Weather: Amazing weekly totals throughout Geraldton along with a chunk of the Australian growing belt.

Weather: Amazing weekly totals throughout Geraldton along with a chunk of the Australian growing belt.

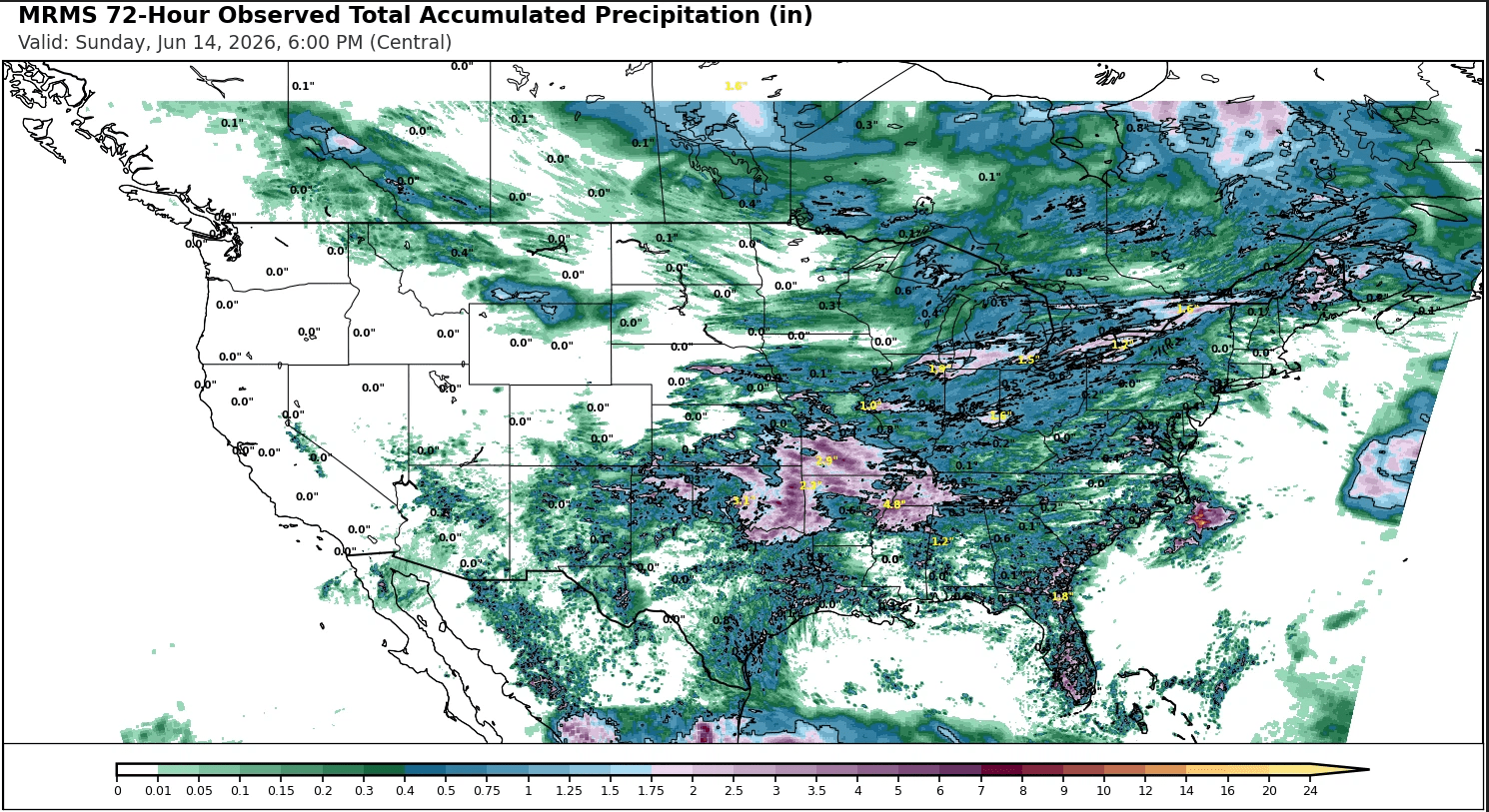

Parts of Oklahoma got around 3 inches over the weekend with 1-2 inches on the way. As per the last USDA update, 44% of that crop has been harvested – not ideal.

