Weather: Too much of a good thing – spring wheat areas of Russia have been belted with rain, and more is on the way. Given spring wheat is around 30 percent of total wheat production, this has the potential to skew the balance sheet a little. Go time for NNSW and Qld – BOM still reckons the rain is coming. Some rain in the driest part of the Brazilian corn belt.

Markets: It’s hard to know what’s what at the moment. Despite Donald saying he had an awesome time in China and the meeting was grouse, he failed to come back with a trade deal. More talk about ags being included but without confirmation, the market has almost given up. The other omission from the China trip was a resolution on the Iran conflict; there was some thought that Xi was going to force Donalds hand. Wheat markets were higher on the week, but that misses the fun and games post the WASDE. The market is telling us that low $6/bu is where the value is.

Day ahead – Australia: More of the same – east coast waiting on rain, west coast focused on the lack of export interest. New-crop basis is actually pretty good, particularly in the West despite the current lack of demand.

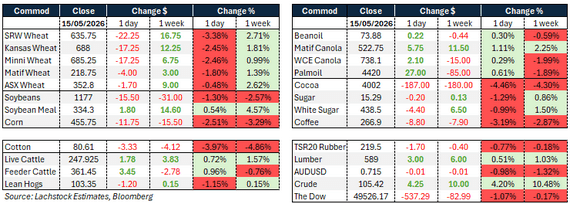

Global wheat: Chicago -22.25c, Kansas -17.25c, MATIF -€4.00. Friday’s session was a case of classic post-event liquidation, with the two key risk points for the week — the May WASDE and the Trump/Xi summit — now in the rearview mirror and the mystery that had kept longs committed largely gone. Markets were higher early in the overnight session before deteriorating steadily through Friday.

The WASDE’s surprisingly low HRW production number initially sparked a limit-up reaction, but the conversation quickly shifted to slashed export forecasts, raised import projections, and the prevailing view that this represented the smallest crop estimate of the season rather than a genuine supply shock.

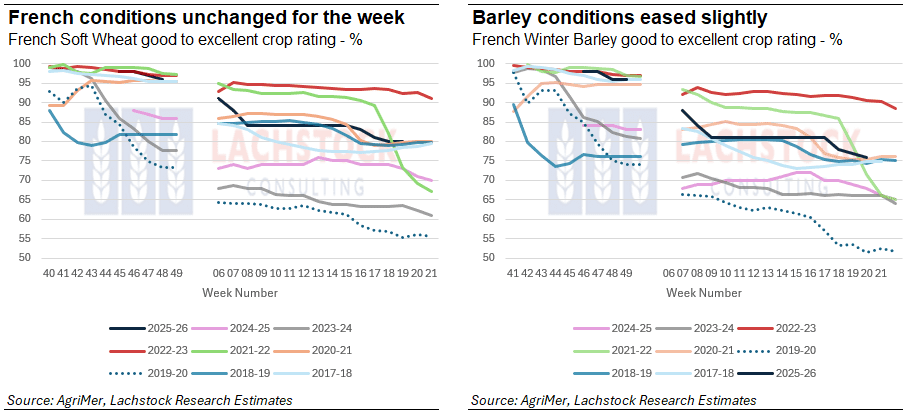

On the crop condition side, France rated 80pc of its soft wheat good or very good as of May 11, steady on the week and above year-ago levels, while Rouen port exports jumped to 230,385t for the week, up sharply from 141,463t the prior week.

Russia provided the one bearish offset, with heavy rain and cold producing what analysts described as the worst start to spring planting in many years.

Morocco’s soft wheat import requirement for 2026-27 is expected to fall to between three and four million tons from five to six million tons this season following a strong domestic harvest.

Other grains and oilseeds: Corn -11.75c, soybeans -15.50c, canola +C$5.75. The same post-summit disappointment that weighed on wheat drove corn and beans lower, with speculative buyers who had positioned aggressively ahead of the Trump/Xi meeting caught on the wrong side as no specific Chinese purchase commitments materialised.

Corn fell 11.75c with South American supplies remaining competitively priced and no weather threat emerging in the US, while beans dropped 15.50c as the 180Mt Brazilian crop reality returned to the conversation and the Argentine harvest began making meaningful progress, helped by dry and cooler conditions expected through May and June.

The product complex told a different story, with crush margins surging to new highs as meal and oil both found support. April NOPA crush came in at 211.9M bushels, slightly below the 215.8Mb estimate but well above the year-ago 190.2Mb, while soybean oil stocks were tighter than forecast.

The USDA announced a daily sale of 155,000t ns of soybean meal to Italy, the third such sale since mid-March and consistent with earlier reports of Italy redirecting away from Argentine meal. Soybean oil’s premium over palm oil reached $507/t, the widest since October 2023, underpinned by biofuel mandate demand and the passage of US legislation allowing nationwide year-round E15 sales.

ICE canola bucked the broader weakness, finishing higher on the back of rising crude, a softer Canadian dollar, and delayed Prairie seedings, though cumulative export pace at 6.7Mt remains well behind the 8Mt shipped by this point last year.

Macro: AUD US71.5c, Dow -537pts, crude +$4.25. Crude surged 4.2pc as Trump returned from Beijing without any concrete progress on reopening the Strait of Hormuz, with US-Iran negotiations described as deadlocked. Brent crude has now risen roughly 50pc since the start of the war, and the risk of fresh escalation continues to dominate the macro backdrop for commodity markets. On the ag trade front, US Trade Representative Greer flagged expectations of double-digit billions in annual Chinese agricultural purchases across all commodities, but no binding agreement was announced and the market treated the blanket statements as insufficient to hold long positions.

Spot urea in New Orleans declined 6.2pc on the week to its lowest since late February, though at $565 per short ton, it remains around 20pc above pre-war levels.

Local markets: The week ended softer in the west, with canola down $8/t to $795, while new season was bid $830. Wheat was $347 current and $370 new, with barley $336 and $331 FIS Albany. Through the east, canola eased to $770 current and $806 new crop, wheat was $345 and $365, while barley was $315 and $328 track Geelong. Handy falls through SA’s Eyre and Mallee extended into the Vic Mallee and Wimmera, with water laying again and moisture profiles filling. SNSW picked up a welcome 10-25mm, though more will be needed. With new-crop production prospects improving by the week across SA and Vic, it will be interesting to see whether growers step up engagement on both current and new-season sales.

HAVE YOUR SAY