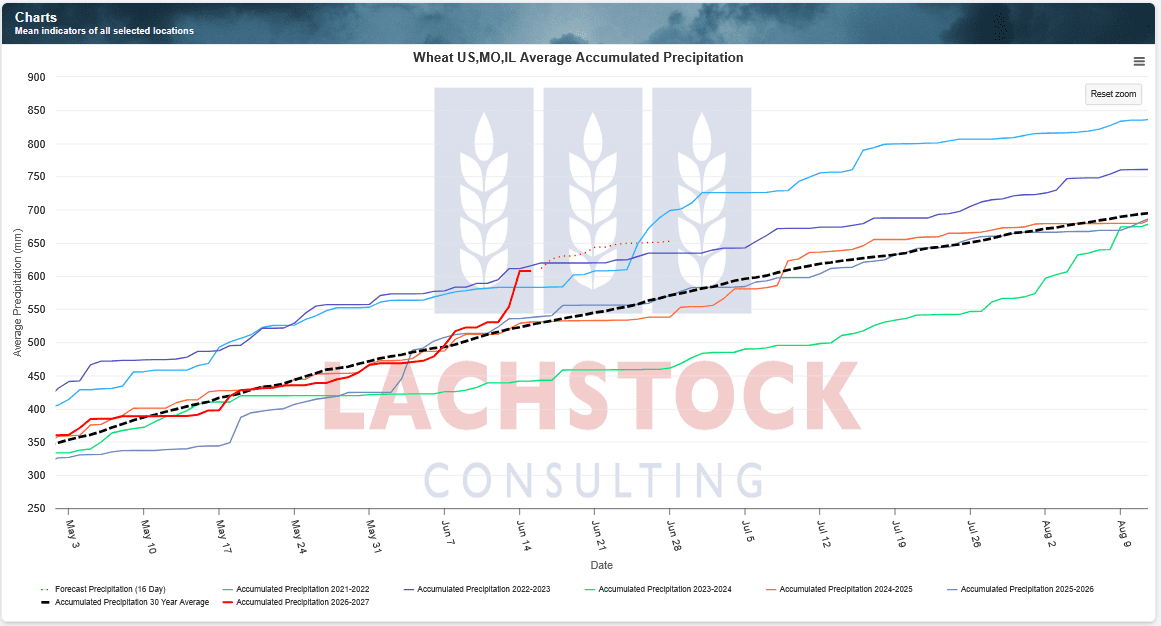

Weather: Hot in France, wet through the SRW belt – probably the two main weather events at the moment.

Weather: Hot in France, wet through the SRW belt – probably the two main weather events at the moment.

We are keeping an eye on the Indian monsoon – early days, only 2 weeks in but the all important Uttar Pradesh which accounts for around 35 percent of India’s wheat production is already building deficits.

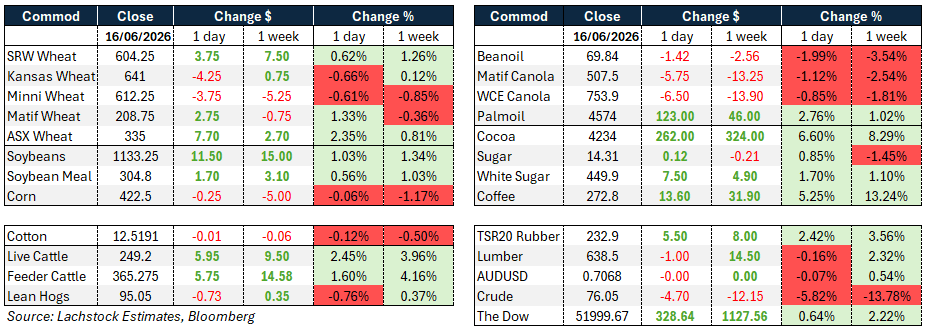

Markets

Well – I have to admit feeling a little confused today. The details of the cease fire are still bleeding out but, from what I have seen so far, is just strange. There is unclear reports that Iran would be able to sell oil as soon as the agreement is inked, additionally, they can access a $300 billion fund set up by the US and a bunch of Persian Gulf States designed so Iran can rebuild.

Wheat reflected to two areas of concerns – SRW is going to get exceptionally wet, and the heat in France is a concern – so some risk premium has been built in. The EU risk is arguably reduced given how advanced that crop is but SRW is in the gun.

Day Ahead – Australia

More of the same – it feels like we have growing confidence in a massive Russian crop – although FOB markets are still to reflect this. However, the need for sustained risk premium underlined by the BOM reminding us that El Nino is set to hit during spring is a balancing item.

Status quo.

Wheat: The dominant theme was weather risk to SRW at the worst possible time. A parade of storm systems is expected through Midwest and southern SRW regions just as harvest approaches, raising fears around quality losses and potential yield washouts.