Another heat wave for Europe with France set to get over 35 degrees, très chaud. Can’t imagine this is good given harvest is still around 4 weeks away so i imagine they are in headfill in many parts of the country.

Markets

When the war is over, got to get away / Pack my bag to no place, in no time, no day.

This time for sure. Donald has indicated that the deal will be inked on Friday in Switzerland. interesting timing given western central banks grapple with energy linked inflation, particularly the RBA who meet this week. NAB business survey has been bleeding, housing also on the nose. However, there is still an issue that needs dealing with. The Aug meeting is probably more significant given they will reassess their targets. Regardless, the market is looking for rates to remain unchanged.

Energy markets have come off in response to the agreement – no big surprise. I have been banging on about the fact our retail diesel price hasn’t been reflecting the fact we have cut out 20% of the worlds crude/refined product flow – I saw an interesting article suggesting that as much as 7mbbl/day has been flowing out of the Strait with vessels turning off their transponders and the US navy has been helping these boats get out.

Day Ahead – Australia

We have ticked off some of the key data points that could be market driving with little to no fanfare.

will be interesting to see how Ag futures react to the cease fire – at time of writing US futures are down 4-5usc/bu.

RBA should leave rates unchanged but, as per the last few updates, I’m not sure the AUD cares.

US recorded rainfall

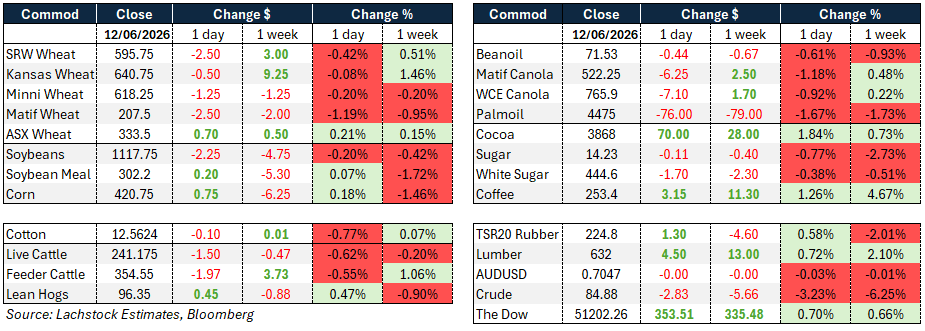

Wheat: Wheat markets struggled to hold onto intraday gains on Friday, with Chicago SRW shedding 2.25 cents, Kansas City easing fractionally, and MATIF September losing €2.25/t to close at €207.50.

The pattern was familiar — markets found buyers early in the session before fading sharply into the close, finishing 8 to 10 cents off their intraday highs.

The US HRW crop remains historically small, with USDA confirming the smallest Hard Red Winter harvest since 1957, though this is not new information and the market has largely priced it in.

Chicago SRW carryout remains tight near 100 million bushels and KC stocks are around 150 million bushels tighter year-on-year, which is keeping the short side uncomfortable in US wheat.

In Paris, French soft wheat crop conditions improved one point to 77% good-to-excellent as of June 8, recovering from two consecutive weeks of declines following the May heatwave.

European weather forecasts have shifted hotter for next week, though MATIF traded with little conviction around French crop concerns.

Rumours of Chinese wheat inquiries circulated without confirmation and the market’s muted response suggests traders are sceptical.

Russian wheat continued to ease, down around $2 to $239/t.

In Turkey, domestic production is forecast 5-6 million tonnes above last year, which will weigh on import demand.

Egypt is tracking toward a record domestic procurement season, having already purchased 4.6 million tonnes of the 5 million tonne target.

Western Australia received welcome rainfall after a dry May, with GIWA describing the state as set up for a reasonable year assuming average rainfall persists, though wheat area estimates were trimmed to 3.68 million hectares from 3.75 million as growers shifted toward canola and barley.

Cool and wet forecasts across the US Midwest heading into the weekend raised some disease concerns for SRW wheat by late June.

On positioning, managed money sold 18,000 contracts of Chicago wheat and 22,000 of KC in the latest COT reporting period, pushing Chicago to around 50% of its record gross short and leaving KC with more sellers than buyers for the first time in some time.

Other grains and oilseeds: Corn and soybeans both had the look of markets that wanted to rally but couldn’t hold it together. Corn traded 4 to 5 cents higher at its peak before July futures finished up just 1 cent, with December barely clinging to gains.

