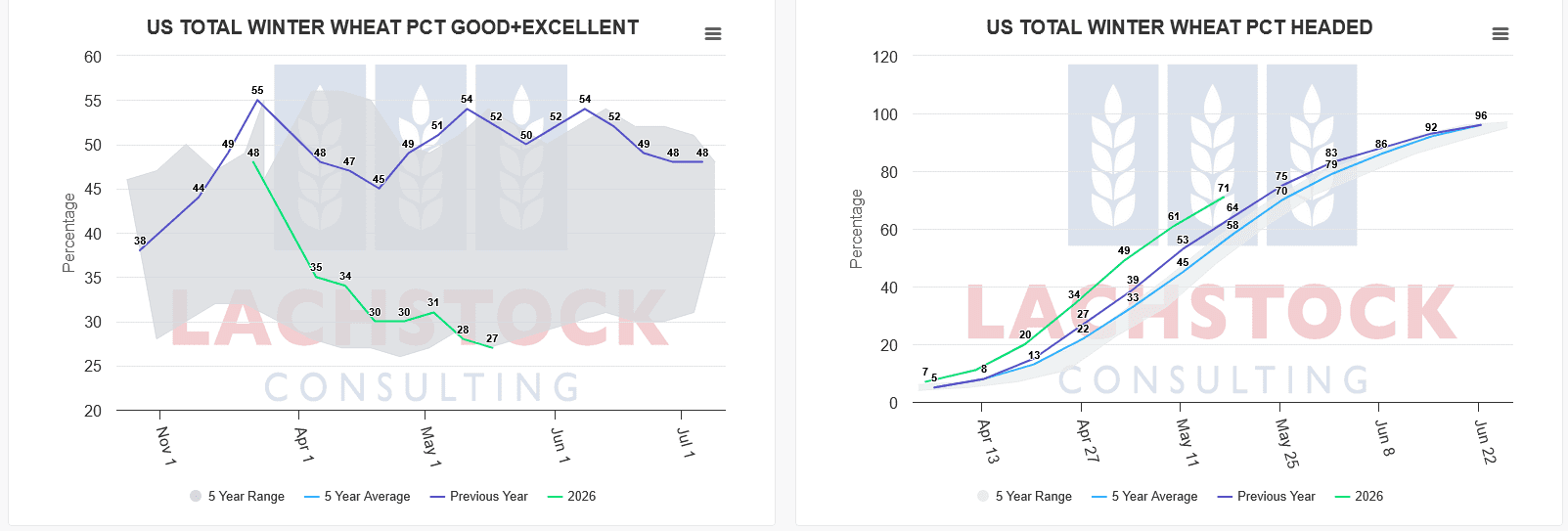

Weather: US condition reports continue to reflect what a challenging season they have had, particularly in the main HRW states.

BOM still calling for more rainfall through the eastern states – fair to say there are some non-believers out there.

Still concern around Spring Wheat planting pace in Russia which has been belted with rainfall

Markets

Donald exerting his influence – not least of which was his recently disclosed trading activity – The Don is having a crack.

According to the market, it likes the trade deal – in the case of wheat however, it feels like its got ahead of itself a little – remember there isn’t a stipulation on what they have to buy, just they have a number to spend.

Day Ahead – Australia

Ground hog day

Northern Sorgo has caught a bid with at least one of the bigger cattle feedlots making the shift to include sorgo in the ration.

New crop pricing should be supported today – 27/28 also starting to get some liquidity.

.

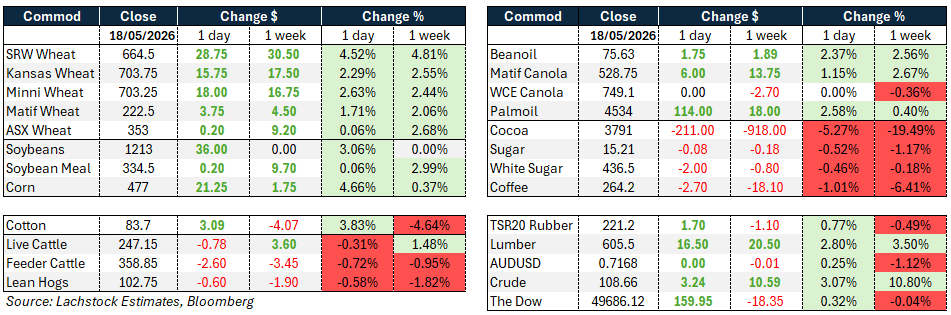

Global wheat: Chicago 664.5 (+28.75, +4.52%), Kansas 703.75 (+15.75, +2.29%), MATIF 222.5 (+3.75, +1.71%)

Wheat surged on Monday after the White House confirmed over the weekend that China has committed to purchasing at least $17 billion of US agricultural products annually in 2026, 2027 and 2028. Chicago SRW gained 28 cents, Kansas HRW rallied 15.75 cents, and MATIF September closed up €3.50.

Implied volatility in Chicago jumped sharply, with the front month going out at 35.28% versus 32.25% on Friday, reflecting the abrupt reversal in sentiment from last week’s liquidation mood.

