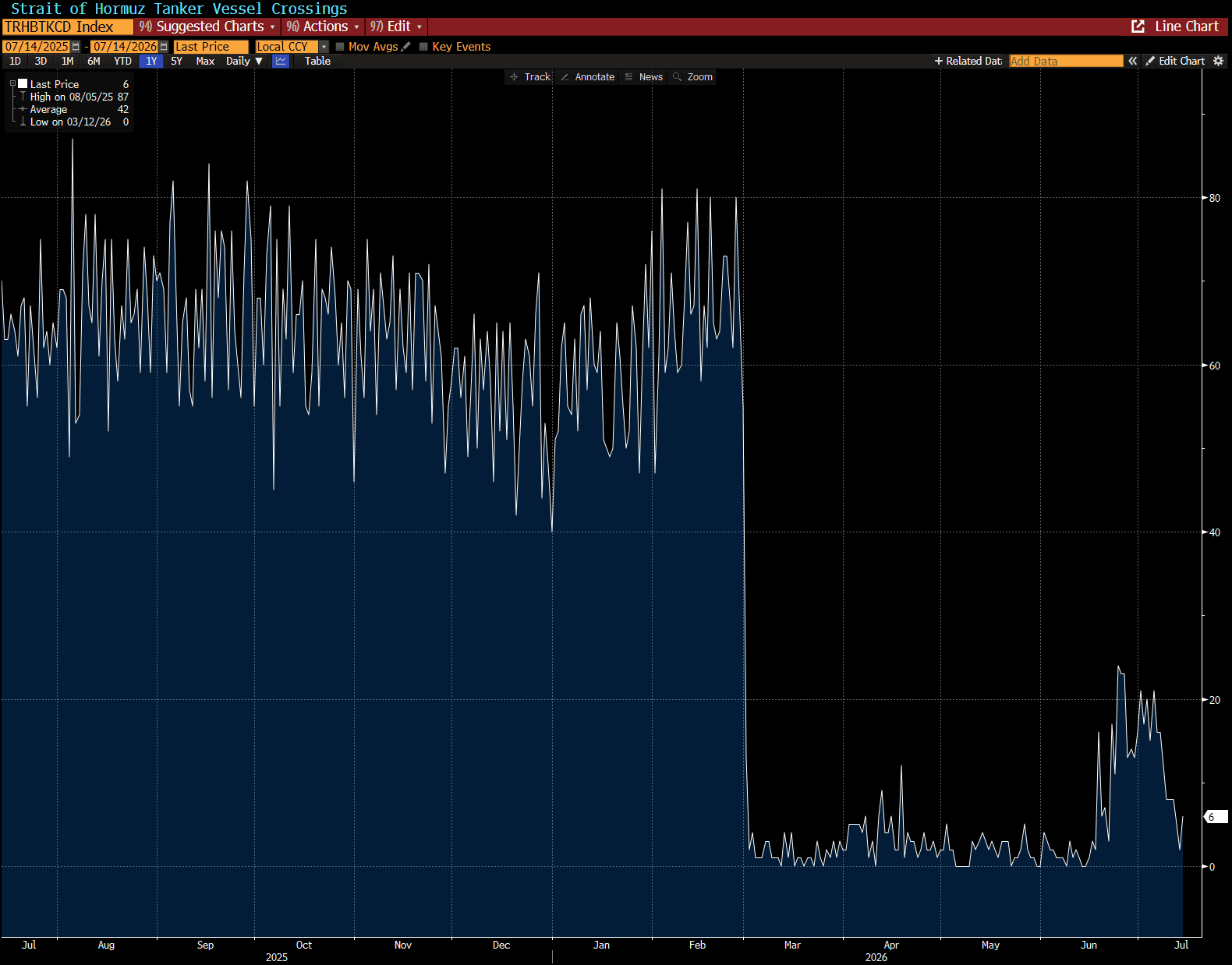

Macro: Crude carries the macro story this week, up nearly 13pc as the Hormuz standoff escalates rather than resolves.

Trump dropped his proposed 20pc transit fee after Gulf allies pushed back, replacing it with unspecified investment pledges — but in the same breath the US restarted its naval blockade of Iranian shipping and launched fresh strikes, with Trump threatening to extend attacks to bridges and power infrastructure next week absent negotiation.

Brent settled near $84.73, its highest in about a month.

The rapid reversal on the fee fits the pattern traders have tagged Trump with before, but the underlying military escalation is what’s being priced, not the policy flip-flop.

The Dow is essentially flat on the day but down on the week, reflecting the broader unease the energy and grain markets are also carrying.

Local: In the west of the country bids were significantly higher on canola again, wheat was back A$3-4/t and barley bids were unchanged. New crop bids in Albany PZ were $873 FIS for canola and $842 for GM, wheat $358, and barley $330.

Here one day, gone the next. Rainfall for the back end of the forecast has pulled back significantly. The northern market liquidity in tied to the next rain event and forecasts will be traded given the continued focus on the so-called “Super El Nino”.

HAVE YOUR SAY