Weather: The US is in for a wet weekend with Illinois set to cop it on Sunday. Only 20% of winter wheat has been harvested in that state as per the last update so this forecast isnt ideal

Weather: The US is in for a wet weekend with Illinois set to cop it on Sunday. Only 20% of winter wheat has been harvested in that state as per the last update so this forecast isnt ideal

EU will see most of the heat over the next two days – France the worst hit.

Markets

Im a little surprised with the lack of interest in Ag markets overnight – The fact one of the major Russian refineries was blown up is not only impactful for the capitals energy requirements, but also pretty symbolic. As has been the case through this conflict – any escalation is generally met with a over weighted response – and one of the logical targets will be Ukraine’s port infrastructure – amazingly they are still shipping really.

Many in the middle east are not happy with Donalds deal – some indicating that deal actually strengthens Iran.

Day Ahead – Australia

A long weekend in the US should keep things a little quiet but, personally, i wonder how wheat markets look if Russia’s retaliation effects grain supply chains. I get that the market is exhausted and somewhat insensitive to Russia/Ukraine conflict – however, the Asian consumer will be watching with interest as Russian supply will be the price setter for July forward

.

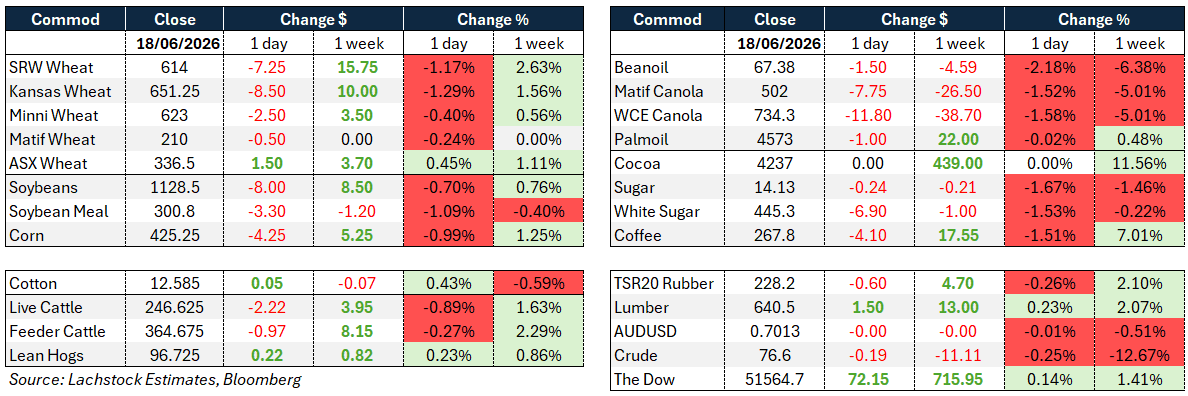

Wheat: A broad sell-off into the Juneteenth long weekend as traders pared risk, with WN off 7c, KWN down 8.5c and MWN down 2.5c. Implied vol in WN eased to 26.03% from 30.12% Wednesday.

Wheat: A broad sell-off into the Juneteenth long weekend as traders pared risk, with WN off 7c, KWN down 8.5c and MWN down 2.5c. Implied vol in WN eased to 26.03% from 30.12% Wednesday.

The main difference versus the prior session was the absence of China rumours; weather was largely unchanged.

The Midwest stays waterlogged for the next 10 to 15 days, threatening SRW quality and delaying harvest, with the wettest pockets in the central Midwest.

The EU remains hot, with a heat wave pushing temperatures 5C to 12C above normal across France, Germany, Italy, Spain and southern England.

India’s monsoon has started nearly 40% below normal, while Australia’s east looks wet near term and WA has rain in the 6 to 10 day window.

US weekly sales were 401k vs 500k expected, with Japan, Mexico and the Philippines the top buyers.