The fundamental backdrop remains a tug of war between ample Northern Hemisphere moisture — which is constructive for the crop but has removed weather premium — and potential Chinese demand if the Trump-Xi relationship yields anything concrete.

Paraguayan and Indian production upgrades in the latest WASDE added supply without materially moving markets, and further Brazilian corn supply continues to be absorbed by insatiable domestic demand.

Argentina retains the cheapest overall FOB title globally, though PNW is currently the cheapest landed option into Asia.

Chinese feed demand for corn is being pressured by rising imports of alternative grains, with sorghum and barley shipments rising significantly according to CASDE.

South Korea purchased between 55,000 and 68,000 tonnes of feed corn in a tender on Friday from optional origins.

Managed money added a record 120,000 contracts to their corn gross short in the latest COT period, a significant repositioning that has levelled the playing field heading into a weather-sensitive Northern Hemisphere growing season.

Soybeans were similarly unable to close in positive territory, with July losing 1.5 cents and November off 2 cents.

Soyoil weighed on crush margins, with July bean oil down 17 points, leaving the July crush down 1.25 cents to 366.50.

The market’s narrative is simple — beans need China, and that demand has not yet materialised in size.

May NOPA crush is due Monday and is expected at 216.4 million bushels, up 12.3% year-on-year.

Managed money sold 65,000 soybeans, 25,000 bean oil, and 75,000 meal contracts in the latest reporting period.

MATIF canola shed €6.25 on the week, consistent with softness across the oilseed complex.

Malaysian palm oil was effectively unchanged on Friday, consolidating a fourth consecutive week of gains as El Niño weather uncertainty and Indonesian export policy shifts continue to support near-term sentiment. Palm oil buyers are locking in Indonesian supplies ahead of potential disruption from the country’s new one-gate export policy.

Macro: The dominant macro development over the weekend was the announcement of a US-Iran peace framework that will see the Strait of Hormuz reopen upon signing in Switzerland on Friday.

The deal was first announced by Pakistani Prime Minister Shehbaz Sharif before being confirmed by President Trump and Iranian state media, though the full text has not been released.

Trump confirmed the US naval blockade on Iranian ports will be lifted and that the Strait will reopen once the memorandum of understanding is signed, with a 60-day negotiation period expected to follow toward a formal end to the conflict.

Oil fell sharply in response, with Brent dropping more than 4% toward $83/bbl and WTI losing 4.4% to around $81/bbl, extending losses after crude had already closed last week at its lowest in more than three months.

The Strait had been effectively closed since the war began in February, with roughly 7 million barrels per day — around half pre-war volumes — flowing through.

Equity futures responded positively, with S&P 500 futures up 0.7-0.8% in early Asian trade, though analysts cautioned that optimism should be tempered until the deal is formally signed. Gold rose 1.5% to $4,284/oz.

The Australian dollar edged higher to $0.7072 on risk-on sentiment. Bitcoin climbed over 2.5%. Attention this week shifts to the Federal Reserve, which meets Wednesday for the first time under new chair Kevin Warsh.

Markets will be watching the dot-plot closely for signals on the inflation outlook and whether Warsh aligns with the majority for a hold or dissents.

The Bank of Japan is also expected to raise rates to 1% — a level not seen since 1995 — while the RBA is anticipated to hold on Tuesday.

The World Bank cut its 2026 global growth forecast to 2.5%, warning of a potential further slowdown to 1.3% if energy supply disruptions prove more severe.

The EU proposed a €540 million aid package for farmers facing elevated fertiliser costs linked to the war, and President Trump separately indicated he is considering assistance for US farmers facing similar pressures.

Local markets: The week ended steady in the west with canola bid $820 current season and A$860/t new crop, wheat was $346 and $356, while barley was $326 and $327 FIS Albany.

In the east, canola was $775 current season and $815 new crop, wheat was $332 and $348, and barley was $312 and $315 track Geelong. – Protein demand remains evident through eastern wheat markets, with H1 wheat bid around $385 delivered port on the back of solid export container demand.

After 5–15mm fell across parts of SA and Victoria over the weekend, forecasts are calling for another 25–50mm this week, continuing an already strong start to the season for most southern cropping regions.

HAVE YOUR SAY