The trade deal announcement was the dominant driver, though the market is debating how much of the $17 billion figure represents genuinely new demand versus a redirection of existing trade flows. SRW is seen as a potential beneficiary given China has some history of purchasing that class, and with the current US carryout sitting at 93 million bushels, even a modest Chinese programme of 15-20 million bushels would be significant.

HRW conditions continued to deteriorate, with Kansas poor-to-very-poor ratings jumping 7% on the week, adding a weather premium to an already charged market.

Russian cash wheat was unchanged at $241. Separately, US buyers were again reported purchasing Polish milling wheat from the new crop, with estimates ranging from 120,000 to 350,000 metric tons, reflecting the competitiveness of European origins against elevated US prices.

Algeria issued a tender for 50,000 tonnes of soft milling wheat, and South Korea picked up around 130,000 tonnes of feed wheat in private deals.

Egypt reported local procurement of 3.3 million tonnes since mid-April, around 600,000 tonnes above last year’s pace.

Weekly US wheat export inspections were soft at 223,972 tonnes, well below the prior week’s 511,703 tonnes and last year’s 431,383 tonnes.

Other grains and oilseeds: Corn 477 (+21.25, +4.66%), Soybeans 1213 (+36.00, +3.06%), MATIF Canola 528.75 (+6.00, +1.15%)

Corn surged 21.25 cents in the front month on the back of the China trade deal announcement, with the December contract gaining 17 cents.

China is widely expected to be a significant corn buyer under the new commitment given it already has substantial involvement in US sorghum this season and US corn was the cheapest landed origin into Asia heading into today’s session.

Planting progress came in at 76% complete versus 75% expected and the five-year average of 70%, offering no weather-related resistance to the rally.

Soybeans gained 36 cents as the complex responded to the combination of Chinese demand optimism and storm activity across the Corn Belt, with severe thunderstorms, tornadoes and flash flooding reported across growing areas and wind and hail damage in Kansas and South Dakota.

Bean oil soared 175 points while meal gained only fractionally, leaving the July crush down 16.5 cents to 354.75.

Brazilian soybean premiums tumbled in response to the perceived rush toward US origins, a familiar pattern when the market senses a surge in US export demand.

US soybean planting came in at 67% complete after the close, ahead of the 66% estimate and well above the five-year average of 53%.

The MARS unit trimmed its 2026 EU rapeseed yield estimate to 3.19 tonnes per hectare, down 1.8% from a month earlier due to late frosts in central and eastern Europe, though the figure remains broadly in line with the five-year average.

India is also reported to be considering higher import duties on vegetable oils.

The latest CFTC commitment of traders data showed managed money reducing longs in corn and soybeans while adding shorts in wheat, which paradoxically reduced the risk of a disorderly selloff when the trade deal news broke.

Macro: AUD US0.7168 (unchanged, +0.25% on week), Dow 49,686 (+159.95, +0.32%), Crude 108.66 (+3.24, +3.07%)

Risk assets were generally firmer on Monday though trading was choppy, with the Dow closing up around 160 points as markets weighed the positive signal from the US-China agricultural trade deal against an unresolved Iran situation.

Crude rose over 3% on the day as the Strait of Hormuz remains effectively closed to Persian Gulf oil exports, though President Trump announced late Monday that planned strikes on Iran had been called off following appeals from Saudi Arabia, Qatar and the UAE, who sought two to three days to pursue a diplomatic resolution.

Oil and equities whipsawed through the session on the conflicting signals, with WTI falling 1.4% after Trump’s remarks before partially recovering. The situation remains fluid with no confirmed resumption of formal talks from Tehran, which has maintained hard positions on its nuclear programme and insists on the return of frozen assets and war reparations.

The US Treasury extended a sanctions waiver allowing Russian oil sales for a further 30 days to provide relief to vulnerable nations.

Trump also indicated he had raised with Xi Jinping the possibility of lifting sanctions on Chinese companies buying Iranian crude, noting that China accounted for around 90% of Iranian oil exports before the war.

Putin is due in Beijing on Tuesday and Wednesday for discussions expected to include the Iran conflict.

Analysts at StoneX flagged that the real impact of rising energy costs on agricultural input prices is likely to be felt most acutely in June and July, with longer-term fertiliser implications potentially affecting 2027 global crop productions.

Local markets: The week started firmer in the west, with canola bid A$805/t current season and $845 new crop, wheat $350 and $369, and barley $337 both current and new crop FIS Albany.

In the east, canola improved to $784 current and $807 new crop, while wheat was $340 and $368, and barley $317 and $330 track Geelong.

Northern markets have continued to ease, with Downs Jun/Jul wheat now bid around $414, back from the mid-April high of $450. Barley remains firmer at $423 and harder to buy.

Local markets will be interesting today after strong offshore gains overnight, particularly in the US, which now looks well out of place on global pricing. Canola should see more direct support, while wheat gains may be more muted given local basis and export competitiveness.

HAVE YOUR SAY