Algeria’s OAIC bought over 800,000t of milling wheat at around $264 to $265 c&f, with Black Sea origin expected to dominate. South Korea picked up 55,000 to 65,000t of feed wheat privately at $277.25 c&f from ADM, optional origin excluding Russia and Ukraine.

South Africa will hold its current import tariff framework.

Geopolitically, the Iran peace deal was signed just as the Ukraine/Russia conflict escalated, with Ukraine reaching deeper into Russia more consistently and wire stories suggesting Russian strikes on infrastructure could cut Ukrainian exports by a third.

Other grains and oilseeds: Corn sold off with CN down 3.5c and CZ down 4.75c, though the wet weather threatening SRW is viewed as gold for corn production, with rain continuing through most of June.

Some privates flagged the potential for heat entering the corn belt around June 29th.

Old crop corn sales were 1.157mil vs 1.050 expected and new crop 519k vs 800k expected, with Japan, Mexico and Spain the largest buyers, plus a daily sale of 286k new crop to Mexico.

EU heat may sustain Spanish corn imports, Argentina is the cheapest fob and landed Asia, and Brazilian corn use for ethanol set a record on May data.

In the oilseed complex it was a shutout. SN lost 9.25c, SMN dropped $3.50 and BON sunk 185 points, taking July crush down 18.75c to 306.75 — the same crush that settled at 417.50 on June 3rd. Bean oil liquidation continued despite constructive fundamentals, with RIN generation implying the mandate is not being met; soyoil fell to its lowest in more than eight weeks tracking crude lower.

Beans dipped despite confirmation of China business, with the USDA announcing 132k new crop to China and 120k to unknown — the first daily sale to China in four months — as traders watch progress toward China’s 25 MMT commitment.

Weekly bean sales were 425k old vs 200k expected plus 304k new, meal 284k old plus 120k new, and bean oil 2.2k old plus zero new.

ICE canola was weaker, pulled by crude, with November holding below its 20- and 50-day averages but above the 100-day; Saskatchewan seeding reached 97% complete.

Malaysian palm eased with rival oils, while Indonesia remains on track to launch its B50 mandate on July 1.

Macro: The hawkish twist in the June FOMC dot plot reflects prioritising a return of inflation to target and supports rates staying on hold for now, albeit with a hawkish bias. The Fed is focused on whether higher energy prices percolate more broadly into second- and third-round effects, though inflation data so far suggest that has not occurred and the recent sharp fall in oil implies the shock may prove transitory.

The removal of the easing bias is appropriate, with the committee split nine for higher rates by year end and nine against, and Warsh not submitting a forecast; the bar to raise looks high for the Board of Governors and Williams, suggesting a majority of voters do not expect higher rates by year end.

The Bank of England left rates unchanged in a 7:2 vote, with economic weakness expected to keep rates on hold before cuts resume in Q4.

Domestically, trimmed mean inflation is expected to rise 0.3% m/m in May with upside risk, headline easing 0.3% m/m to take annual growth to 4.3% y/y, ahead of the RBA’s forecast of a high 0.9% to 1.0% q/q for Q2 trimmed mean.

