Weather: The glimmer of hope for NNSW and Qld evaporated over the weekend. The whole east coast looks like it will be relatively clear for the next 8 days with some rainfall through WA.

Kansas is struggling, but the fact it avoided a frost event is a real positive for production. The crop is advanced and it would have done some damage. The US drought monitor shows OK getting worse over the last 2 weeks

Markets

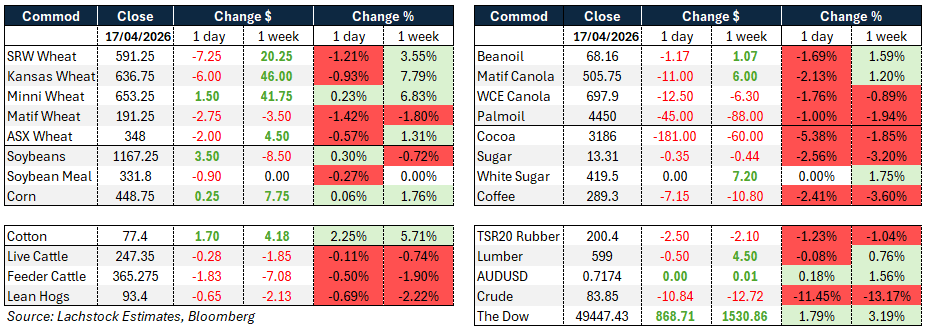

The US navy shot out an engine room of a Iranian vessel… that feels like an escalation… According to the Bloomberg tracker, 17 vessels got through on the first day the strait was opened, only 1 yesterday.

So, here we go again – strait is closed and energy is ripping. no end in sight.

Day Ahead – Australia

Hard to unwind the offshore noise and how it relates to Australia. The import relativity onto the downs is more captivating with traders doing the calcs from SA and WA – based on Fridays numbers, it works to a Brissy end user but not the Downs yet. Oddly, diesel fell last week which increases the reach in the central west of NSW. This week will be interesting given the lack of rain in the forecast.

Source: Bloomberg Strait of Hormuz commercial vessel crossings

Global wheat: (Chicago: -1.21%, Kansas: -0.93%, MATIF: -1.42%)

Wheat markets opened sharply lower Friday after Iran announced the Strait of Hormuz was open, triggering an exodus of weak long positions across the grain complex. Chicago shed 7.25 cents, Kansas lost 6 cents, and MATIF May dropped €2.75, while Russian cash held flat at $238.50.

The selloff was heaviest early in the session, with markets finding stability through the afternoon — Kansas finished 12 cents above its session low and Chicago recovered 7-8 cents from its worst levels.

Minneapolis was the standout, posting gains of 1.5 cents on the back of a spread that had gotten too narrow relative to Kansas City.

Implied volatility in Chicago eased notably, with May vol closing at 28.31% versus 31.71% the prior session.

Despite the recovery, wheat remains caught between bearish macro sentiment and genuine crop concerns.

It looks like KS avoided a freeze over the weekend with the line tinning through NE and half of Il.

French wheat crop conditions remain firm at 84% good to excellent, while chatter around lower Australian wheat acres for the coming season continues to circulate.

Other grains and oilseeds: (Corn: +0.06%, Soybeans: +0.30%, MATIF Canola: -2.13%)

Corn and beans both suffered macro-inspired liquidation early before staging impressive recoveries.

July corn finished fractionally higher after dipping to $4.57, with the market in a holding pattern as traders weigh whether a Trump-Xi thaw could direct Chinese purchases toward US corn, monitor US planting progress, and wait on South American harvest clarity.

Argentina is finally approaching a dry window that should help resolve the gap between USDA’s 52 million tonne estimate and private Argentine forecasts above 60.

Turkey was also noted as seeking 5 million tonnes of world corn through July.

Soybeans rallied 3.5 cents in the May contract, driven by meal strength, while soyoil dropped 117 points on the back of crude’s collapse, leaving May crush down 18.25 cents to 312.5.

Bean volatility remains compressed with SK vol at just 11.70%, reflecting a market going nowhere fast — unable to break on product strength, yet finding a bid whenever crush corrects lower.

ICE canola fell sharply, with the May contract down C$12.50 to C$697.40, dragged lower by crude, soyoil and MATIF rapeseed.

Agriculture and Agri-Food Canada’s April estimates left canola production for 2026-27 unchanged at 19.2 million tonnes with ending stocks at 1.06 million tonnes.

Cumulative Canadian canola exports stand at 5.9 million tonnes, running approximately 1.5 million tonnes behind last year’s pace.

Macro: (AUD: +0.18%, Dow: +1.79%, Crude: -11.45%)

The dominant macro story Friday was the collapse in crude oil, with WTI falling over 11% to around $84.50 a barrel following Iran’s announcement that the Strait of Hormuz is open and nuclear talks could resume.

The move reverberated across commodity markets, pressuring vegetable oils and grains while simultaneously boosting equities, with the Dow adding 868 points.

The reopening of Hormuz is being interpreted as a signal that central banks globally may return to an easing bias, with odds of at least one Fed cut by December jumping from 30% to 50% on CME FedWatch.

The Australian dollar was marginally firmer on the day. The weekend dynamic leaves markets on edge, with the durability of the US-Iran goodwill yet to be tested and a full slate of USDA data — weekly export inspections and crop progress — due Monday.

Local: Friday’s WA bids were firmer to end the week with canola A$778/t for current and $820 for new season, wheat was $332 and $358, barley $340 and $331 FIS Albany.

In the east of the country bids were firmer with canola $760 current and $790 new, wheat $337 and $365, barley $315 and $325 track Geelong.

Any rainfall through the east of the country that was starting to appear in forecasts has now been pulled, likely to keep a firm floor under domestic bids.

In other news, Australian wool prices pushed higher again this week despite a larger offering and firmer AUD, with the EMI up 39c to 1825c/kg clean — now the highest since June 2019 — as strong buyer demand, particularly for better-style finer Merino types, more than offset the bigger bale volume.

HAVE YOUR SAY