Weather: Rainfall forecast for Texas is going up – now, some of the southern belt is looking at 4+ inches in the next 10 days; just nuts.

That pattern looks to push into the SRW areas which should be a net positive for production.

Note that it is getting pretty warm in France over the next week, but I don’t think its a crop altering issue.

Rainfall forecast hanging in there for NNSW and Qld.

Markets

Risk off last night – not really any fundamental change, just bulls need constant feeding.

Donald/Xi meeting very much mixed. Xi put a shot across Donald’s bow – indicating that mishandling Taiwan could spark conflict. The US has a sale on the books for US$14b worth of US arms to Taiwan. This was the bitter aftertaste in an otherwise constructive meeting.

Not a skeptic, just calling it as I see it – I did note that China said it may end up purchasing some US crude if the strait remains closed.

Day Ahead – Australia

Down day offshore, Eric Snodgrass sees good falls in the short term, and explores the idea that a late El Niño may not be as impactful to winter crop production.

Softer today.

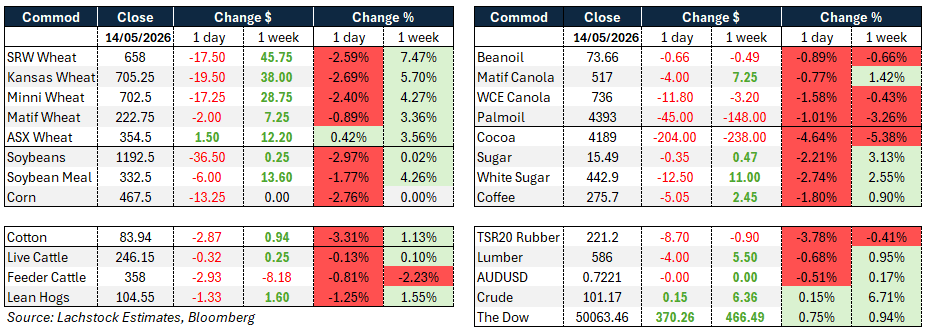

Global wheat: Chicago -17.50c, Kansas -19.50c, MATIF -€2.00

Global wheat: Chicago -17.50c, Kansas -19.50c, MATIF -€2.00

Wheat markets sold off sharply as the first day of the Trump-Xi summit in Beijing produced no concrete agricultural purchase commitments, disappointing traders who had positioned for a positive headline.

Chicago fell 17.5c, Kansas 19.5c, and MATIF eased €2.00, with implied volatility in Chicago pulling back to 34.56 percent from 35.78pc.

The mood was one of relief-selling as the market had already absorbed the key crop tour data — the Wheat Quality Council pegged the Kansas crop at 218 million bushels, broadly in line with the USDA’s 214.6Mbu.

Southwestern Kansas yields were estimated at 39.3 bpa, well below last year’s 53.3 bpa and the five-year average of 43.4 bpa.

Export sales of 134k tonnes old crop came in above the 100k expected, with Indonesia taking 50k HRW a notable highlight, though new crop at 221k was marginally below the 225k expected. Russian cash edged up 50c to $241.

Argentine new crop wheat estimates are pointing to reduced acreage relative to last season’s 28 million tonnes (Mt) harvest, with Rosario at 18–19Mt and BAGE at 21.3Mt.

EXPANA put EU 2026 soft wheat production at 128.8Mt, up slightly from prior estimates but still around 6pc below the 2025 crop.

The Russia-Ukraine conflict remained in focus with reports of the largest aerial drone and missile assault on Ukraine since the war began, though the market largely set this aside given the broader risk-off tone driven by China disappointment.

Other grains and oilseeds: Corn-13.25c, Soybeans -36.50c, MATIF Canola -C$11.80

Grains and oilseeds were broadly shellacked on the day as the Trump-Xi summit failed to deliver the agricultural trade news the market had priced in.

Corn fell 13.25c with December off 11.5c, as weekly export sales of 685k tonnes came in well short of the 1.45 million tonne trade expectation.

CONAB nudged its Brazilian corn estimate higher to 140.17Mt from 139.57Mt, with the safrinha crop holding near last month at 108.46Mt versus 109.12Mt previously.

Argentina’s corn harvest remains slow at just 32pc complete. The NOAA’s Climate Prediction Center is now assessing an 82pc chance of El Niño emerging this month or in June, with a 96pc probability it persists through next winter — a development that could bring above-average rainfall to the US Corn Belt and add to what is already shaping up as a strong production year.

Soybeans bore the brunt of the selling with the July contract down 36.5c and November off 24.25c. A daily sale of 252k tonnes to unknown buyers — 120k old crop and 132k new — was noted but was too small relative to market expectations to provide much support.

Weekly soybean export sales of 102k tonnes hit a new marketing year low against expectations of 250k.

CONAB raised its Brazilian soybean estimate to 180.46Mt from 179.15Mt, while Rosario lifted its Argentine estimate to 50Mt.

Argentina’s harvest is now 57.9pc complete. Canola followed soybeans lower, with the July ICE contract off C$11.80, with European rapeseed and soyoil also weaker on the day.

The US House passed legislation permitting year-round E15 sales, though traders remain sceptical the bill can clear the Senate.

Macro: AUD flat, Dow +370.26, Crude +0.15

The macro backdrop was mixed. The Dow posted a solid gain of 370 points and crude edged marginally higher by 15 cents, while the AUD was effectively unchanged on the day.

The dominant theme remained the Trump-Xi summit, which produced broad language around agricultural trade, energy flows, and fentanyl but no binding commitments.

A White House readout noted Trump and Xi agreed the Strait of Hormuz must remain open for the free flow of energy, with Xi reportedly expressing interest in purchasing more US oil to reduce reliance on the strait — though Chinese state media made no mention of oil purchases.

Trump was reported to have raised agricultural purchase commitments and fentanyl precursor flows during the more than two hours of talks.

Putin is expected to visit China very soon according to the Kremlin. Iran’s foreign minister used a BRICS foreign ministers meeting in New Delhi to call for condemnation of what he described as illegal US and Israeli actions, underscoring ongoing tensions in the Middle East that continue to carry latent implications for energy pricing.

Local: WA bids were softer yesterday with canola bid A$800/t and new crop $840, wheat $350 and $370, barley was $338 and $333 FIS Albany.

In the east bids were a little softer with canola $775 while new crop was $813, wheat was $345 and $375, barley $318 and $325 track Geelong.

Delivered markets have softened around $10 over the last two weeks through southern markets, with Hanwood now bid $360 current season and $370 new crop, Murray Bridge $348 and $360, and Geelong $368 and $378.

The softer tone through delivered markets suggests nearby domestic consumers are becoming more comfortable with coverage, while improved rainfall forecasts and steady grower selling continue to weigh on basis through southern regions.

HAVE YOUR SAY