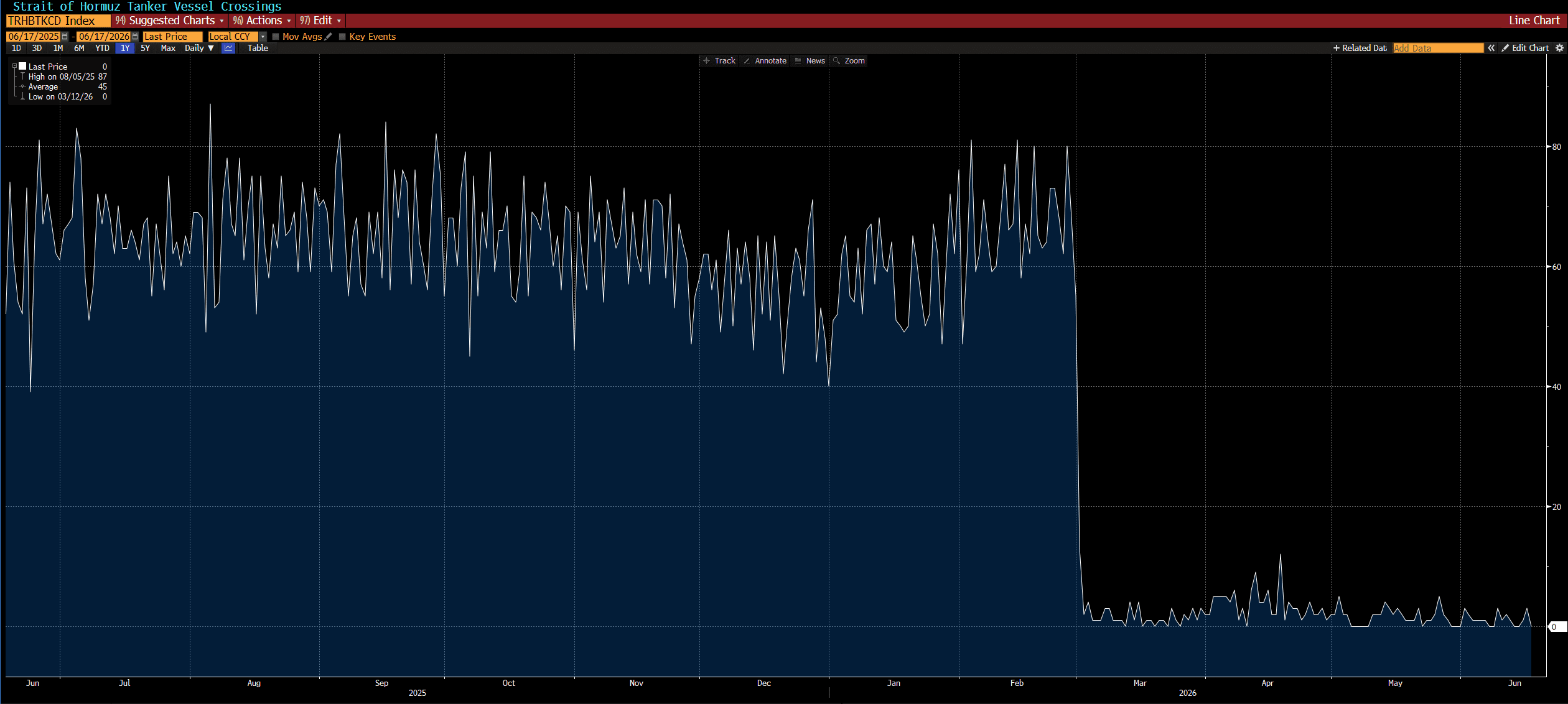

On oil, the Iran deal saw tankers move through the Strait of Hormuz, with crude down 16% since the start of the month and Middle Eastern prices likely to fall further on the strait’s reopening; Trump flagged he may reinstate sanctions on Russia to keep oil low.

Local markets: Through the west of the country canola found some support to be bid $795 for current season and $830 for new, wheat was +$3 to $343 and $357, barley $332 and $324 FIS Albany.

In the east canola was $750 current season and $785 new, wheat was $332 and $345, barley $310 and $315 track Geelong.

Barley feels like it has found some engagement over the last few days with values +$3. Further downside appears limited given ongoing feed and export demand alongside a relatively tight balance sheet. Canola has come under pressure from weaker crude oil, however global vegoil demand remains rock solid. Building a bullish case for wheat remains more challenging.

The EYCI briefly traded above 1000c/kg this week for the first time since 2022, but unlike the last rally which was driven by severe cattle shortages during herd rebuild, the current surge is being fuelled by aggressive restocker demand despite significantly larger cattle numbers nationally.

HAVE YOUR SAY