Wheat: The dominant theme was weather risk to SRW at the worst possible time. A parade of storm systems is expected through Midwest and southern SRW regions just as harvest approaches, raising fears around quality losses and potential yield washouts.

Chicago pushed higher on this alone even as KC and Minneapolis underperformed, the KC-Chicago spread sold off aggressively, calendar spreads in Chicago firmed, and implied vol in WN rose to 25.78pc from 24.83pc.

In Europe, Matif gained on heat building over southwest Europe — supportive for quality if short-lived, though concerns are growing the ridge moves east into Ukraine.

Russian cash was unchanged at US$238/t fob. Ukraine’s 2026 wheat crop is forecast at 23.5-24 million tonnes (Mt), up from ~23Mt last year, while Russia’s seaborne exports surged 71.7pc y/y in May, bringing the season total to 49.8Mt, up 10.5pc y/y.

EU soft wheat exports reached 22.4Mt for the season, ahead of last year’s pace.

Algeria tendered for 50kt August shipment.

Traders have contracted up to 700kt Ukrainian barley from the 2026 harvest.

A US-Iran deal reopening the Strait of Hormuz could trigger a rush of grain imports into Persian Gulf nations that have relied on longer trade routes for months.

Australia’s Bureau of Meteorology warned a strong El Nino has formed and could intensify in the second half of 2026.

Other grains and oilseeds: The session’s headline was a dramatic move in soybeans on Chinese buying rumours. SN was down 9c into the midday pause before tagging 1136 within 15 minutes of reopening — a 27c swing — on reports China was seeking US bean offers for an Oct/March slot.

Some cargos may have traded before Brazilian basis softened and China reportedly returned there.

SN finished up 10.75c, meal gained $2.80, bean oil lost 145 points, and July crush fell 20.5c to 342.75c.

The Chinese demand narrative spilled into corn and wheat, though corn faded after tagging 421c and settled down 1.75c.

Weather for corn remains broadly supportive with USDA crop progress showing 68pc of corn and 66pc of soybeans rated good/excellent.

A derecho (fast moving, widespread wind storm that has the potential to flatten crops) risk in Illinois and Indiana Wednesday is worth watching, as is the prospect of a drawn-out SRW harvest cutting double-crop soybean acres.

ICE canola fell further toward its 50-day moving average, weighed by crude weakness and lower soybean oil.

Palm oil was the exception, rising on anticipation of Indonesia’s B50 biodiesel mandate.

French corn plantings are down 19pc y/y and 13pc below the five-year average, with farmers shifting to sunflower and rapeseed.

India’s soybean acreage is expected to rise as four-year-high prices and El Nino concerns push farmers from water-intensive crops.

Macro: Crude extended Monday’s sharp losses on the prospect of Iranian oil returning to market under the US-Iran framework agreement due for signing Friday.

Trump confirmed Iran will be permitted to immediately begin selling oil under the MOU, and a $300 billion private investment fund was outlined with more than half already committed. Significant uncertainty remains however.

US intelligence has assessed Iran now has de facto control of the Strait of Hormuz and could close it again at will, retaining missiles, drones, fast boats and mine-laying capability.

Shipping officials expect traffic to remain at a trickle for weeks or months regardless of any agreement.

Iran is also reportedly holding in reserve the option of directing the Houthis to close Bab-el-Mandeb (Red Sea) should nuclear negotiations collapse.

The Fed holds rates Wednesday in Kevin Warsh’s first FOMC meeting as chair, with several officials flagging potential rate hikes and wanting to remove language suggesting the next move is a cut.

Markets price a 60pc odds of a hike by December, and fresh dot plots are expected to show higher inflation forecasts with cuts pushed back to 2027.

ADP showed a fourth consecutive week of slowing private payroll growth, with the four-week moving average falling to 25.5k.

China’s economy showed increasing divergence in May with retail sales falling for the first time in over three years while industrial output accelerated.

US-Mexico trade talks resumed in Washington focused on agriculture and energy.

Local markets: Through the west of the country canola was softer bid A$800/t and new crop was $840, wheat was $340 and $352, barley $325 and $323 FIS Albany.

In the east of the country canola was back $10 to $755 and new crop was $790, wheat was $330 and $345, barley was $306 and $315 track Geelong.

Lentil bids remain around $640 delivered ports, with reports of a distressed cargo of Canadian lentils sold into Bangladesh at US$20/t under the market weighing on local values yesterday.

Australia has exhausted its 2026 China beef quota of 205kt, meaning beef entering China from 19 June will face a 55pc tariff for the remainder of the year, likely redirecting volumes into alternative export markets and reducing Chinese demand significantly.

HAVE YOUR SAY